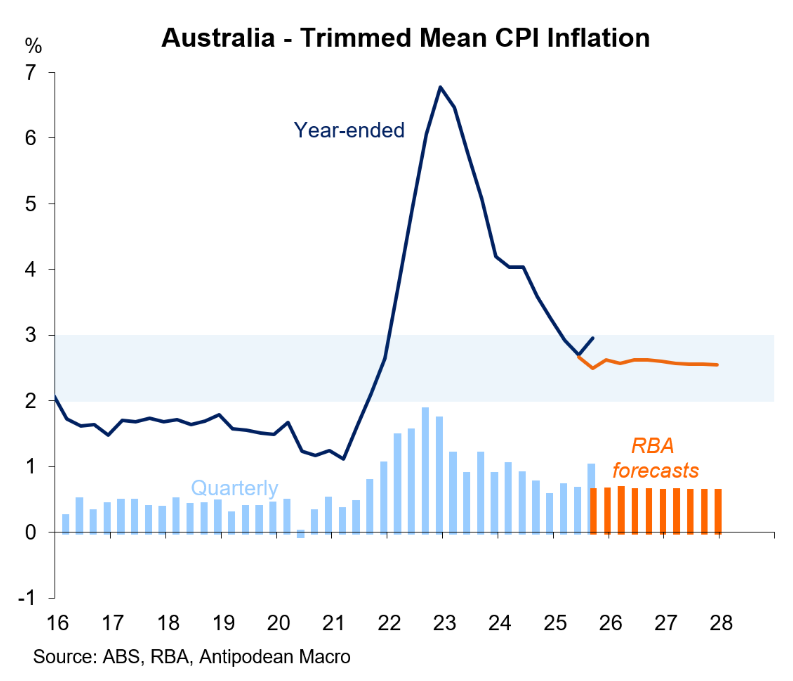

Last week, the Australian Bureau of Statistics (ABS) reported that the policy-relevant trimmed mean inflation surged by 1.0% in the September quarter to be 3.0% higher year-on-year—the top of the Reserve Bank of Australia’s (RBA) target band.

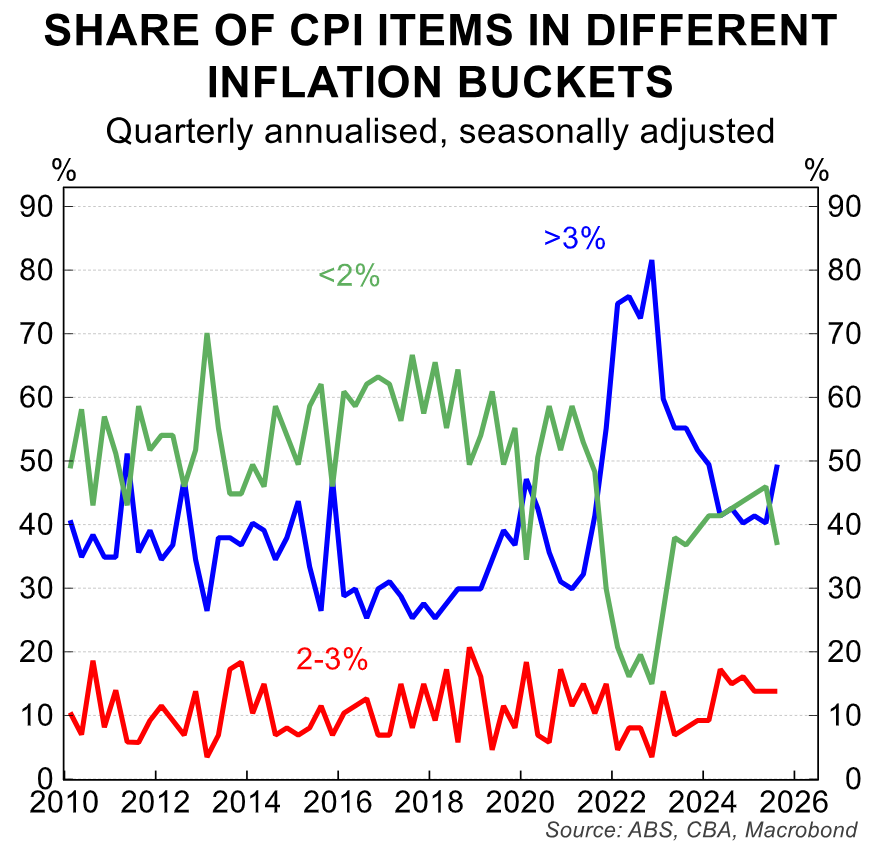

Inflation pressures were broad-based, with the share of CPI items growing above 3% rising to 50% in Q3, up from 37% in Q2:

The surge in CPI inflation has killed off hopes of near-term interest rate cuts, with financial markets ascribing a near-zero chance of the RBA cutting rates further.

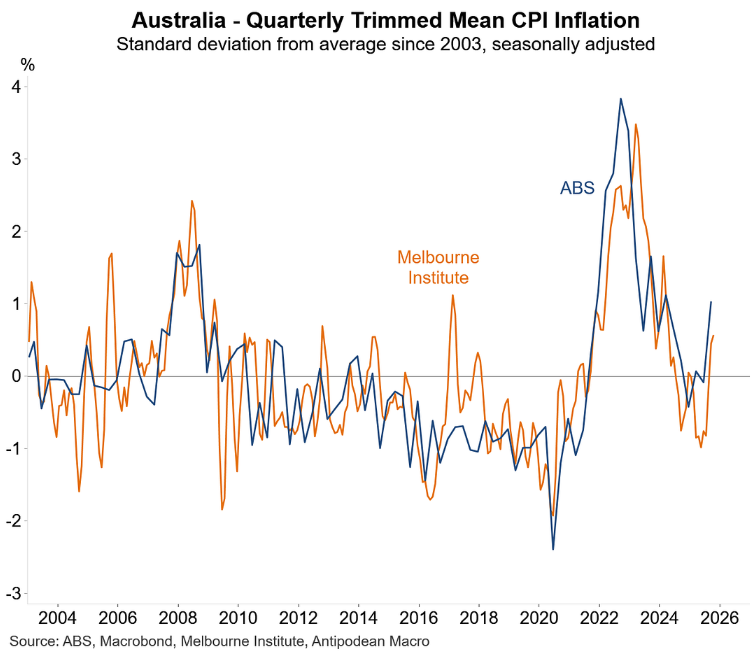

On Monday, the inflation picture in Australia worsened, with the unofficial Melbourne Institute (MI) measure of trimmed mean inflation surging higher.

As illustrated below by Justin Fabo from Antipodean Macro, MI quarterly trimmed mean inflation continued its upward surge in October, mirroring the quarterly jump in the ABS trimmed mean inflation:

Overall, the result bolsters the case that the RBA will keep interest rates on hold for the foreseeable future.

For the RBA to even consider a rate cut would require:

- Trimmed mean inflation falling back toward the middle of the target band (i.e., closer to 2.5%); and/or

- The unemployment rate rising significantly above its current level of 4.5%.

A significant rise in unemployment is the more likely outcome given the rapid expansion in labour supply (courtesy of high immigration) amid weak private sector employment growth.

But even if unemployment were to rise, any additional rate relief would be unlikely to arrive until the second quarter of 2026 at the earliest.