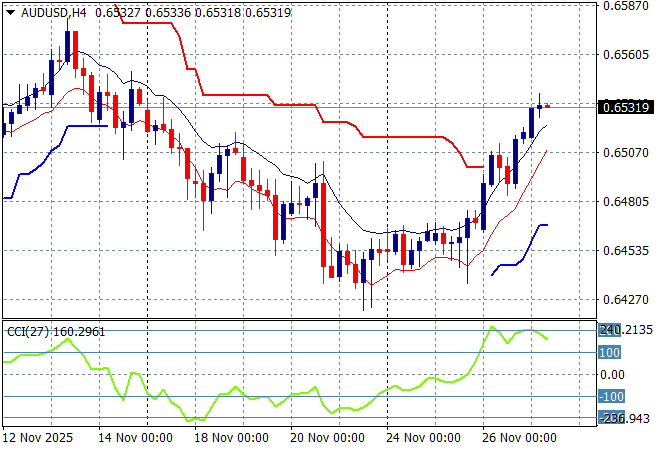

Asian equity markets are generally up with the lack of a lead tonight as Wall Street will be closed for thanksgiving (thanking the AI bubble that is stuffing the stock market turkey that it is). Movement has been more regional as Chinese markets react to the latest and slow industrial production numbers while locally capex numbers are much higher than expecting, giving more concern to the case that the RBA will raise rates in 2026. The Australian dollar is still moving above the 65 cent level against USD pulling the Kiwi along with it to a near monthly high.

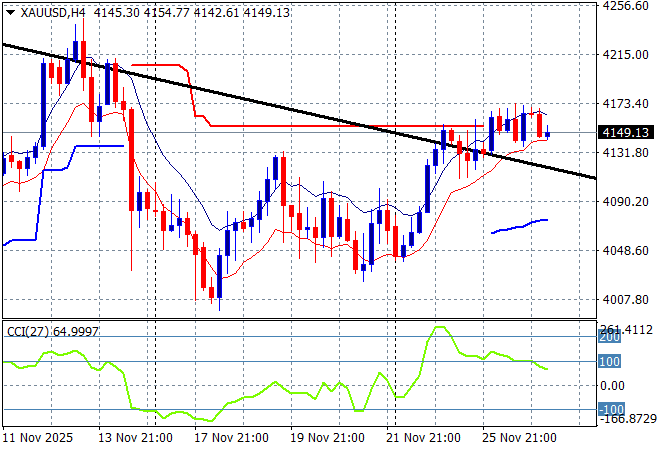

Oil markets are steady but very weak with Brent crude drifting towards the $62USD per barrel level while gold is holding on to its recent gains as it steadies just below the $4150USD per ounce level:

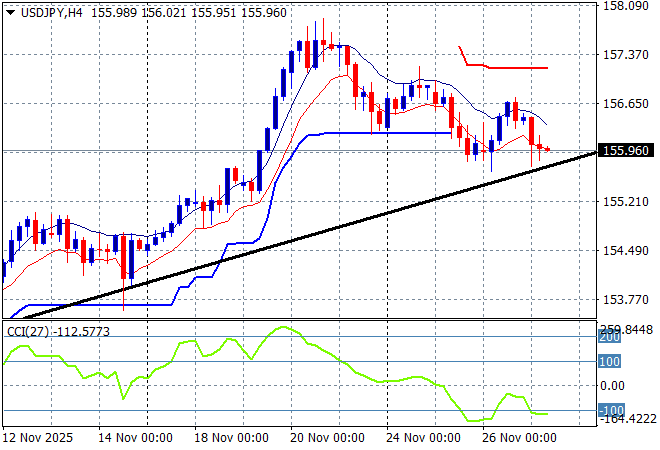

Mainland Chinese share markets are lifting slightly in afternoon trade with the Shanghai Composite up 0.4% to 3882 points while the Hang Seng Index is up around 0.4% to 26028 points. Japanese stock markets are pushing much higher however with the Nikkei 225 up 1.2% to breach 50000 points with the USDPY pair falling back below the 156 level:

Australian stocks are putting in a near scratch session with the ASX200 up just 0.2% to 8617 points while the Australian dollar has continued its lift above the 65 cent level against USD as it looks like the RBA has lost the inflation game:

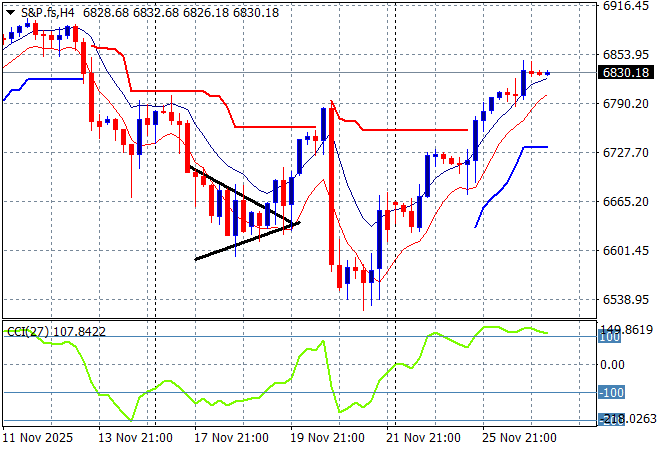

S&P and Eurostoxx futures are steady given the closed session on Wall Street tonight with the S&P500 four hourly chart showing a hold at last weeks highs around the 6800 point level:

The economic calendar is European focused tonight with closed US markets for Thanksgiving, with German consumer confidence and few ECB speeches to keep an ear out for.