Asian equity markets are mixed in today’s session as Japanese markets return with all eyes on talks between China, Japan and USA in recent days but the newsflow and outcome has been vague at best. With the shortened trading week due to US Thanksgiving risk markets are effectively in a holding pattern. Currency land was fairly stable again as traders digest the continued Fedspeak that may support a possible rate cut in the upcoming December meeting. The Australian dollar is unsteady however, still unable to get back above the 65 cent level against USD.

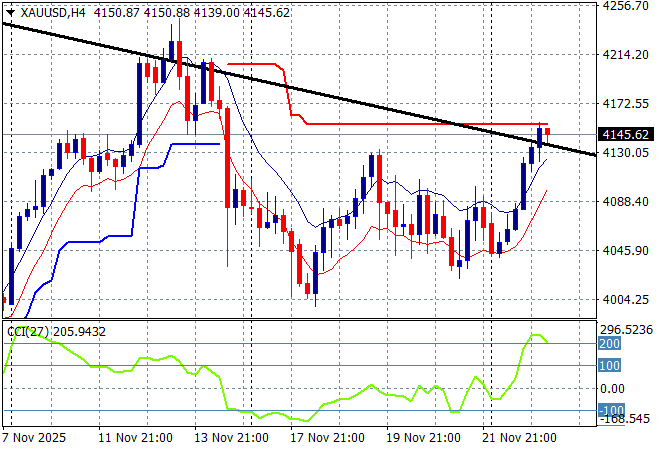

Oil markets are slowly pulling back again with Brent crude drifting below the $62USD per barrel level while gold is doing well to extend its recent gains as it heads up to the $4150USD per ounce level:

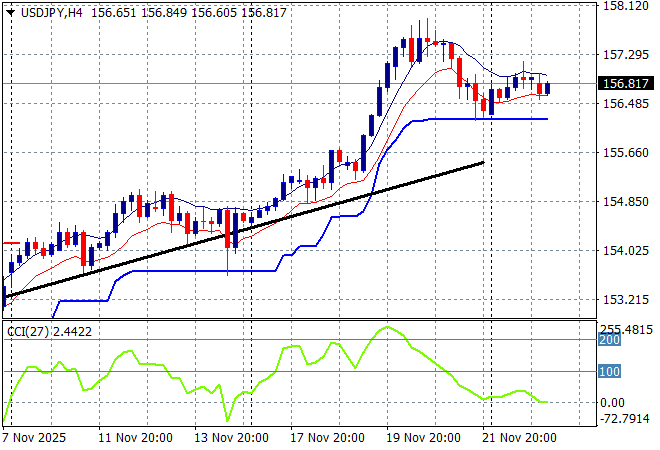

Mainland Chinese share markets are up in afternoon trade with the Shanghai Composite moving more than 1% higher to 3880 points while the Hang Seng Index is up much the same, lifting some 0.7% higher at 25875 points. Japanese stock markets reopened from their long weekend – again – with the Nikkei 225 almost unchanged at 48644 points with the USDPY pair steady above short term support at the mid 156 level:

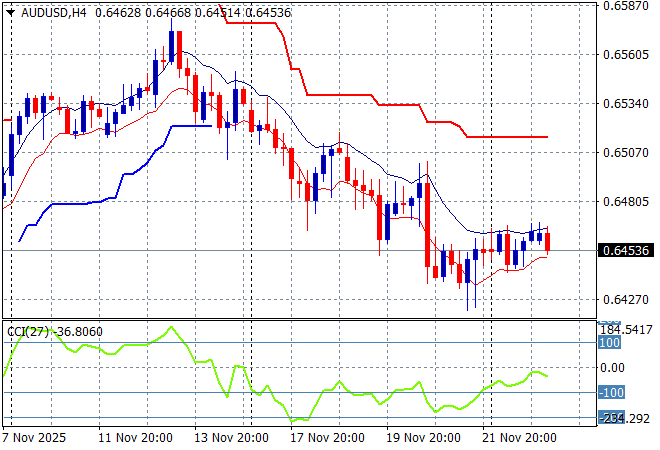

Australian stocks are looking to put in a scratch session with the ASX200 up only a handful of points to 8525 points while the Australian dollar has lost some confidence, hovering around the 64 cent level against USD:

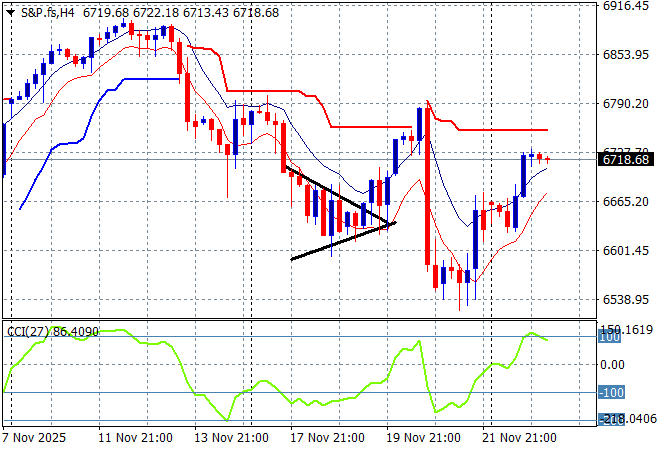

S&P and Eurostoxx futures are eking out small lifts after last night’s rally on Wall Street with the S&P500 four hourly chart showing a possibly return to last weeks highs around the 6800 point level next:

The economic calendar supposedly includes the latest PPI and retail sales data from the US, but with the Trump regime cancelling economy releases left, right and centre (or should that be far right?) who knows if it will be published tonight.