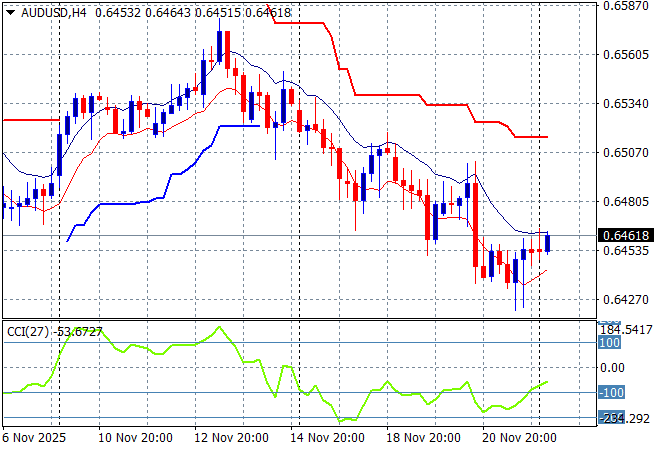

Asian equity markets are fairly buoyant today but Japanese markets are closed while the risk complex ponders the next stage of the Ruzzian/Ukrainian peace “talks” amid a shortened trading week due to US Thanksgiving. Currency land was fairly stable without any large gaps as traders digest the Fed talk from Friday night that may support a possible rate cut in the upcoming December meeting. The Australian dollar built slightly higher but is still under a lot of pressure as it fails to get back above the 65 cent level against USD.

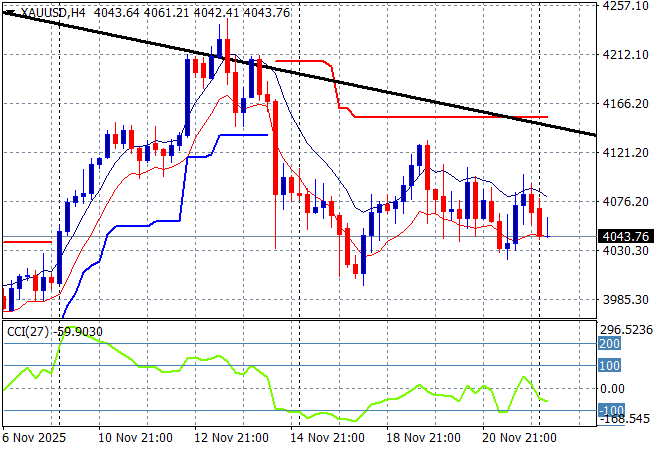

Oil markets are slowly pulling back again with Brent crude drifting below the $62USD per barrel level while gold is failing to stabilise around the $4050USD per ounce level:

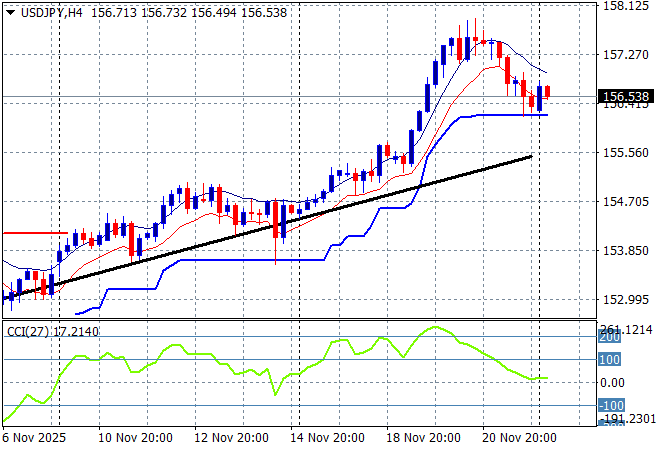

Mainland Chinese share markets are up only slightly in afternoon trade with the Shanghai Composite moving just 0.2% higher to 3843 points while the Hang Seng Index is doing a lot better, up more than 1.2% to 25541 points. Japanese stock markets are closed for yet another holiday with light trading in Yen keeping the USDPY pair steady above short term support at the mid 156 level:

Australian stocks were the best in the region despite of or because of BHP volatility with the ASX200 eventually closing 1.3% higher at 8525 points while the Australian dollar has gained some confidence, gapping above the mid 64 cent level against USD:

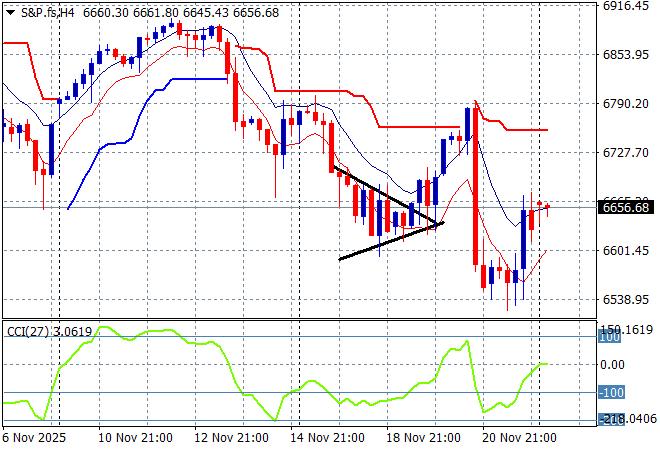

S&P and Eurostoxx futures are struggling to get off the floor although the S&P500 four hourly chart is trying to show a market looking healthier than it really is:

The economic calendar starts the trading week with the latest German IFO survey, then a few Treasury auctions overnight.