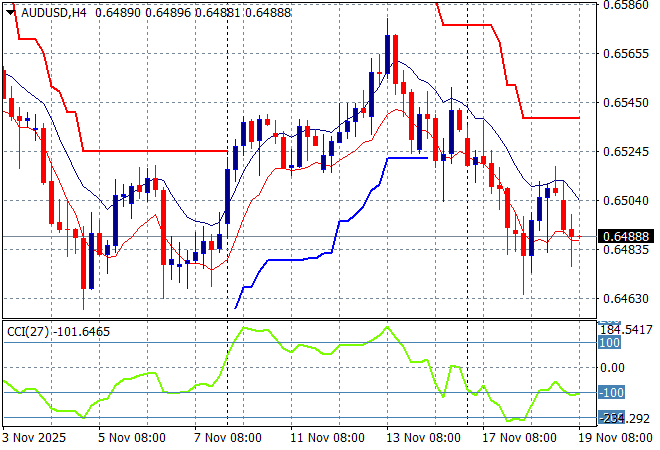

Stocks across Asia had mixed sessions today with domestic pressures overriding the bigger macro picture with tensions between China and Japan still boiling over. Most undollars fell back during the session, especially the Kiwi on the poor PPI print while the Australian dollar lost its gains from overnight on the wages data while Bitcoin briefly fell below the $90,000 level.

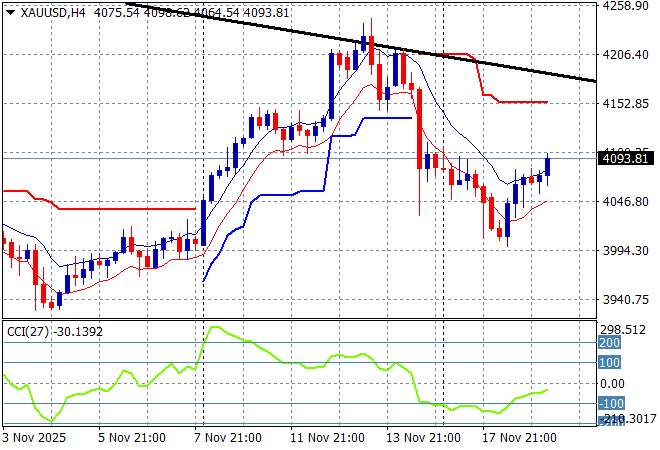

Oil markets are steady and building some internal strength amid the likely invasion of Venezuela by the Trump regime with Brent crude pushing above the $64USD per barrel level while gold is picking up again after bouncing off the $4000USD per ounce level:

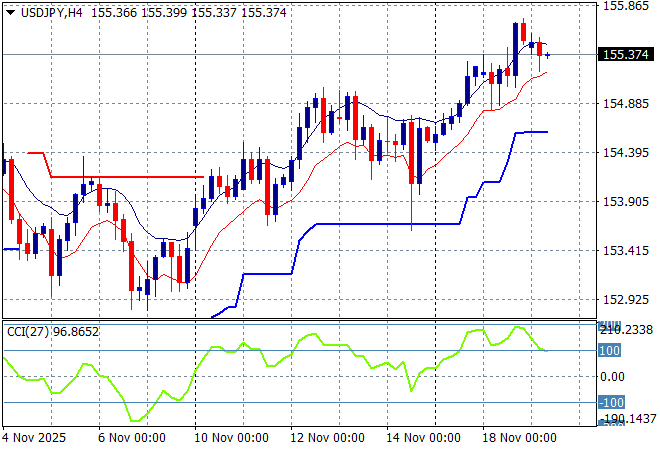

Mainland Chinese share markets are lifting slightly back into the green at the close with the Shanghai Composite up 0.2% to 3944 points while the Hang Seng Index is down more than 0.6%, currently at 25781 points. Japanese stock markets stabilised somewhat on the new stimulus package but look unsteady at best with the Nikkei 225 down nearly 0.3% to remain below the 50000 point level while the USDPY pair has stabilised just above the 155 handle as it went too high too fast from last week:

Australian stocks had a meandering session with the ASX200 eventually closing nearly 0.3% lower at 8447 points while the Australian dollar has dipped back below the 65 cent level against USD:

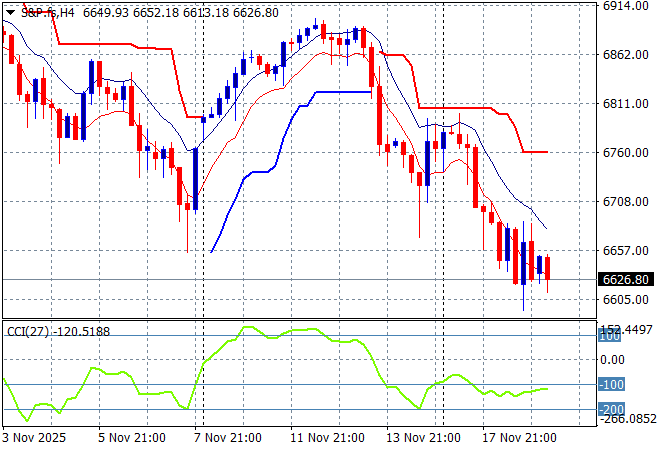

S&P and Eurostoxx futures are trying to stabilise at the previous weekly low but look weak going into the London session with the S&P500 four hourly chart showing the market well below previous support at the 6700 point level:

The economic calendar includes NVIDIA earnings, plus note that the September NFP data is coming out on Thursday night.