A sea of read across Asian stock markets in response to the selloff on Wall Street as the premium for pricing in the re-start of the US federal government is being overshadowed by political events, namely a probable war in central America. Operation “Big Distraction” I think it’s called? Currency markets appear nonchalant however with the Australian dollar holding somewhat steady but looking carefully at the latest Chinese economic releases and iron ore prices with apprehension.

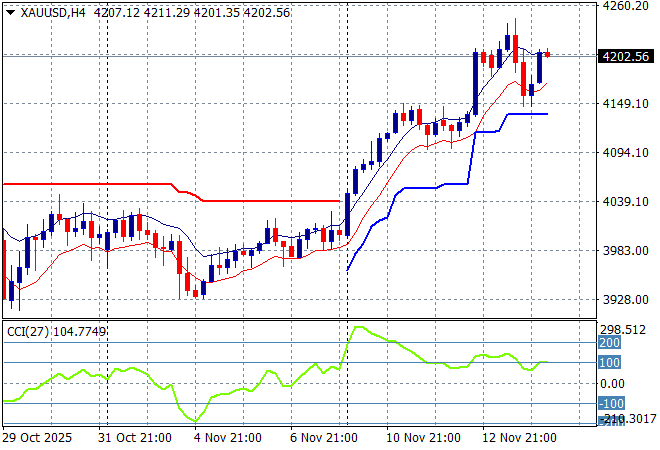

Oil markets are up slightly but still looking very weak amid the risk off mood with Brent crude returning above the $63USD per barrel level while gold is holding steady above the $4200USD per ounce level as it wants to return to the October highs:

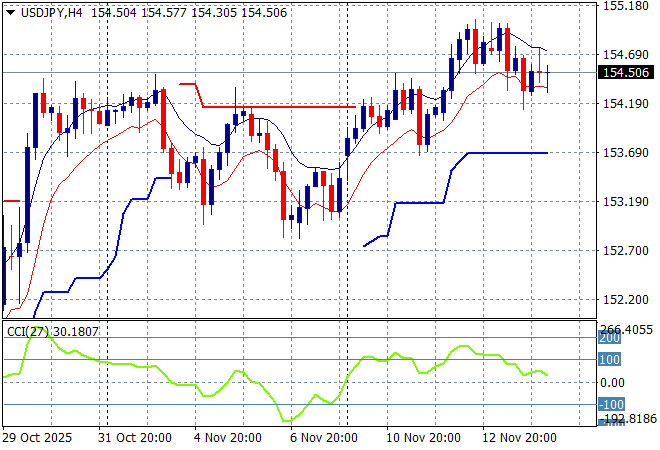

Mainland Chinese share markets are relatively steady going into the close with the Shanghai Composite just holding above the 4000 point barrier while the Hang Seng Index is down more than 1% lower, currently at 26725 points. Japanese stock markets are selling off sharply however with the Nikkei 225 down more than 1.6% to almost retreat below the 50000 point level while the USDPY pair has steadied at the mid 154 handle to hold on to most of its weekly gains so far:

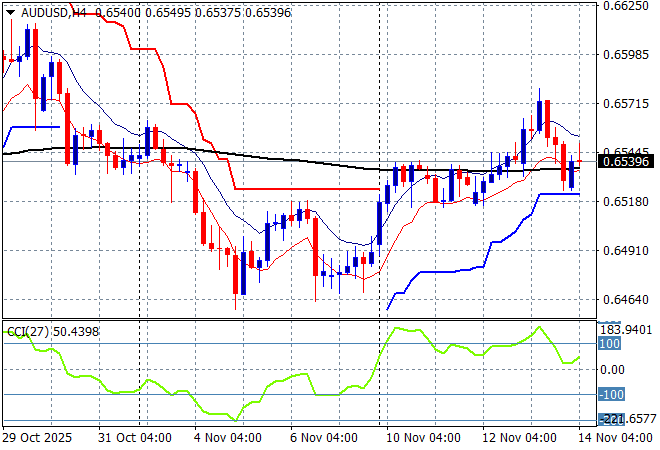

Australian stocks are in line to have the worst falls in the region with the ASX200 down more than 1.4% at 8630 points while the Australian dollar has maintained its position above the 65 cent level against USD:

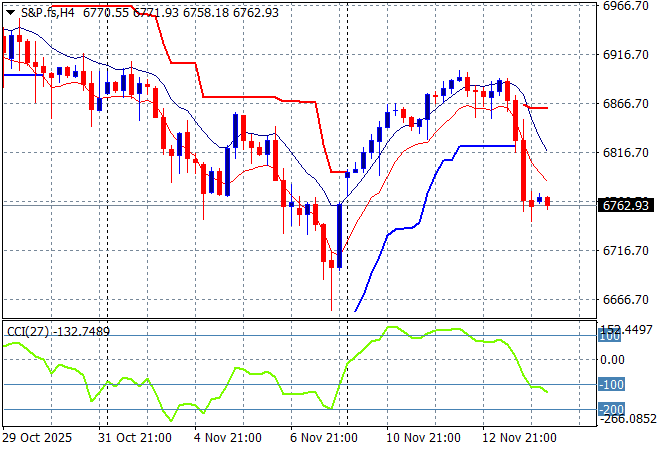

S&P and Eurostoxx futures are steady but starting to move lower again going into the London session with the S&P500 four hourly chart showing the market possibly rolling over like a dead duck – a dead Donald perhaps?

The economic calendar ends the trading week with hopefully the latest PPI print from the US but don’t hold your breath.