First home buyers risk waves of negative equity

Labor’s First Home Guarantee scheme, which commenced at the beginning of October, enables first home buyers to purchase a home with only a 5% deposit without requiring lenders’ mortgage insurance, with the government guaranteeing 15% of the mortgage.

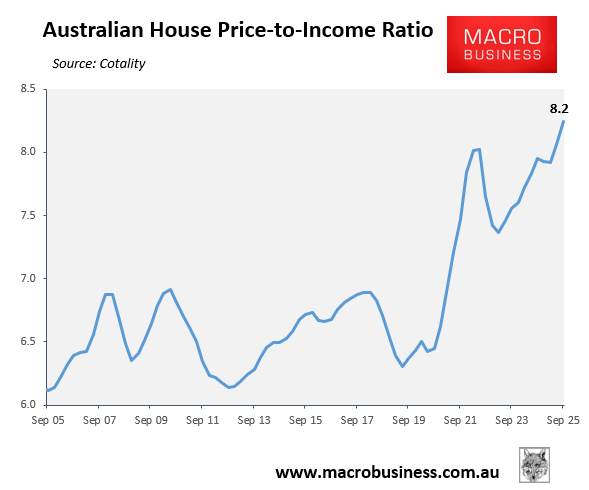

With Australian home values already the most expensive in history relative to household incomes, the First Home Guarantee scheme is widely expected to push home prices higher, making housing structurally less affordable in the future.

While early users of the scheme will likely be okay, since they will ‘get in’ to the market before prices have risen, one of the biggest risks with this policy is that it will leave future first home buyers carrying larger mortgages with thinner equity than they otherwise would have, leaving them vulnerable to future house price corrections and negative equity.

Victorian mortgage arrears highlight the risks facing first home buyers.

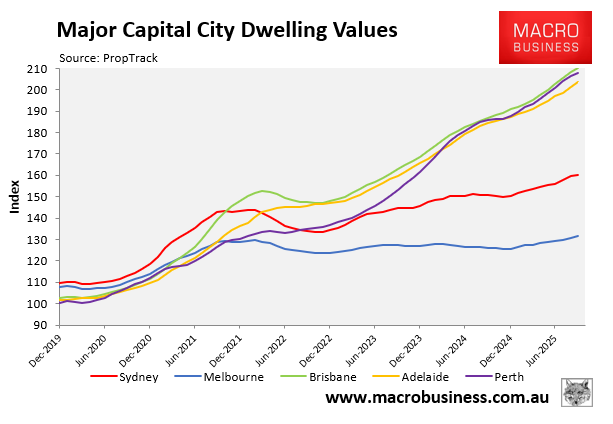

Melbourne’s housing market has been the weakest performing of the capital cities since the pandemic, rising in value by only 22% since March 2020, with unit & apartment values rising by only 13%.

However, the median value hides the fact that a significant share of homes would have experienced price declines.

The sluggish value growth (and price declines in some areas) has meant that Victoria leads the nation in mortgage arrears, with one in every 100 of the state’s mortgages tracking behind on repayments by at least 30 days.

Melbourne is also dominating the nation’s worst-performing postcodes, accounting for six of the nation’s 10 poorest results—a list it has dominated for 18 consecutive months.

S&P credit analyst Erin Kitson explained that there was “quite a close connection” between mortgage arrears and home price growth, and Melbourne’s soft growth could have led to homeowners being unable to sell properties they could no longer afford or left them unable to refinance their loan if they had low equity.

Kitson rightly added that Labor’s 5% deposit scheme for first home buyers could result in more being at risk if the RBA hiked rates in the future or home prices declined.

“Any increase in household indebtedness, particularly if they are younger and don’t have savings buffers or a secondary property, that puts them in a more vulnerable position when the rate cycle changes direction”, she said.

For more than a decade, Australia’s financial regulators have warned against high loan-to-value ratio (LVR) lending. And yet, the federal government has thrown caution to the wind with its state-sponsored 5% deposit scheme, effectively institutionalising high LVR lending.

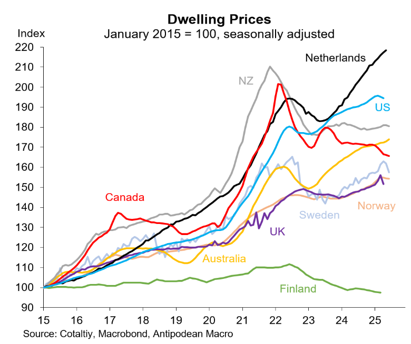

Australia’s most similar economies—New Zealand and Canada—have each experienced severe house price declines of more than 15% from their most recent peaks.

If Australia’s housing market were to experience a similar type of decline, then thousands of first home buyers could be plunged into negative equity, holding mortgages that exceed the value of their homes.

Australian taxpayers, who have guaranteed 15% of first-home buyer mortgages, may also bear contingent liabilities worth billions of dollars.