DXY is still firming. This may go on until the December Fed meeting.

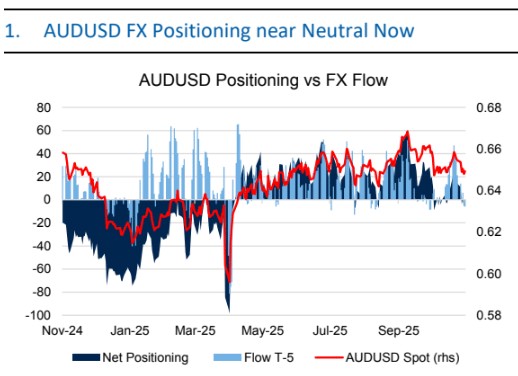

AUD is pinned at 0.65 cents. It looks more likely to break lower given all of those tails.

CNY yawn.

Gold and oil holding.

AI metals are not. This is part of the junk spread widening.

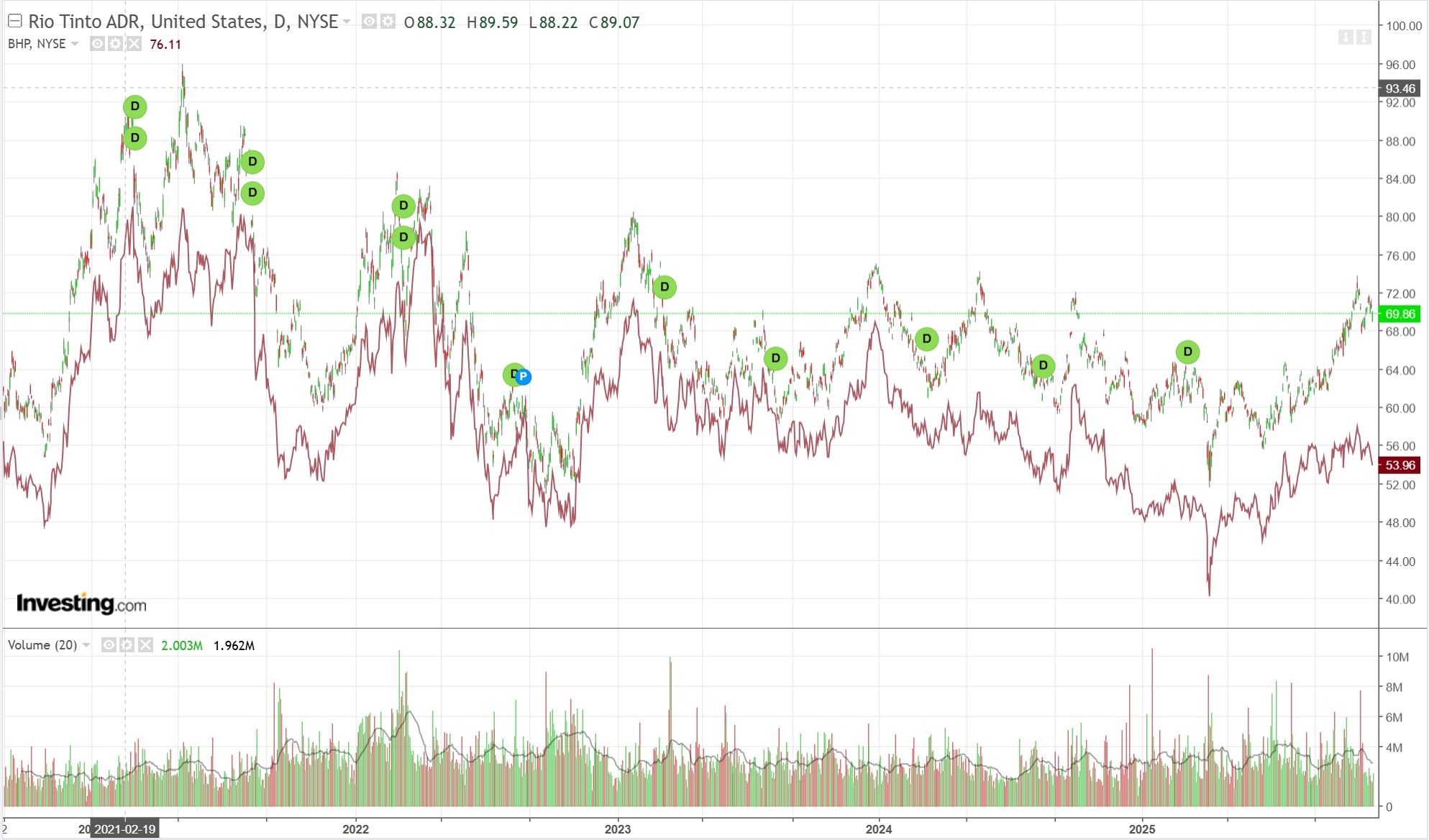

Miners struggle.

Ditto EM.

Junk is a problem for risk, even based on crowding out.

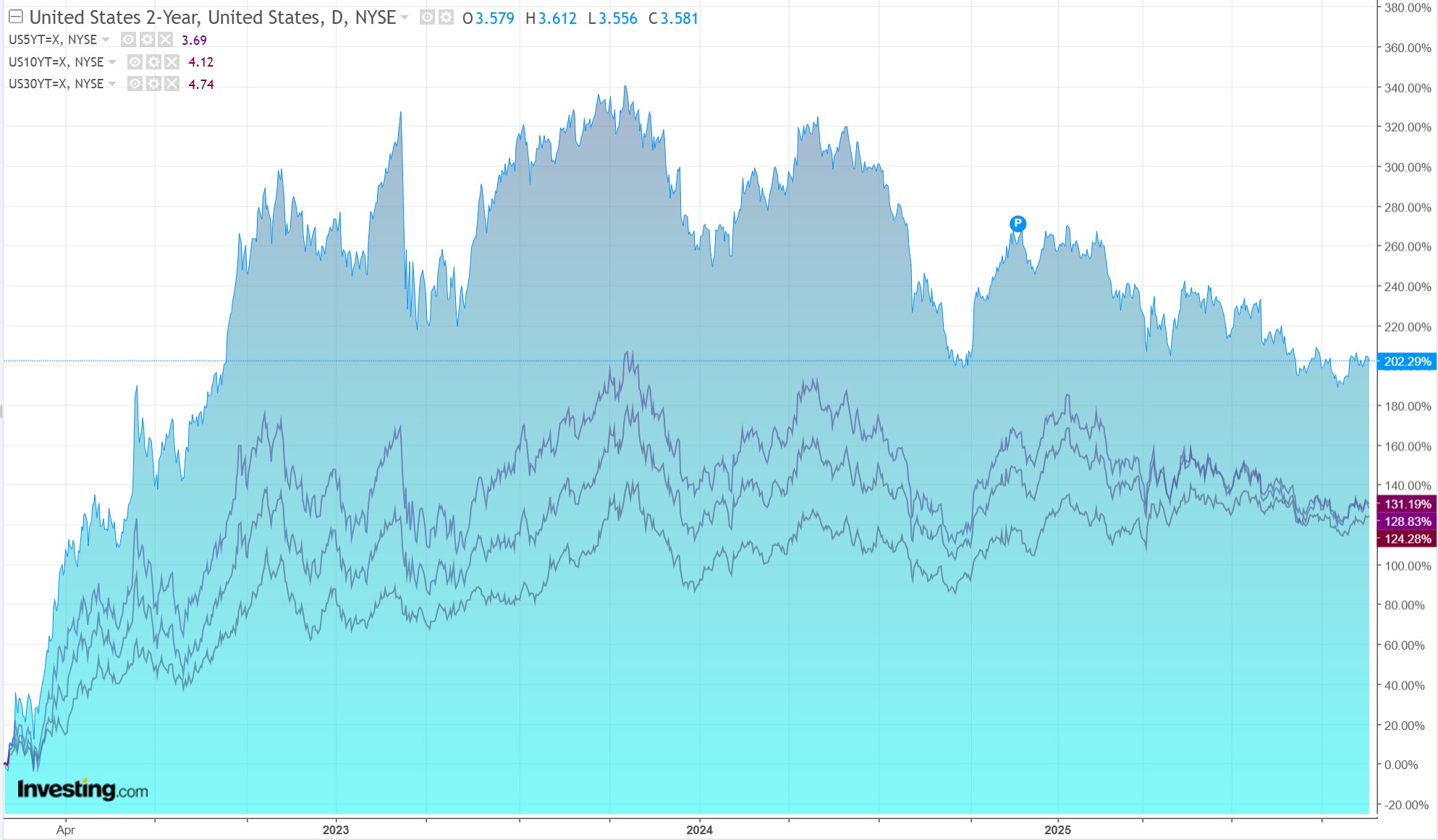

Yields firmed a bit.

Stocks are triggering CTA sells.

RBC has its monthly wrap.

Over the past month, AUDUSD has been driven by diverging central bank paths and commodity-linked sentiment.

The Reserve Bank of Australia has maintained a hawkish stance, keeping rates steady at 3.6% and signaling that core inflation remains undesirably above 3%, which has underpinned the Aussie.

However, this support has been partially offset by broader dollar strength and risk-off sentiment stemming from U.S.-China trade tensions, weaker Chinese export data (October’s steepest drop since February), and volatility in global equity markets.

The pair has largely traded within a 0.6474–0.6625 range during the October-November period, with movements reflecting the tension between RBA resilience and risk-sensitive flows tied to China weakness and U.S. economic uncertainty.

Looking ahead, the near-term outlook for AUDUSD remains conflicted and range-bound.

Technical analysis suggests support around 0.6505–0.6520 and resistance near 0.6600–0.6629.

A close above 0.6615 could confirm renewed bullish momentum.

The key variables going forward will be Chinese economic data, which strongly influences commodity prices and thus AUD valuations, along with any policy shifts from either central bank in early December.

Markets still price in one additional RBA rate cut, most likely in May 2026, but that remains contingent on inflation moderating further.

Until clearer directional catalysts emerge, we expect consolidation within the established trading range with elevated volatility around economic data releases.

I am inclined to see AUD as soft before the Fed on December 9-10 or perhaps the NFP on December 5.

Most signals remain weak for US jobs so the odds favour another cut, and off we go again.