DXY held last night.

AIUD lifted anyway.

CNY meh.

Gold yeh.

Are all metals AI now?

The chosen one returns.

EM meh.

Is a downtrend forming in junk?

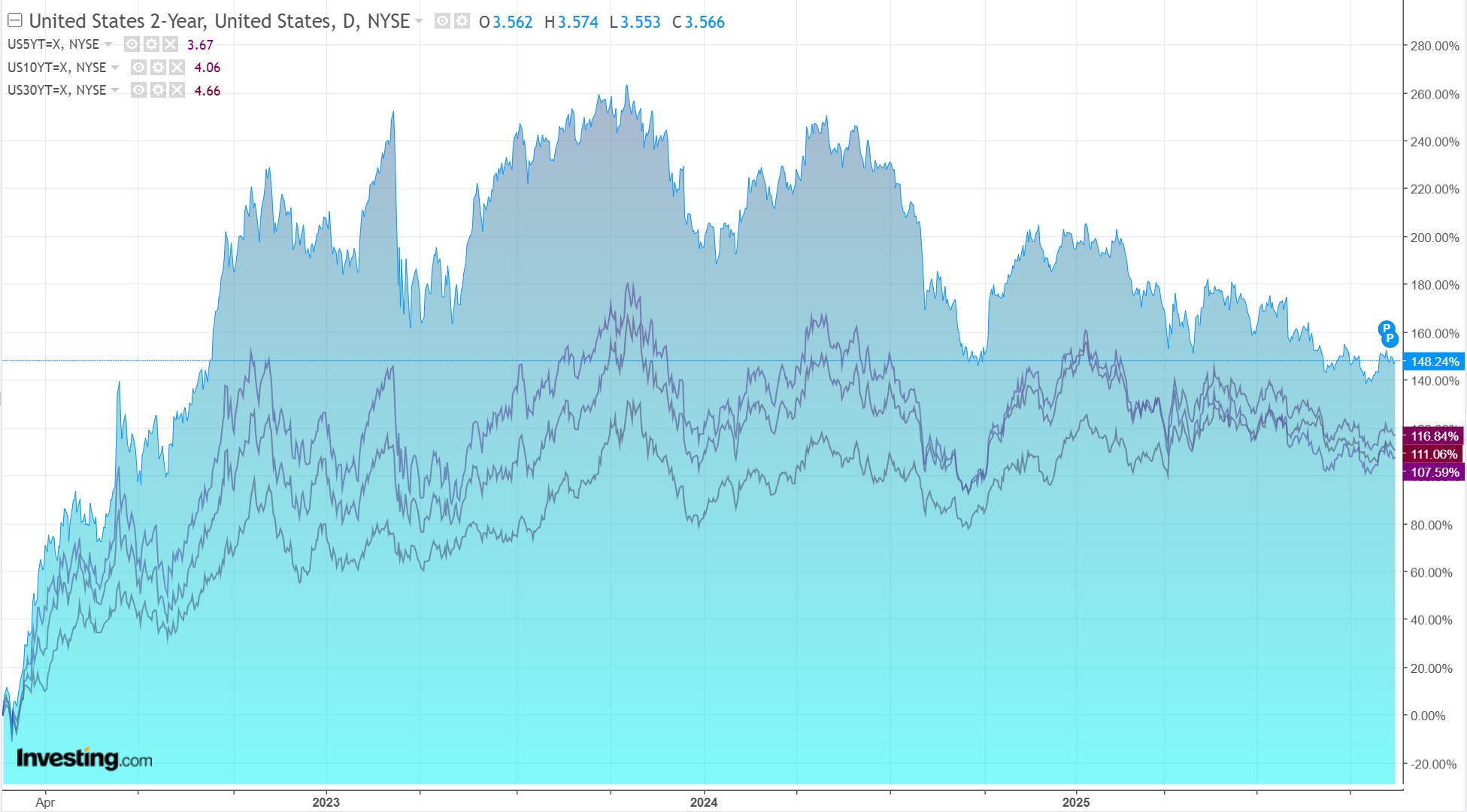

Yields edged up.

Stocks edged down.

The US isn’t going to publish shutdown CPI or job numbers, straight out of Xi Jinping’s playbook. Helping gold.

Credit Agricole has the wrap on AUd.

The Australian rates market pricing for the RBA has swung widely in the past month.

A weak labour market data release followed by a high inflation print and a hawkish shift by the RBA has seen the market swing from pricing in two more 25bprate cuts by mid-2026 to currently pricing in a bit over half a 25bp rate cut over the same period.

AUD/USD has also swung about with this pricing but continues to also be a function of the USD.

AUD/NZD has been where investors have gone in FX markets to express their RBA view, and currently the market is long the cross. Australian labour market data released on Thursday will be a test of these positions.

Following a hawkish speech by RBA Deputy Governor Andrew Hauser on Monday about the Australian economy’s capacity constraints, the labour market needs to start loosening in order for the market and the RBA to believe there is mounting excess capacity in the labour market that would allow further rate cuts.

Weakening job advertisements and business hiring intentions of business suggest further softening in Australian employment growth.

Australia’s financial sector has also been retrenching workers, and these job losses could begin hitting the labour market data in the October data.

The September labour market data showed slowing employment growth, which was unable to keep up with the rise in jobseekers, leading to a jump in the unemployment rate to 4.5% from 4.3% and the highest in nearly four years.

The market looks for some retracement in the unemployment rate back to 4.4% , which would be in line with the RBA’s improbable flat trajectory.

That is the sensible view, but who knows with employment reports? The trend remains up, in my view.

As for capacity constraints, all the RBA is doing is making room for gas cartel cost-push inflation.

There is ZERO evidence of wage-push inflation. Wage growth is moderate and falling.

Labor unit costs are being inflated by the gas cartel’s destruction of profitability across the economy.

The new RBA is worse than the old RBA, which is partly why the AUD is weaker than it should be.