DXY is breaking out in the nightmare scenario for everybody.

AUD was monkeyhammered.

CNY is gassed.

Gold and oil no bueno.

AI metals no more.

The chosen one gaps into madness.

EM yeh, nah.

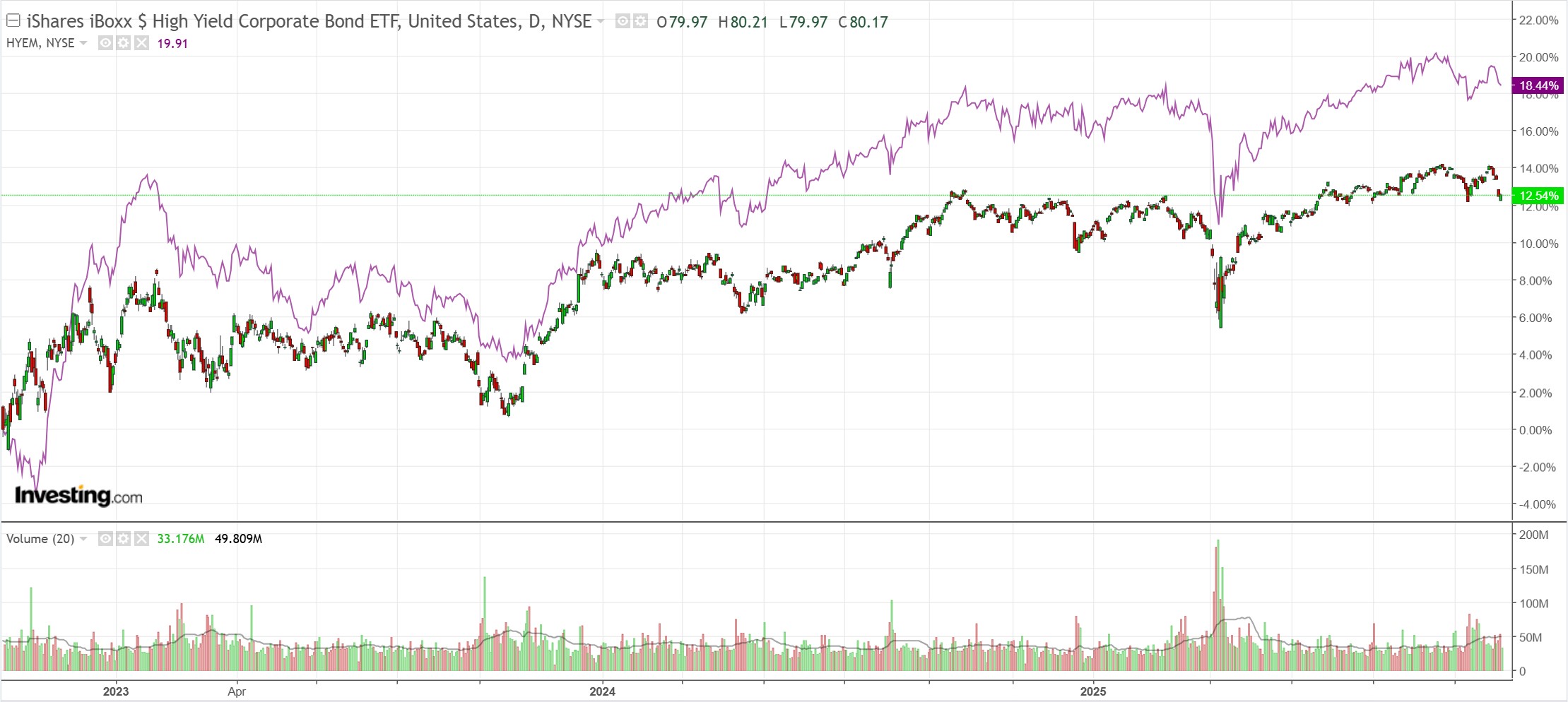

Junk knew.

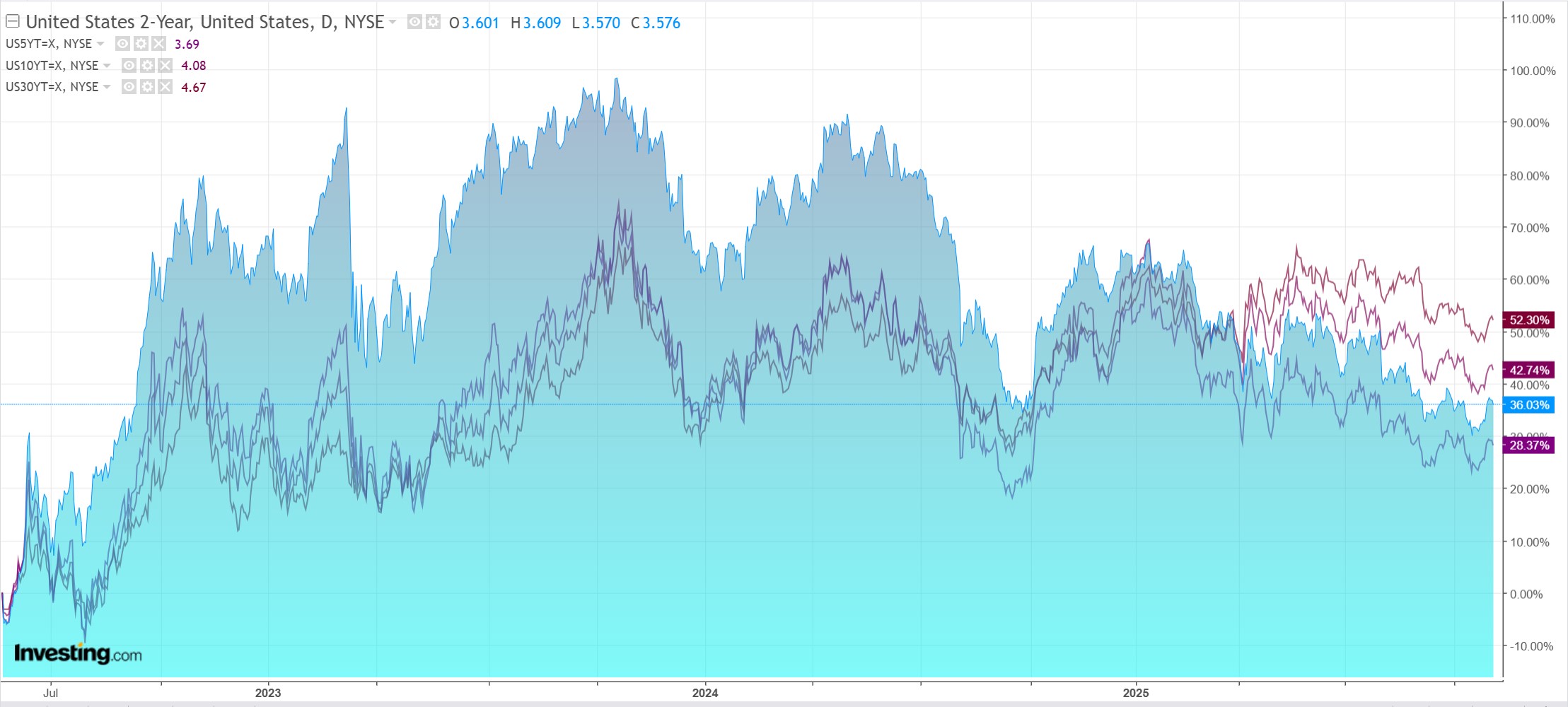

Yields offer hope.

Stocks did a gold.

There is nothing this market hates more than a rising DXY. One might expect the AUD to be holding up better given the suddenly hawkish RBA, but the forex market is voting with its feet for policy error.

There is no more interest-rate-sensitive economy in the world, and given the RBA can’t do anything about cost-push inflation coming out of the gas cartel, trying to do something is a rather stupid idea. PIMCO.

“We think the RBA will likely cut more than once in 2026 on its path toward a neutral policy setting, which we estimate to be around 3%,” Bowe said. While the RBA is in a difficult position, “ultimately the evidence will build for them to get comfortable in lowering rates next year.” Pimco’s Australian bond fund has beaten around 95% of peers in the past year.

Pimco, however, is taking the opposite view. The firm remains overweight Australian debt, with Bowe noting that monetary policy is “still tight.” He expects the labor market to weaken further and inflation to moderate as the RBA remains on hold before making multiple cuts next year.

I agree. There is further to run in this round of energy shock, but the RBA’s notion that labour costs have driven the inflation pop is stupid as unemployment rises.

The RBA risks a curve flattening here as weak growth gives way to stalling on its misdiagnosis of the inflationary causes.

Take this, for instance:

Bullock noted the pick-up in inflation in new dwellings and market services – which are expected to be more persistent – suggest that there is still excess demand in the economy.

Building materials are very electricity and gas intensive. Market services are less so but obviously exposed.

By next year, Chicken Chalmer’s Ukraine War 2.0 energy shock will be over:

Freeing the RBA to resume cuts into an energy-battered economy.

All we needed was gas reservation to prevent it all.