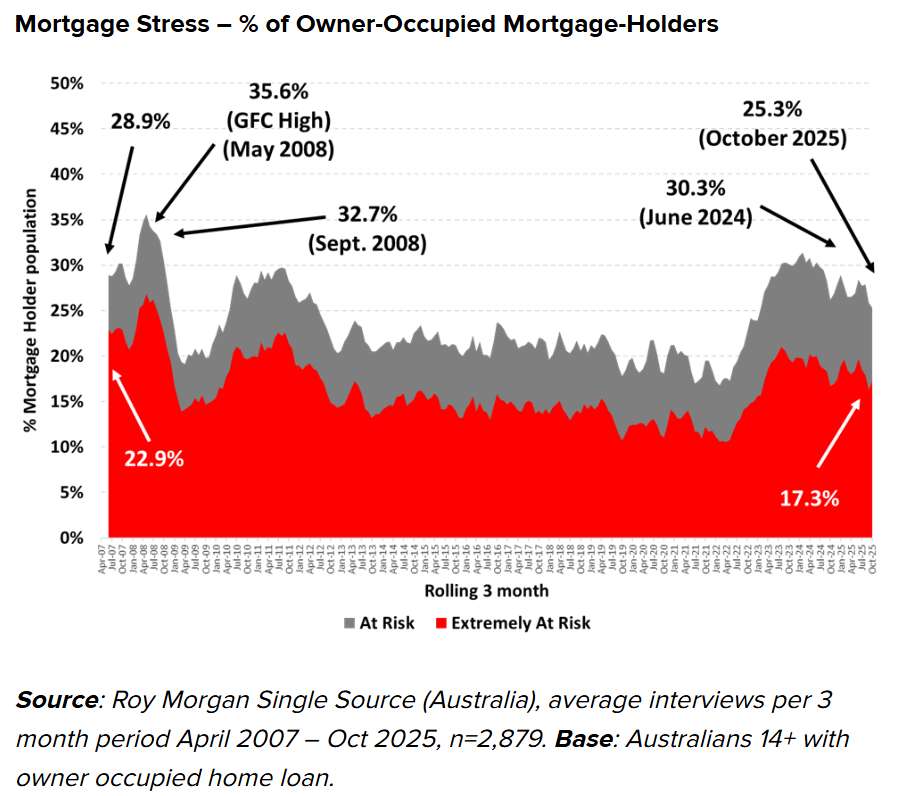

Roy Morgan reported that mortgage stress hit its lowest level since February 2023, following the three 0.25% rate cuts from the Reserve Bank of Australia (RBA).

In the three months to October 2025, 25.3% of mortgage holders were deemed by Roy Morgan to be ‘At Risk’ of ‘mortgage stress’, down 2.6% points from August 2025 and well below the 30.3% peak in June 2024.

Even so, 518,000 more Australians were deemed to be ‘At Risk’ of mortgage stress three years after interest rate increases began, from just 0.1% to a high of 4.35% from November 2023 until February 2025.

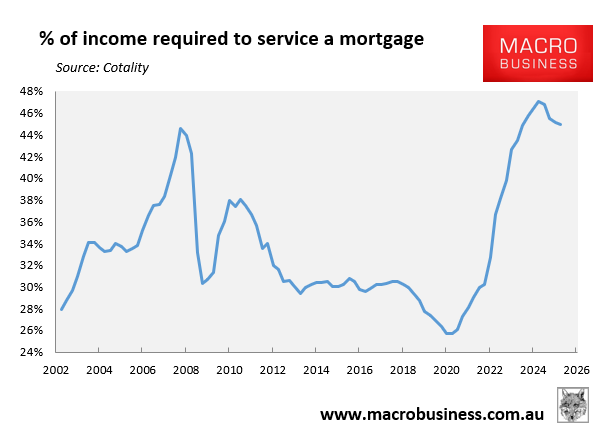

This week’s housing affordability report from Cotality supports Roy Morgan’s findings.

Cotality showed that median mortgage repayments as a share of median household income have fallen from a peak of 47.1% in the September quarter of 2024 to 45.0% as of the September quarter of 2025:

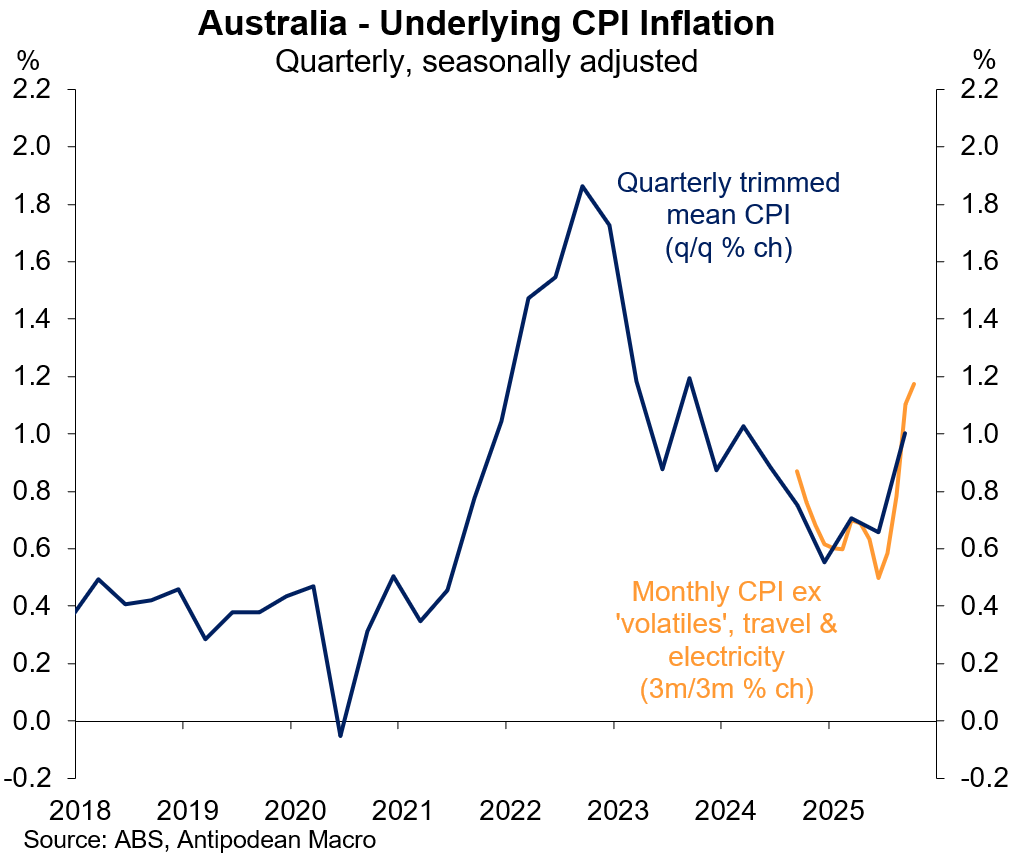

This is where the good news ends, however. As illustrated below by Justin Fabo from Antipodean Macro, Wednesday’s October CPI report from the Australian Bureau of Statistics (ABS) showed that the policy-relevant trimmed mean inflation has shifted higher, tracking above the target range at 0.9% for the quarter and 3.3% annually:

As a result, further rate cuts are off the agenda for the foreseeable future.

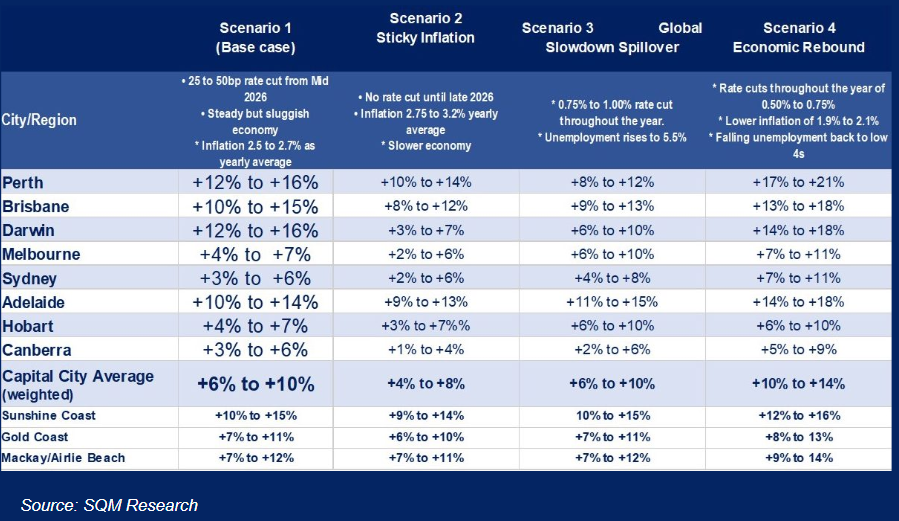

Meanwhile, SQM Research has forecast further robust property price growth in 2026, even in the absence of further interest rate cuts:

Further rises in home values above the rate of income growth without interest rate cuts necessarily mean that the ratio of mortgage repayments to income will increase.

It also means that Australian mortgage stress will climb higher.