What price Australian smelters?

Major global companies like Trafigura, Glencore and Rio Tinto are all negotiating what additional financial assistance federal and state governments are willing to provide to keep aged, uncompetitive smelters operating in Australia.

…China has created a worldwide glut of refining and smelting capacity. That has driven down prices and viability for smelters in other countries while making it even more commercially attractive for miners to just send all their ore or concentrate to China for much cheaper processing.

It’s still clear that Beijing’s current control has undermined support for free trade no matter what G20 leaders say in their communiques. Less clear is the potential price tag to counter China, along with conditions attached by companies as well as governments.

Glencore, for example, will receive up to $600 million to keep its loss-making copper smelter in Queensland open for at least another three years. What then?

The federal and NSW governments are desperately trying to avert Rio Tinto’s planned closure of its Tomago aluminium smelter in NSW in 2028 due to energy costs. Yet power prices aren’t going anywhere but up.

Are they, really? Do power prices have to go up? No.

They can come down. A lot. If we implement a straightforward reform to regulate the gas price, we can expect a 40% reduction in wholesale electricity prices, equivalent to 40% of the average bill.

Other retail bill costs will rise incrementally. Network charges (40% of the average bill) will increase as the rollout of renewables continues, as will environmental charges (e.g. renewable energy certificates). But it will take a long time, and, assuming other nations embrace the climate challenge, it will not undermine Australian competitiveness.

Given our cheap gas advantage, it should increase our competitiveness.

Why would we subsidise smelters when we can do so much more easily by lowering the energy bills that are killing them?

This is particularly true given that the same reform will alleviate Australia’s cost-of-living shock in food and housing, while also reviving a wider range of industries.

If executed correctly, this reform can not only repair the budget but also alleviate unnecessary financial burdens by finally taxing the East Coast gas cartel fairly.

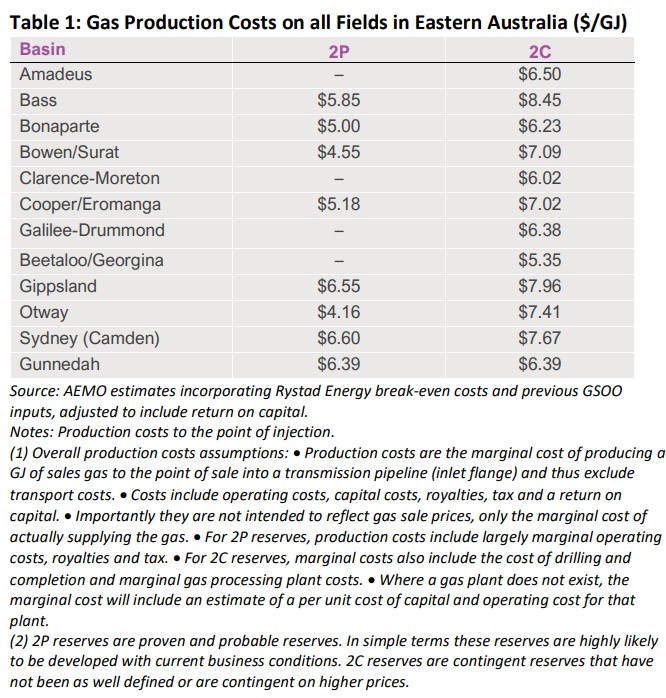

How should the gas price be lowered? Apply a 100% levy on every gas molecule exported at a price above $7Gj.

This automatically lowers the local price to $7Gj, resulting in a 40% decline in wholesale power costs.

For the industry, it also delivers 60% savings in gas costs.

This would buy us a lot of time for cost-effective energy transition, including time for battery prices to come down further and enable ongoing cost reductions in decentralised clean power options, which would limit the spending needed for network expansions.

And it collects tens of billions for the budget while not triggering any sovereign risk, given LNG exporters are profitable at $7Gj.

With any luck, it would also trigger GLNG to declare force majeur and recontract the supply of its export contracts to the US or Qatar, where cheap gas is going to flood the market two years hence.

This would release even more gas for Australian use and could push prices below the $7Gj threshold.

A gas export levy set at $ 7/GJ is a no-brainer national-interest policy.