By Harry Ottley, Economist at CBA

- It was an exceptionally quiet week in Australia with a drop in consumer sentiment the only data of note.

- RBA Governor Bullock appeared before the Senate Economics Legislation Committee but kept communication very much in line with recent statements.

- Offshore, the US government shutdown continued, delaying key economic releases and the RBNZ cut by 50bp.

- Next week, the September labour force survey will be the local highlight. We also release our September HSI.

- The minutes from the August RBA policy meeting are due and various officials will be on the wires throughout the week.

- Offshore, the dataflow is light with US CPI a highlight albeit it may be delayed due to the US Government shut down.

It was an exceptionally quiet week in Australia. The main local data release was the Westpac–Melbourne Institute Consumer Sentiment Index, which fell 3.5% to 92.1. A decline was expected given August’s higher CPI figures and the RBA’s hawkish tilt.

Cost-of-living pressures remain front of mind after the recent period, so consumers are highly sensitive to negative news on inflation and interest rates. Despite persistently weak sentiment outcomes, household spending has held up thanks to supportive fundamentals such as rising incomes, wealth and lower interest rates.

RBA Governor Bullock appeared before the Senate Economics Legislation Committee this morning, though questioning was largely political rather than policy-focused. Her remarks were consistent with recent communications: inflation appears “sticky” in Q3, but her tone was cautious and calm.

With policy near neutral, the Board can afford to be patient and remains firmly data-dependent. We expect the final cut to the cash rate this cycle in February 2026.

Across the Tasman, the RBNZ cut rates by 50bp, in line with our ASB colleagues’ out-of-consensus call. The divergence between the two Antipodean economies is stark: while Australia is still focused on inflation and a still tight labour market, New Zealand policymakers are grappling with how to close a large and expanding output gap.

ASB expect one further rate cut to 2.25% in November, but with the clear risk being the cash rate going even lower.

Globally, the US government shutdown continues, but markets have largely shrugged off delays to key data releases. Analysts remain comfortable with the view that the US labour market has slowed enough to justify further FOMC rate cuts.

In Europe, France faces renewed political turmoil following Sébastien Lecornu’s resignation, while hopes for an end to the Israel–Hamas war pushed global oil prices lower.

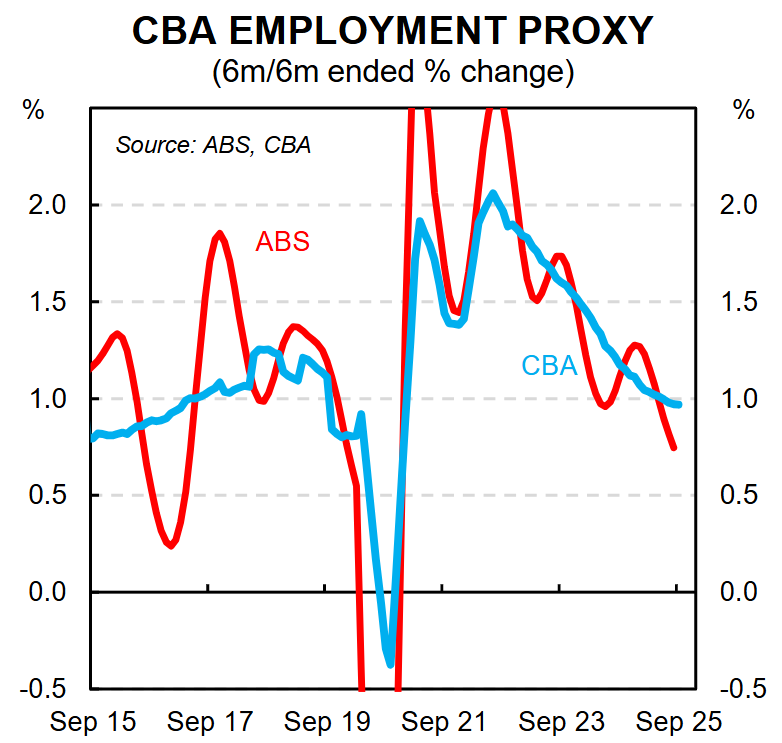

Next week, attention will turn to the September labour force survey. Recent months have been marked by weak employment growth, though lower participation has kept the unemployment rate’s rise modest to 4.2%. That said, the survey can be volatile.

Our broader view is that elevated job vacancies and a strengthening private sector suggest enough jobs can be created to prevent the unemployment rate from climbing much further. Our internal data reinforces our confidence that employment growth remains solid, suggesting the recent weakness in official figures may reflect some noise rather than a true trend.

RBA communication will also be in focus. Minutes from the September meeting are due Tuesday; we expect few surprises but will look to assess how the hawkish tone in the statement translates to the minutes.

The RBA Governor and Chief Economist will speak at separate events, though neither is likely to stray far from the current song sheet.

We will release our CommBank Household Spending Insights report for September on Thursday. The index picked the improvement in consumer spending earlier in the year and has shown consistently solid spending outcomes in recent months.

The NAB Business Survey is also due next week with both conditions and confidence sitting at around long-term averages.

Offshore, US CPI and retail sales are the key data highlights—though these may be delayed if the shutdown persists. UK labour market data and China’s consumer and producer prices are also scheduled. New Zealand has a busy calendar; see inside this documentfor full previews.