The case against RBA rate cuts strengthens

This month, the Reserve Bank of Australia (RBA) decided to hold the official cash rate at 3.60%, citing resurgent inflation risks.

The RBA’s statement alongside its decision noted that “the decline in underlying inflation has slowed”, with “recent data, while partial and volatile, suggest[ing] that inflation in the September quarter may be higher than expected at the time of the August Statement on Monetary Policy”.

Following the decision, economists and financial markets have lowered their expectations of interest rate reductions, with the latest interest rate futures pricing implying that only one additional 25 basis point cut will be delivered:

Financial markets currently ascribe around a 50% probability of the RBA delivering a 0.25% cut at its November meeting.

Recent data has strengthened the case against further rate cuts.

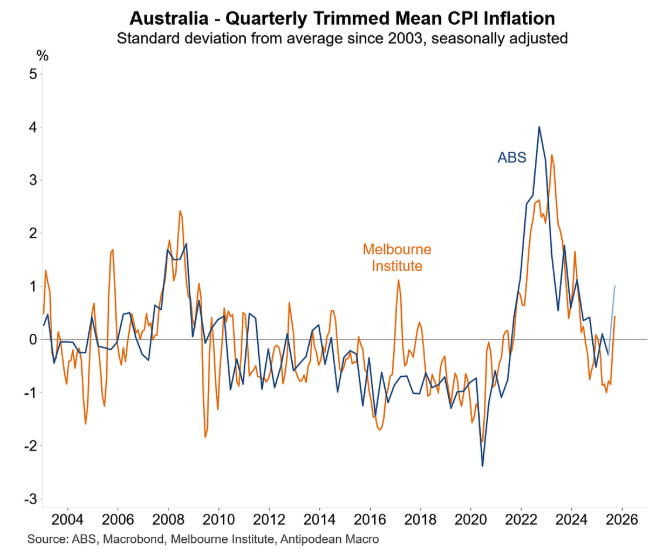

The Melbourne Institute’s inflation gauge for September, presented below by Justin Fabo from Antipodean Macro, reported that trimmed mean inflation has reaccelerated recently, which Fabo believes will be met with a commensurate rise in ABS trimmed mean inflation for Q3 (Fabo’s forecast is shown in light blue).

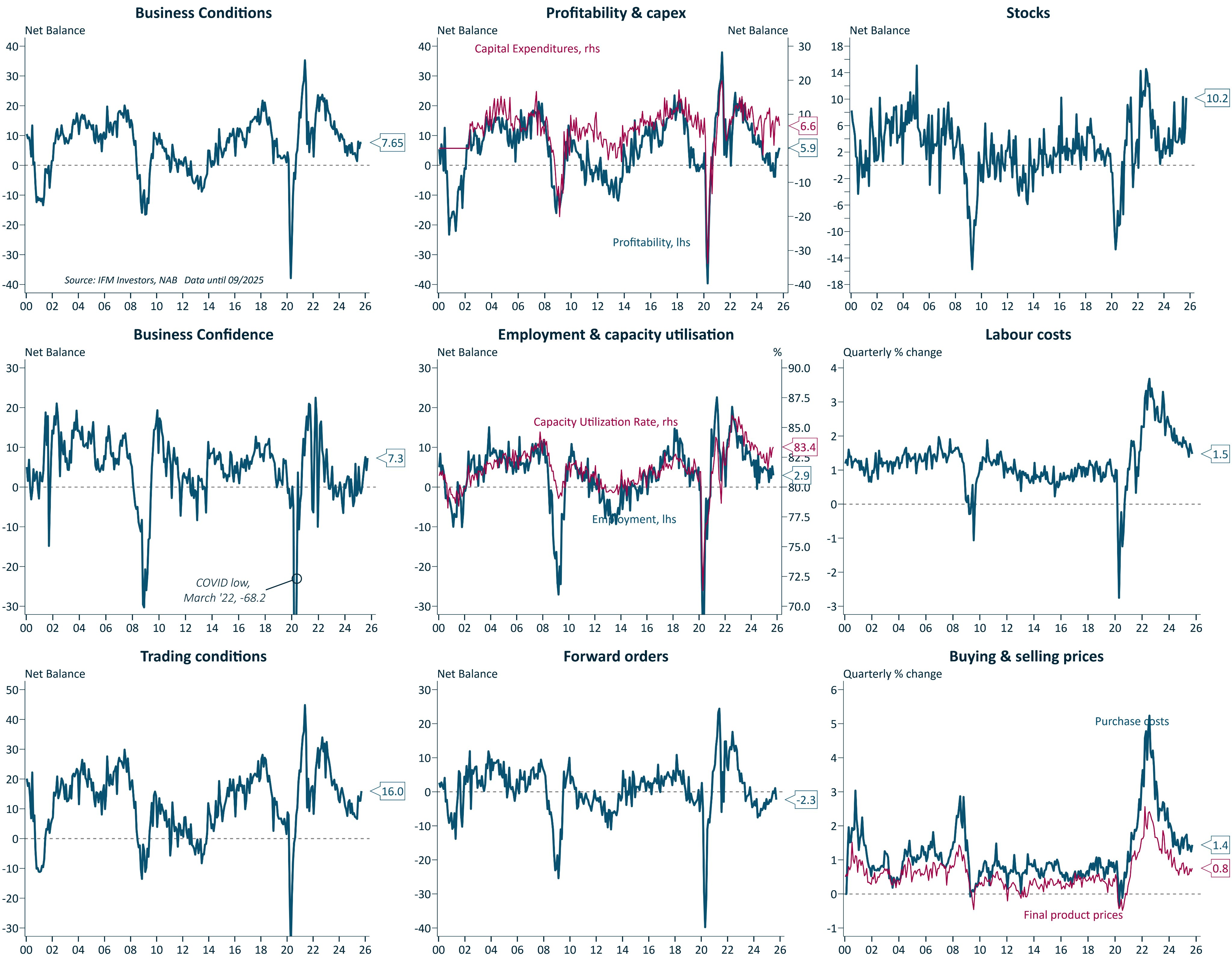

This week’s release of the NAB business survey for September suggested that the economic environment is improving.

Source: Alex Joiner (IFM Investors)Alex Joiner, chief economist at IFM Investors, summarised the results as follows on Twitter (X):

“NAB business survey remains solid. Conditions are holding and confidence is rising. Capacity utilisation is edging higher, employment is okay, trading conditions have improved”.

“Forward orders were the one negative, partially retracing some good recent progress. Inflation measures are well-behaved”.

“Overall the survey doesn’t scream that further rate cuts near-term”.

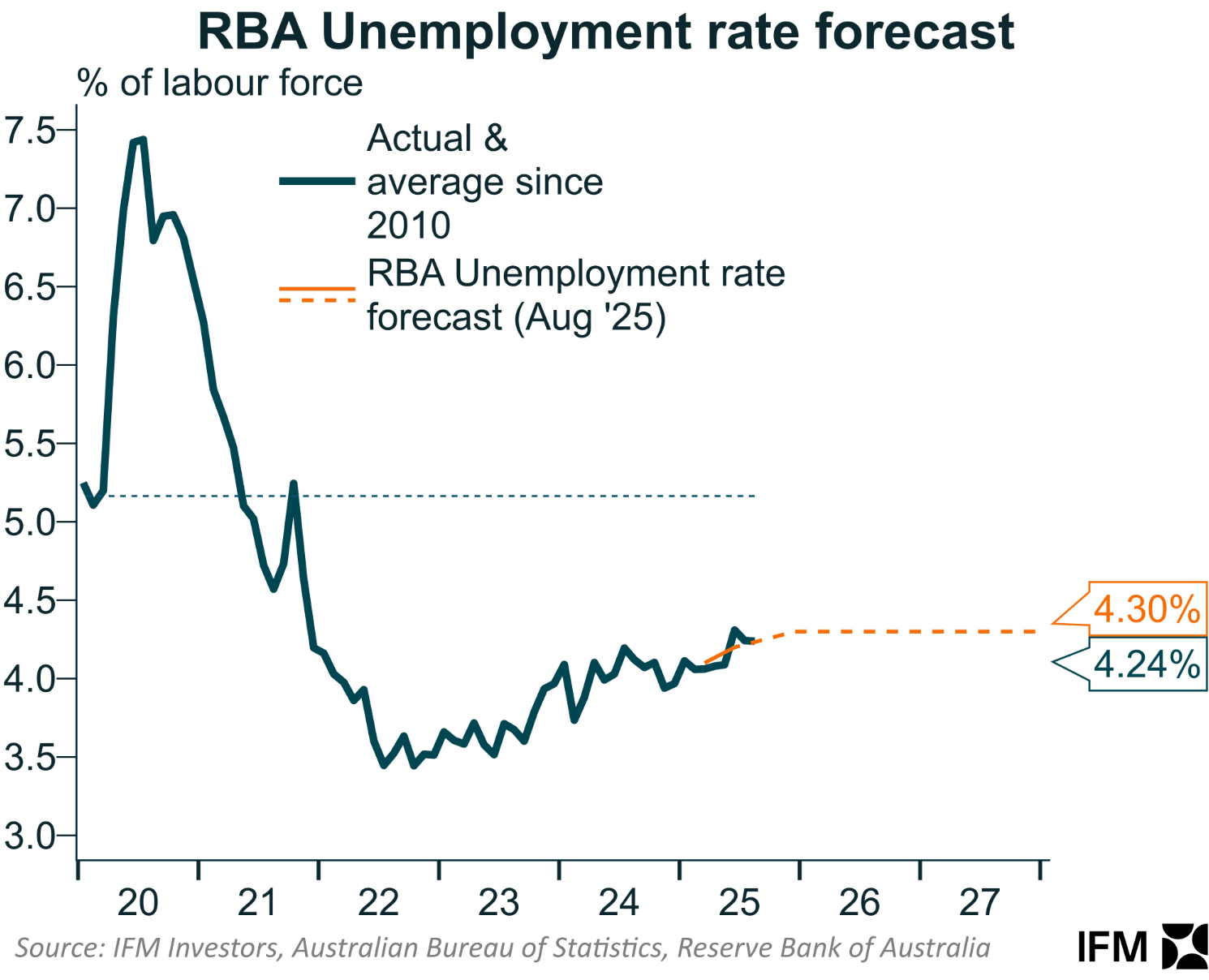

The one area that could prompt the RBA to cut sooner and further than anticipated is if the nation’s unemployment rate rises faster than the RBA anticipates.

The RBA forecasts that the nation’s unemployment rate will remain at its current level for the next two years, which seems optimistic.

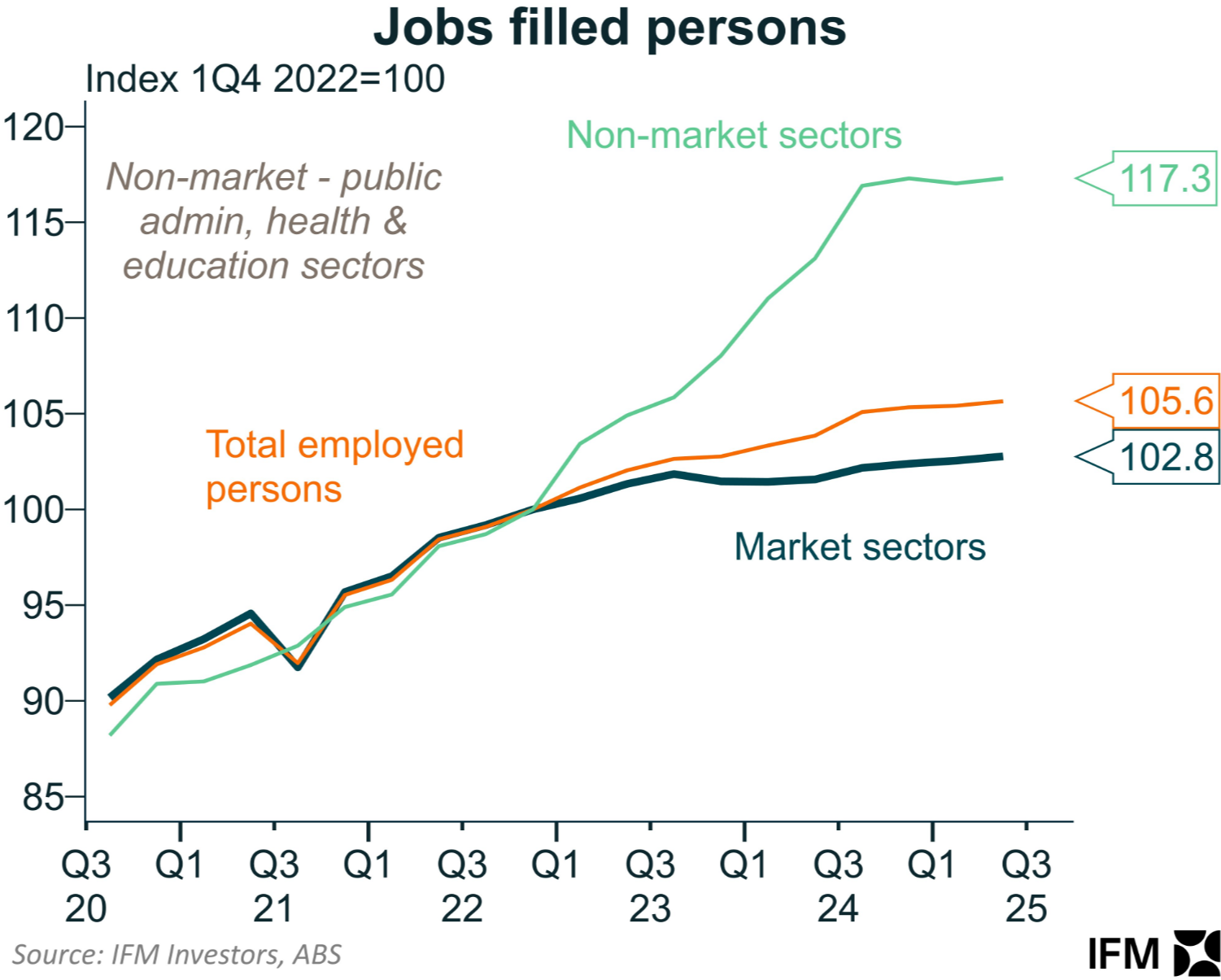

Since the pandemic, the non-market sector, primarily the expansion of the NDIS, has driven the majority of Australia’s job creation, a trend that has never been sustainable.

Therefore, there is the clear and present danger that job creation will stall and unemployment will rise if the private sector does not expand sufficiently to compensate for slowing growth in the non-market sector.

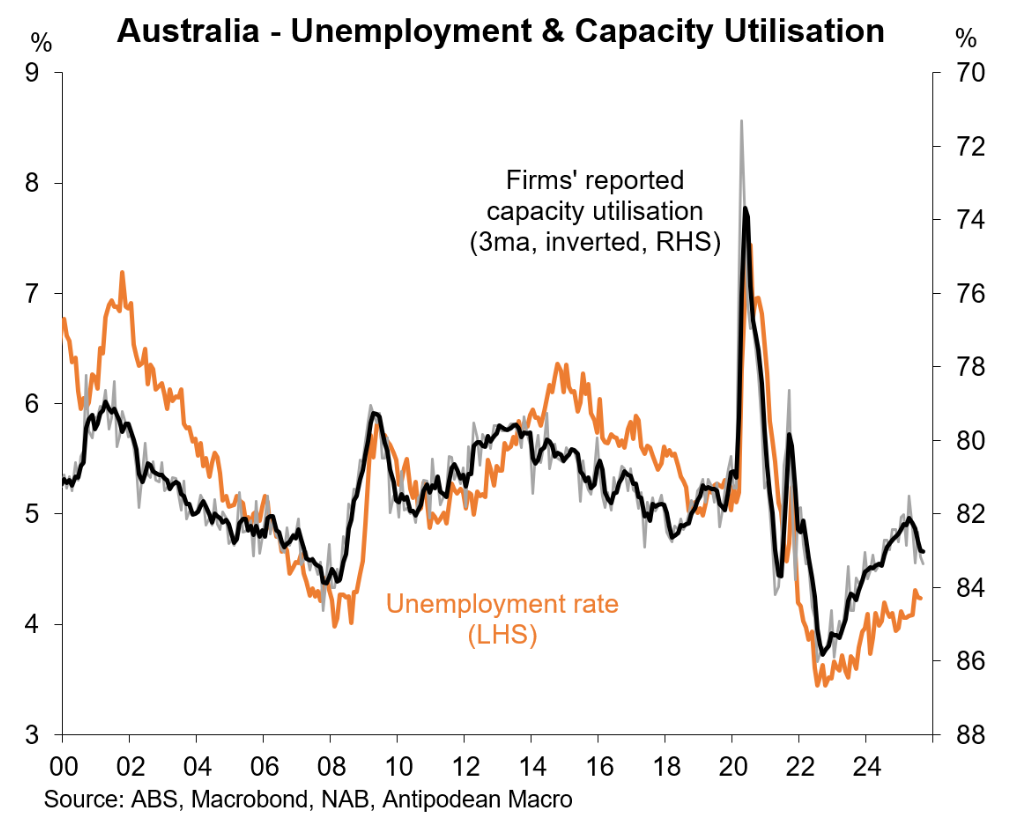

However, as illustrated below by Justin Fabo from Antipodean Macro, the rise in capacity utilisation shown in the NAB Business Survey suggests that the unemployment rate may actually fall in the near term:

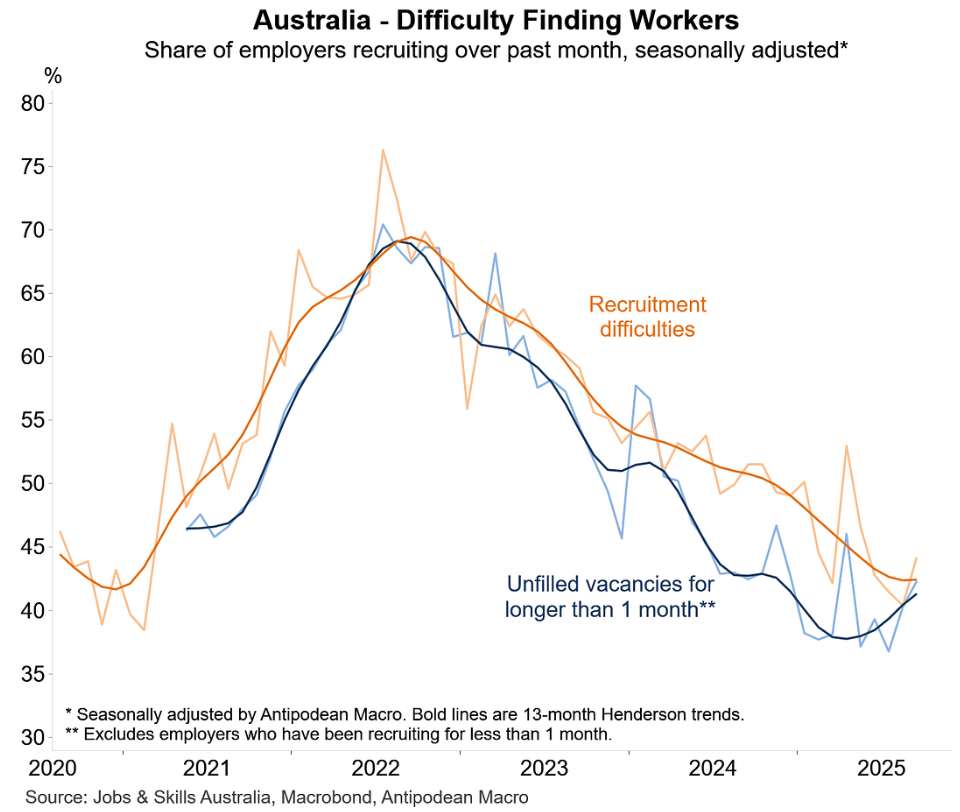

The employer survey by Jobs & Skills Australia for September also revealed an increase in reported recruitment difficulties; albeit following a period of declines:

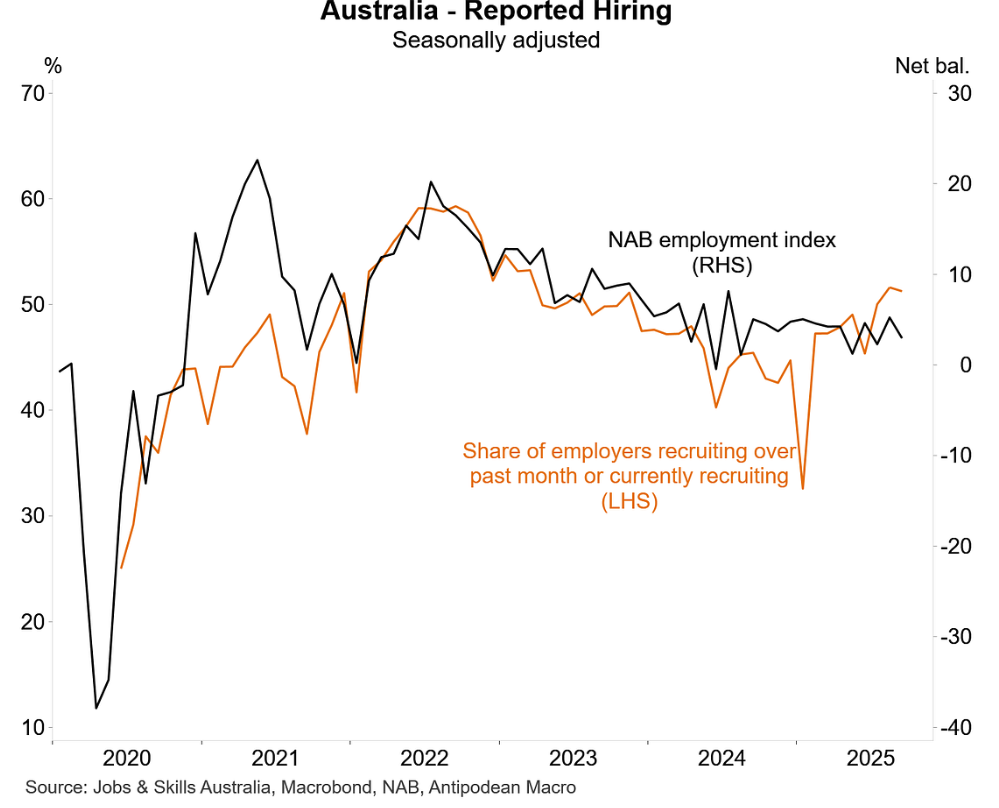

Justin Fabo also shows that the share of employers currently or recently recruiting has increased in recent months:

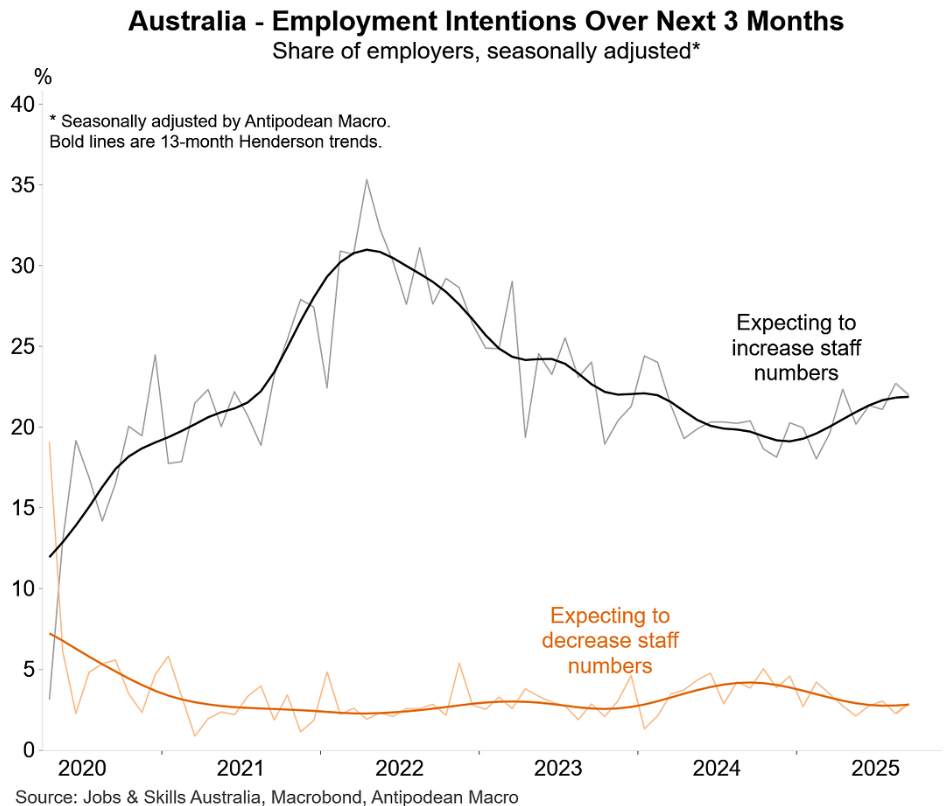

A rising share of Australian employers expect to increase staffing numbers in coming months:

None of which suggests that the labour market is weakening materially or points to rate cuts.

For these reasons, the RBA’s latest minutes, released on Tuesday, state that the board’s decisions will remain “cautious and data dependent”.