DXY is back.

AUD is being sat on by an elephant.

CNY did like the trade truce.

Gold is trying as the Fed hawked up, expecting Trump to go nuts.

AI metals falmed out with AI.

Big miners shooting star.

EM too.

Junk no bueno.

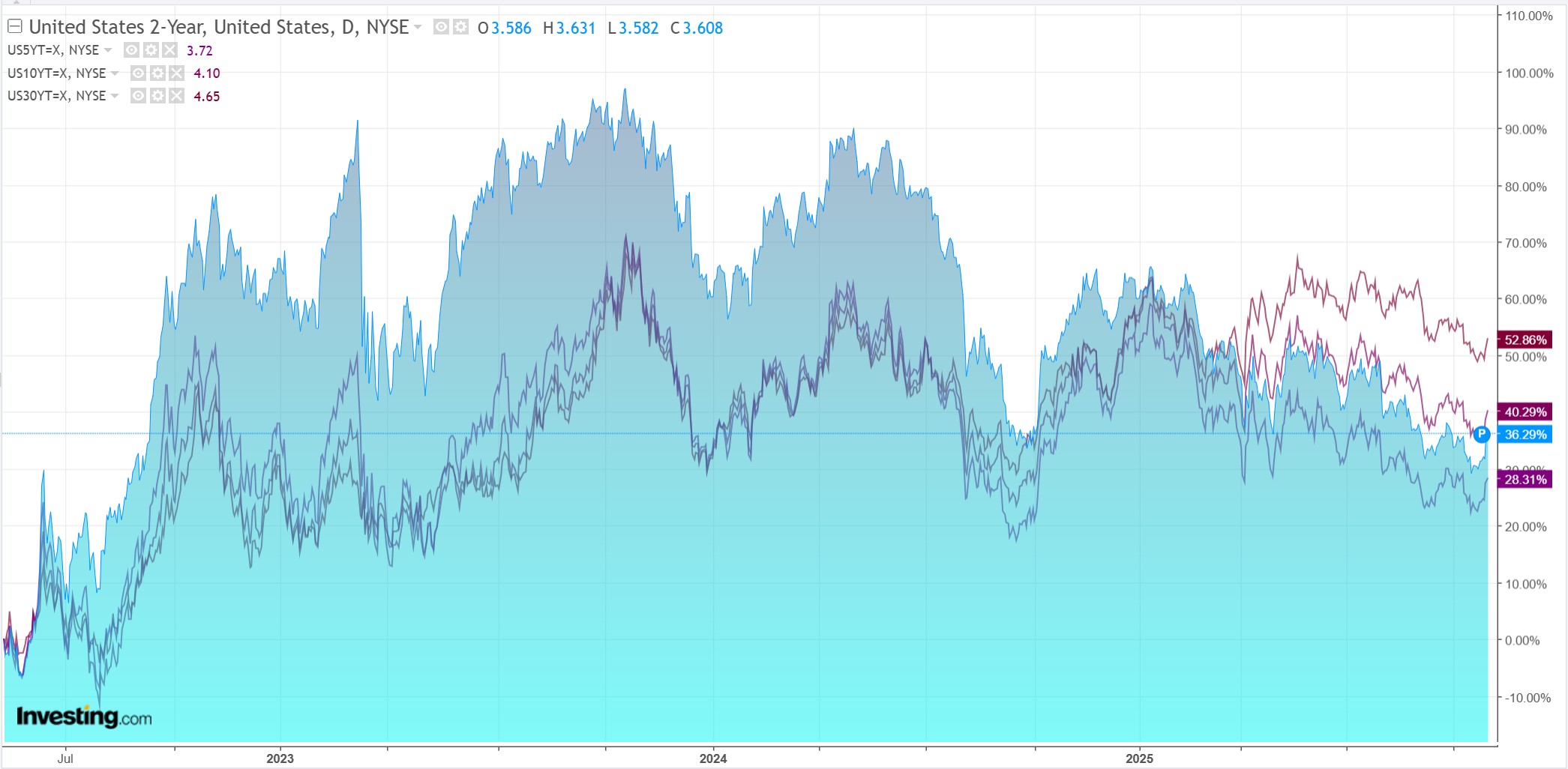

Yields back-up.

Tech dwn.

Charlie McElligott sums it nicely.

Jerome Powell bought-back “some” Fed rate path optionality yday with usual “both sides of mouth” cross-speak—as well as a touch of gaslighting—to push against what had become a rather “tilted” dovish expectation into the meeting (which IMO bears the mark of SOME “lame duck” with the “old guard” trying to muck-up the picture on his way out in Spring ‘26, but at the very least points to potential for widespread dissent votes on next year’s FOMC as a future Rate Vol catalyst—“…strongly differing views today” but only 2 dissents, ehhh?!).

Yet despite his downplaying the certainty of a Dec Fed cut (still the modal expectation @ ~72% “priced” on the implied prob distribution), the market believes the Trump Admin will ultimately get their desired lower rates in ’26 and beyond regardless, “by hook or by crook”…so you’re kinda just shifting the distribution towards the new “future” Fed Chair.

At the core of the JP “reintroduction of optionality” yday was this idea of the Fed “driving in a fog” without econ data due to the govt shutdown, which Powell says merits caution from the FOMC…Yet to say lack of data visibility gives him pause to cut—when today he cut with no data!—just doesn’t hold water.

In USD Vol, I will say that the crowded Short in Upper Left Payer Ladders could get spicy if the “Hawkish” thing further metastasizes, with 1) Dec hypothetically (for now) being a “Live Meeting” and 2) potential for “light at the end of the tunnel” with the Govt shutdown I believe in the next two weeks (with pressure on Dems building on the SNAP impact and the Govt worker unions calling for movement), which then would mean 3) reintroduction of US Econ data risk thereafter.

In short, for now, the Fed has reintroduced the market to risk via possible hawkishness on inflation. But Trump tanty 765.0 will end that before long, which is good for gold, though a rising DXY ain’t.

For now, a risk-fueled DXY is bad for AUD despite the local central bank being even more hawkish.