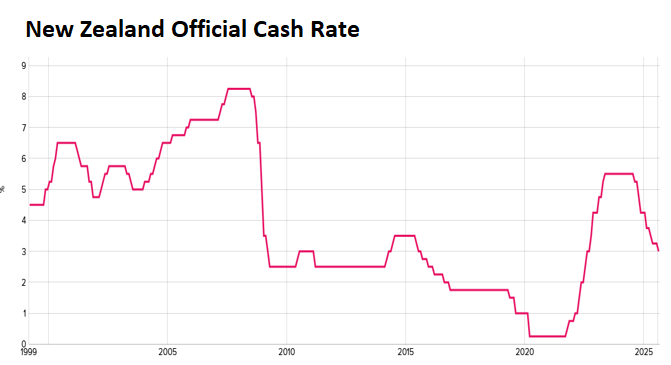

The Reserve Bank of New Zealand has already delivered 2.5% of interest rate cuts, which has taken the official cash rate to 3.0% from a peak of 5.5%.

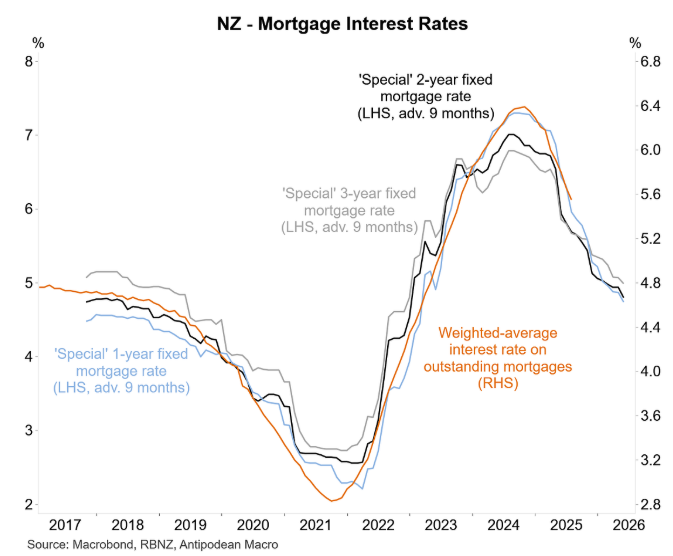

As illustrated below by Justin Fabo from Antipodean Macro, the Reserve Bank’s monetary easing has lowered new mortgage rates to pre-pandemic levels, whereas weighted-average interest rates on outstanding mortgages are lagging behind:

Despite the sharp interest rate cuts, New Zealand’s economy remains in a funk, suffering from high unemployment and excess capacity.

As a result, major bank ASB believes that the Reserve Bank will deliver a series of additional rate cuts in a bid to bolster demand.

ASB expects the Reserve Bank to cut the official cash rate by an outsized 50bp at this week’s meeting, although it admits the market has only priced a 33bp cut. ASB also expects a further 25 bp rate cut.

“The fire of recovery needs more accelerant. The OCR needs to go lower than recently thought, to a low of 2.25%, to get monetary conditions more into stimulatory territory”, ASB wrote in its monetary policy meeting preview.

“The room for regret is shifting from the risks of inflation being more persistent than expected, towards the risk of economic recovery getting bogged down and spare capacity lingering for too long”.

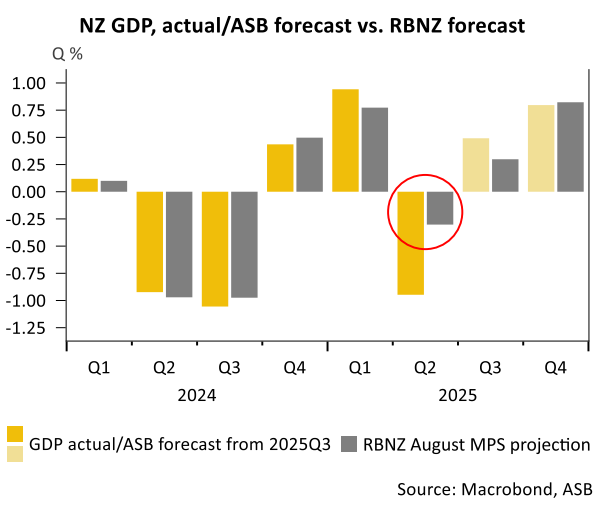

In coming to its position, ASB noted that “the economy lost a lot more momentum than anticipated over Q2” and that it is “mainly down to interest rates getting low enough to entice households and businesses to spend and invest”.

“Q2 GDP rammed that message home: even if you can discount some of the weakness as statistical quirks, 10 of 16 industries still contracted”.

ASB also pointed to “wider signs of the economy’s sputtering momentum, such as the Business NZ/BNZ manufacturing and service sector surveys (which are proving more reliable than the ANZ monthly business survey) that still point to flat/contracting activity”.

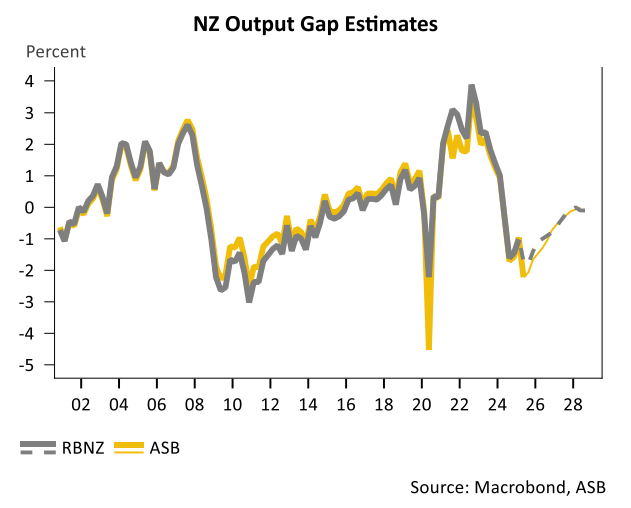

As a result, “the weak economic recovery to date suggests a lot more spare capacity in the economy, at least as measured by the GDP-based output gap (which compares the level of activity to where it ‘should’ be sitting if the economy was operating at full capacity)”.

“This measure suggests the degree of spare capacity is as large as it was when NZ was hit by the full force of the Global Financial Crisis”.

ASB, therefore, has called on the Reserve Bank “to Set Fire to the Rain” and deliver another 75bp of easing to refire demand and to close the output gap.