So says Societe General.

The AU unemployment rate jumped to 4.46% in September, above any of the Bloomberg survey forecasts.

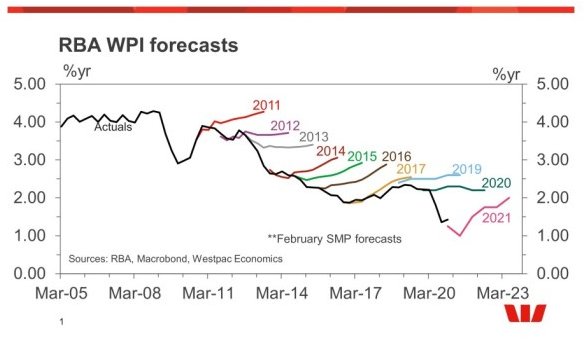

An upward revision to August leaves the average 3Q rate in line with the RBA’s latest SoMP view of 4.3%.

However, the uptick skews risk higher for 4Q.

Markets have been wrong-footed by single prints before (see: June) though this softening is in keeping with modest declines of job ads in one of ‘leading indicator’series that the RBA puts weight on, adding to credibility.

With rates still ‘somewhat restrictive’ and a desire to preserve job gains, there is a strong case for an ‘insurance cut’ in November to 3.35%, assuming the worst tail in quarterly CPI (1% QoQ) is not realised.

Terminal rate pricing is now close to 3.10%.

We expect this area to be sticky, given (i) the RBA may drop the ‘restrictive’ moniker after the next cut, (ii) inflation risks coming from housing and services, and (iii) broader forward indicators still look overall resilient.

Yawn. Same old consensus-hugging drivel. MB was not surprised by the jump in unemployment. Why? Because we have the intellectual credibility to discuss immigration.

Unemployment is going higher and rates lower. Lower than a terminal of 3.1%. It will be somewhere with a 2-handle. It would be lower still without the gold boom.

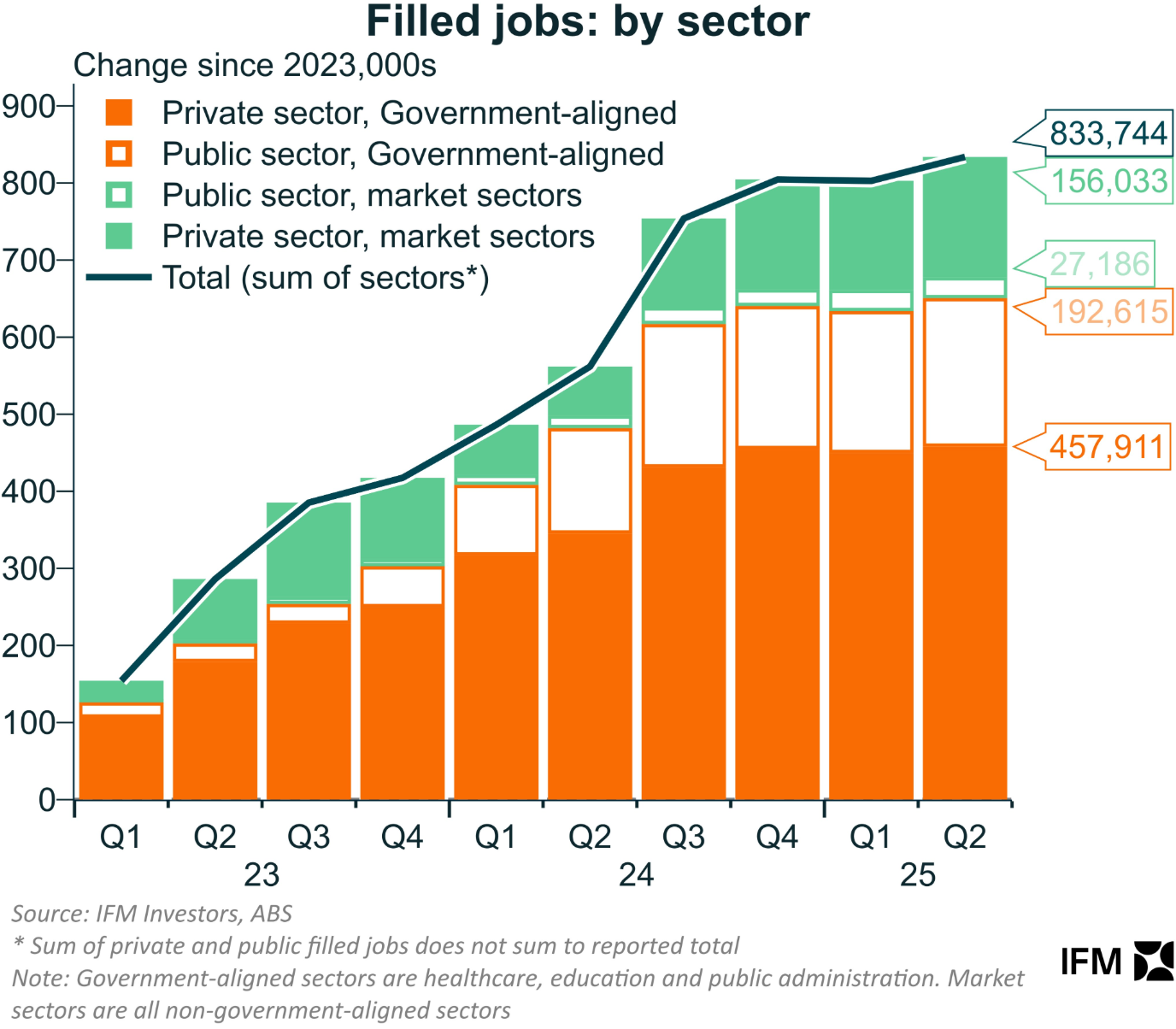

Immigration is still booming, meaning the breakeven rate for job growth is somewhere around 30k per month.

But fiscal austerity has stalled the public sector jobs boom.

And the private sector is not ready to pick up the slack. The two most interest-sensitive sectors—housing and consumption—have large headwinds.

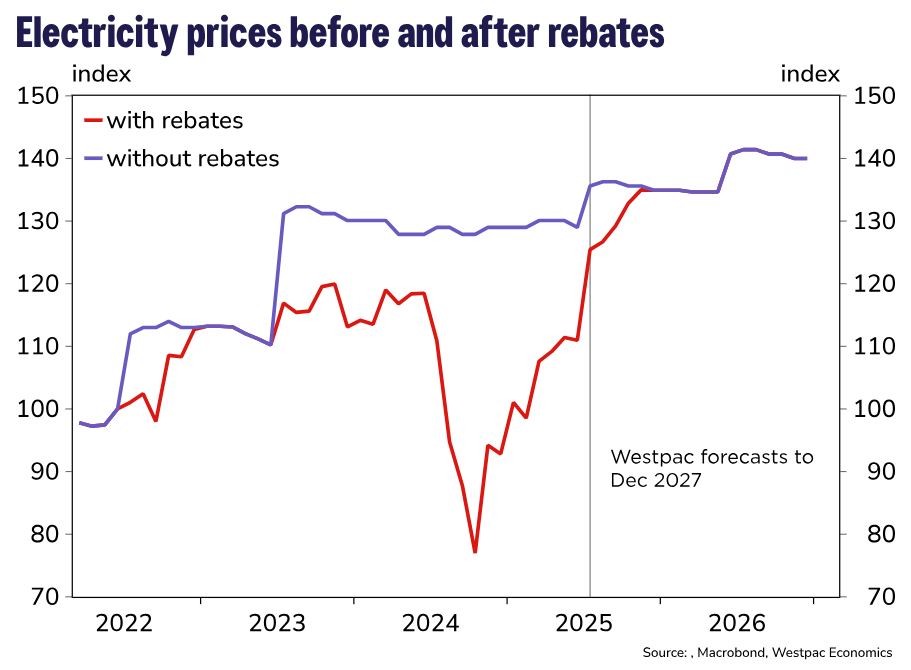

The consumer is being shocked by energy bills.

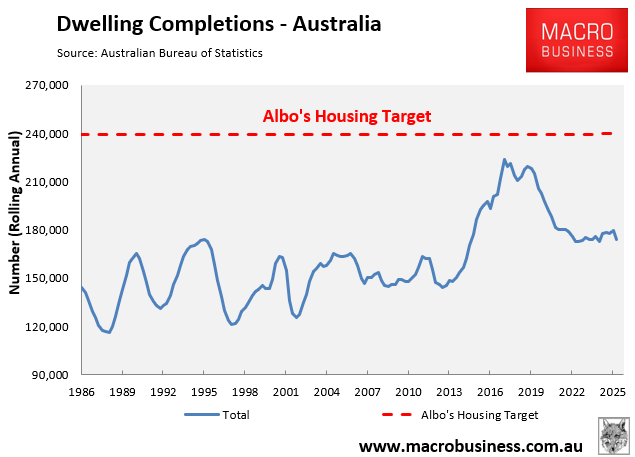

And dwelling construction is stalled at best, also, in part, owing to Albo’s endless energy shock, expressed through building material costs.

There is nothing to pick up the public jobs slack. Ergo, the RBA will be making insurance cuts all the way to 5% unemployment as it wipes out “labour market gains”, again.