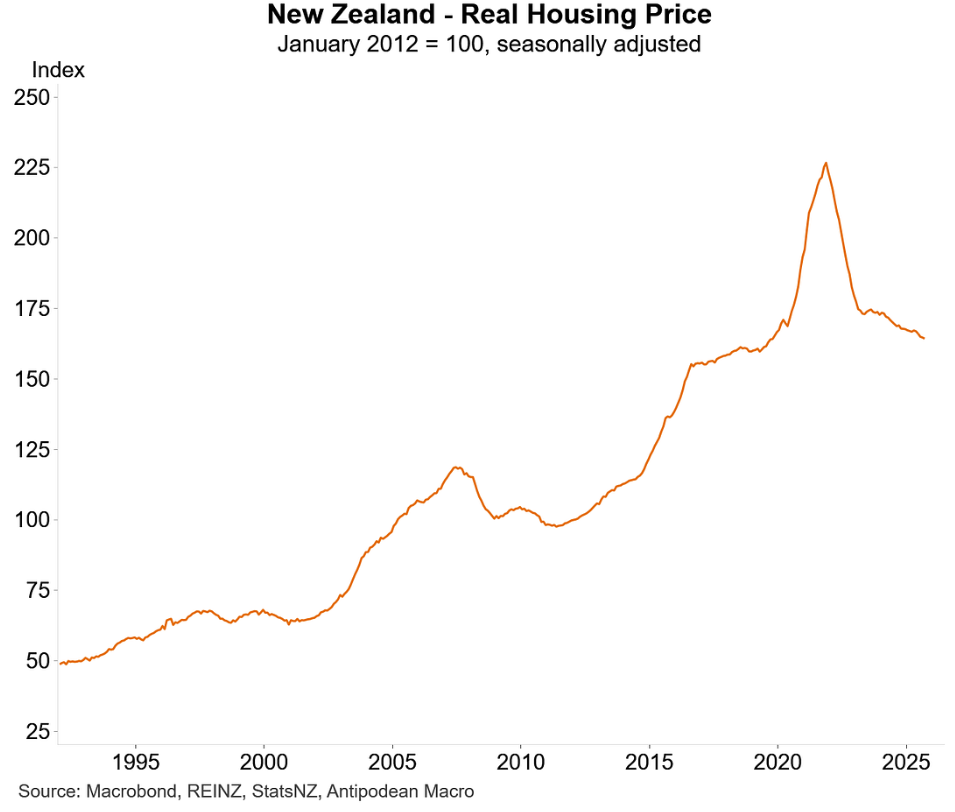

The following chart from Justin Fabo from Antipodean Macro illustrates that, in real inflation-adjusted terms, New Zealand dwelling values have crashed back to 2019 pre-pandemic levels:

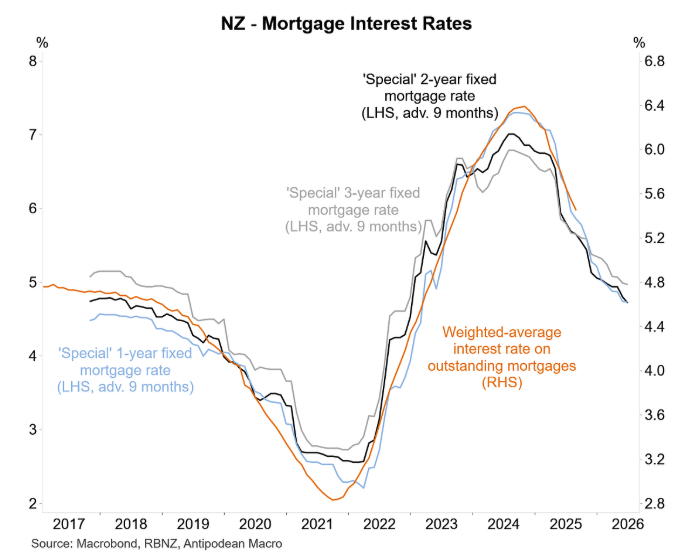

At the same time, the Reserve Bank of New Zealand has slashed the official cash rate by 3.0% to 2.5%, which has driven mortgage rates sharply lower.

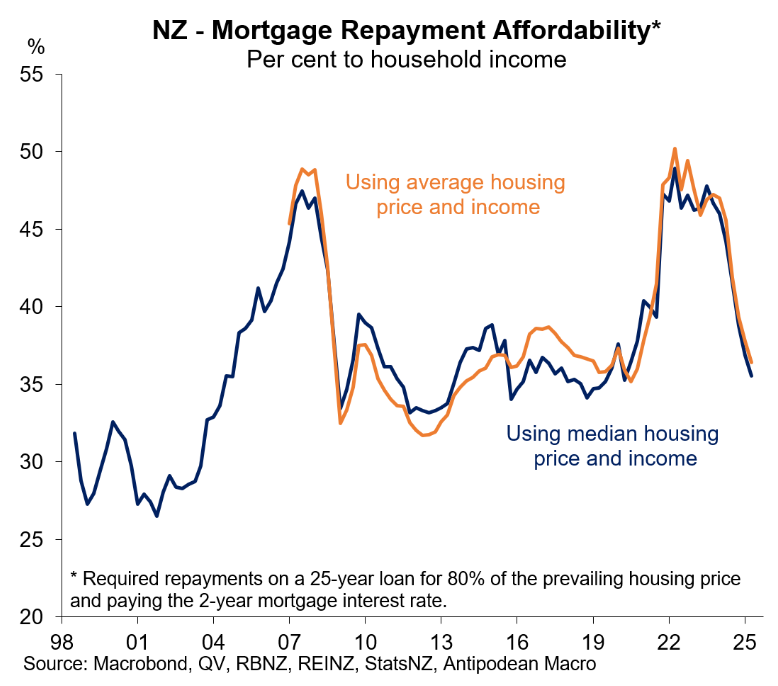

As a result, median New Zealand mortgage repayment affordability has fallen back to where it was in 2004:

New Zealand first home buyers are also finding the going much easier today than a few years ago, thanks to relatively flat prices at the bottom of the market, falling mortgage rates, and slowly rising incomes.

According to Interest.co.nz, the median lower quartile price at which 25% of sales are below has declined to $590,000 as of September, down $80,000 from the record high of $670,000 in November 2021.

The average two-year fixed mortgage rate offered by the main banks has also fallen from 4.72% in September, down from its recent high of 7.04% in November 2023.

Interest.co.nz also estimates that the after tax income of a typical first-home-buying couple has increased by $82 a week (3.9%) compared to September last year.

The upshot is that “if a home was purchased at the September 2025 lower quartile price of $590,000 with a 10% deposit, the mortgage payments would probably be around $728 a week”, which “is the most affordable it has been since June 2021”.

However, this only tells part of the story, given that first-home buyers typically need to rent while they save for a housing deposit.

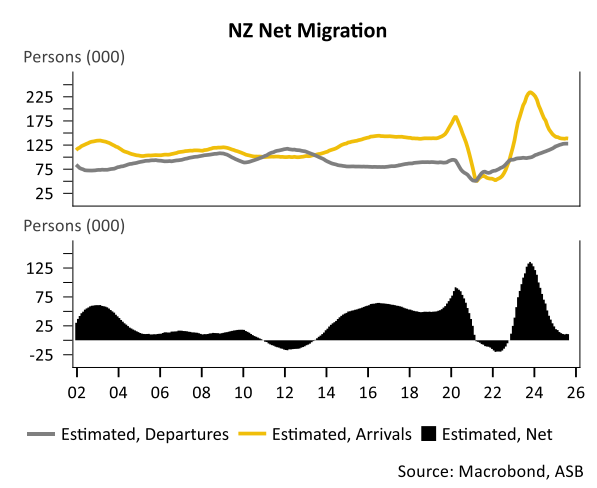

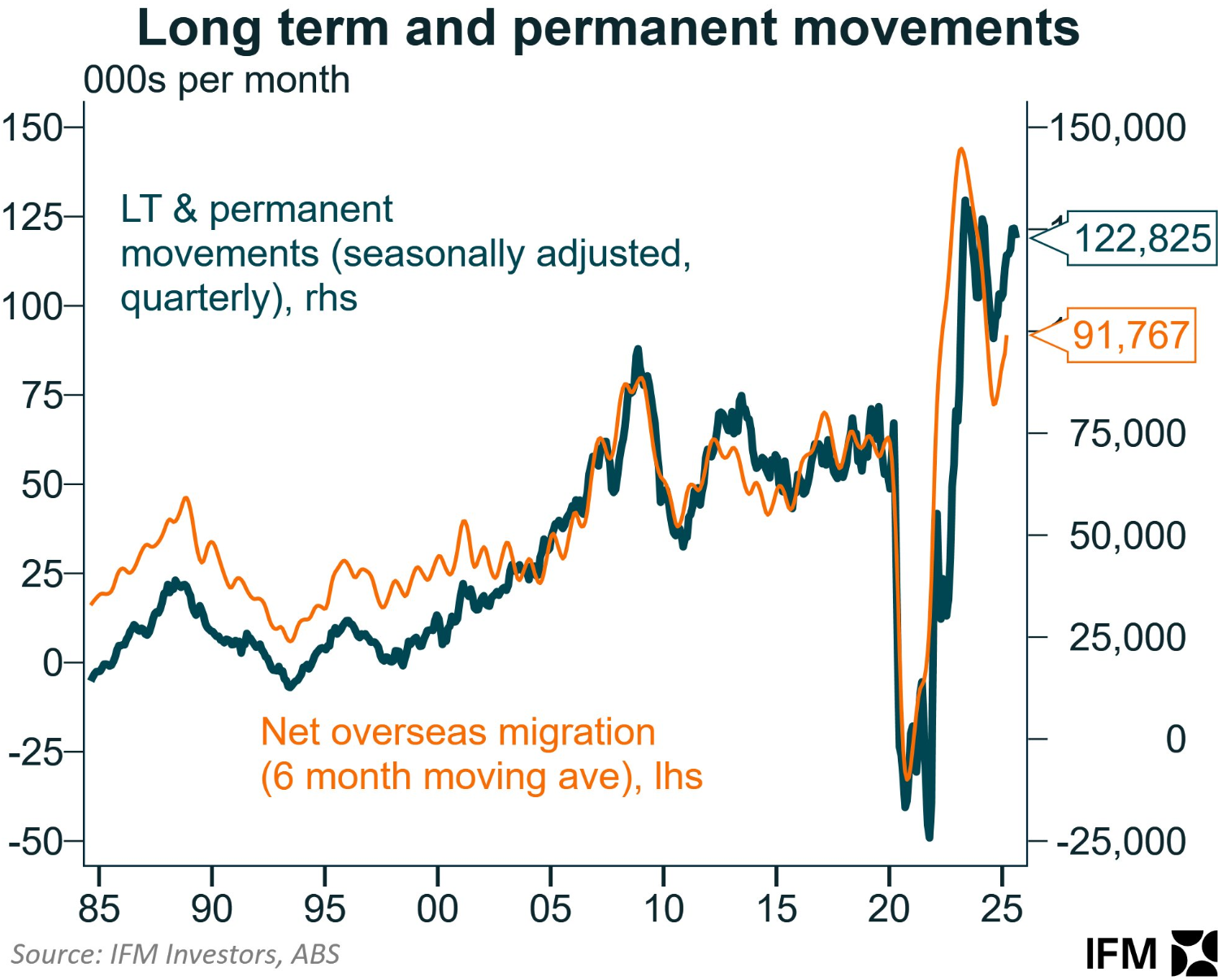

The latest migration data from Stats NZ revealed that only 10,628 net overseas migrants landed in the country in the year to August 2025, which was well below the decade average of 49,000 and around 120,000 fewer than the late 2023 peak:

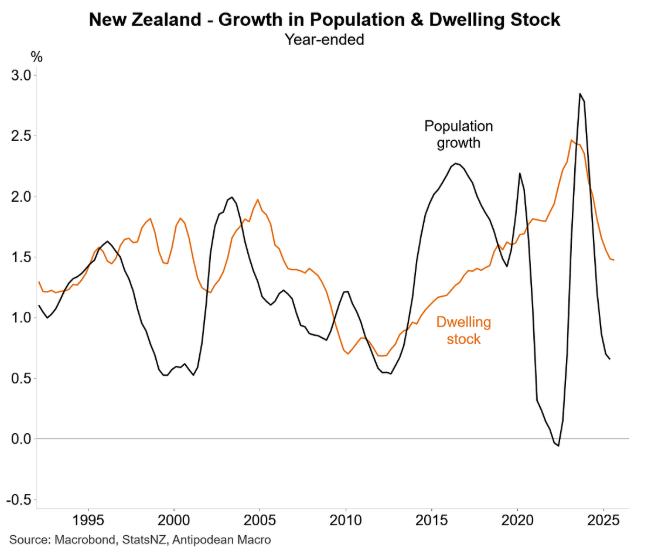

The growth in New Zealand’s dwelling stock is now significantly outpacing population growth:

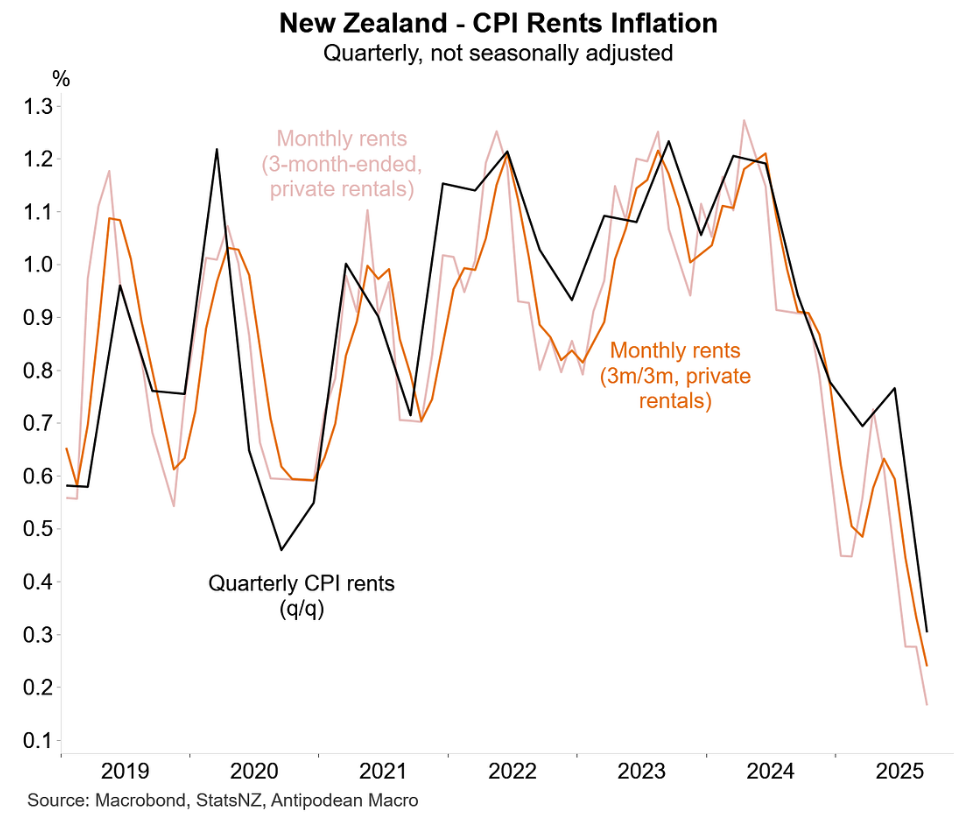

As a result, New Zealand rental growth has crashed to an unprecedented low:

Indeed, the latest Trade Me rent price index reported that asking rents fell by 1.6% in the year to September, whereas Realestate.co.nz reported a steeper 3.1% decline in annual asking rents.

Regardless, prospective first-home buyers in New Zealand are benefiting from lower home prices, rents, and mortgage rates.

Sadly, Australian first-home buyers aren’t so lucky. Net permanent and long-term (NPLT) arrivals into Australia have spiked, adding to housing demand.

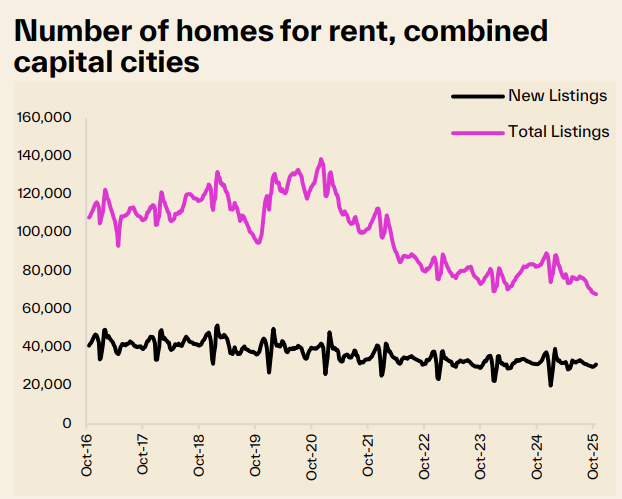

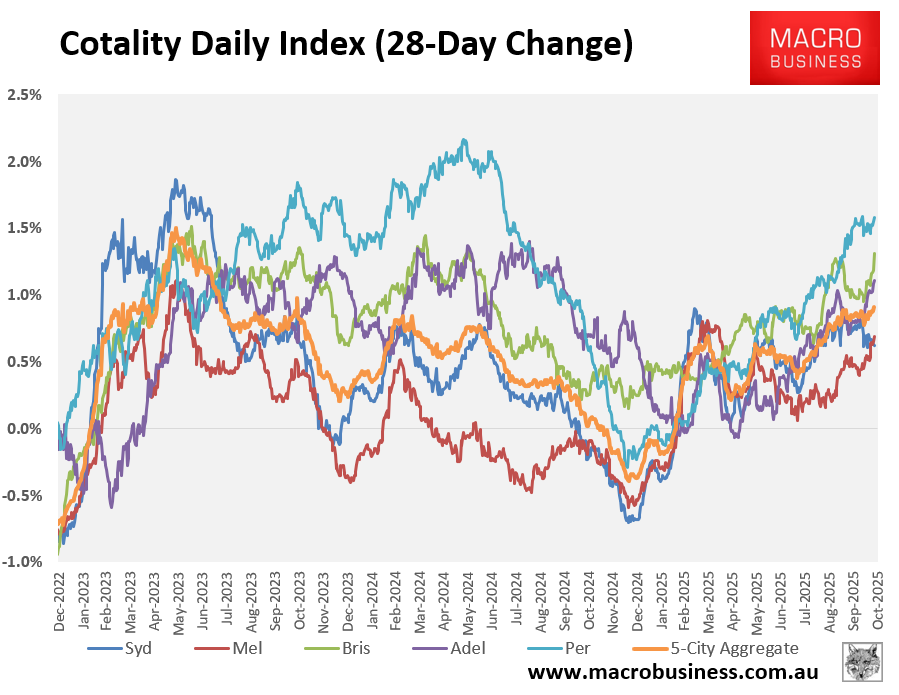

Rental listings across the combined capital cities in Australia have fallen to a record low:

Source: Cotality

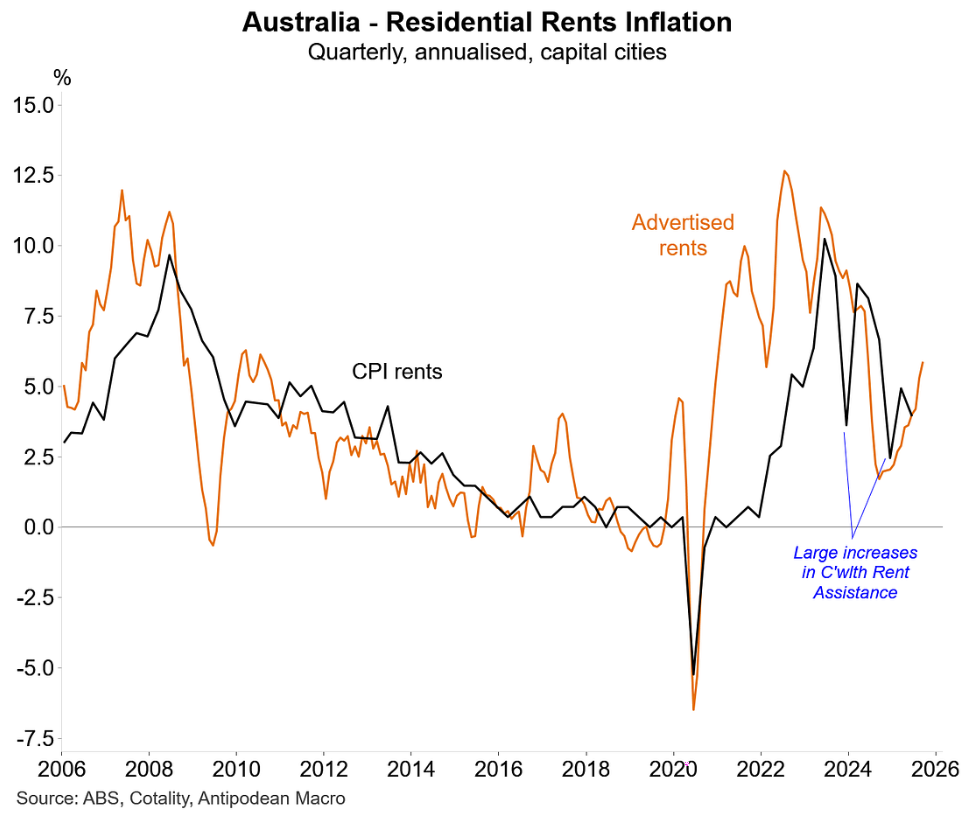

As a result, advertised rents, which have already risen by 43.8% over the past five years, are reaccelerating:

Australian dwelling values have also recorded their fastest growth in two years across the five major capital city markets:

Thus, while housing is becoming increasingly affordable in New Zealand, it is the opposite case across the pond.