The 2025 federal election campaign saw both sides admit that they wanted to see Australian home prices rise at a ‘sustainable rate’ from already record-high levels.

Both Labor and the Coalition offered ‘affordability’ policies that were really aimed at pumping homebuyer demand and increasing prices.

It was a theme that has been repeated throughout this century in Australia, via demand-side policies, including first-home buyer grants, shared equity schemes, etc., that have increased mortgage sizes and pushed home prices forever higher.

Labor emerged victorious in the election and last week unveiled its 5% deposit scheme for first-home buyers, a policy that will intensify Australia’s housing crisis by stimulating demand.

Indeed, mortgage brokers and real estate agents have already reported strong interest from first-home buyers.

Labor’s 5% deposit scheme will leave future first-home buyers vulnerable to negative equity in the event of a future major downturn, whereas taxpayers will be liable for any potential mortgage defaults by users of the scheme.

Because the government will guarantee 15% of first-home buyer mortgages, it also incentivises the government to continue supporting house prices in the future.

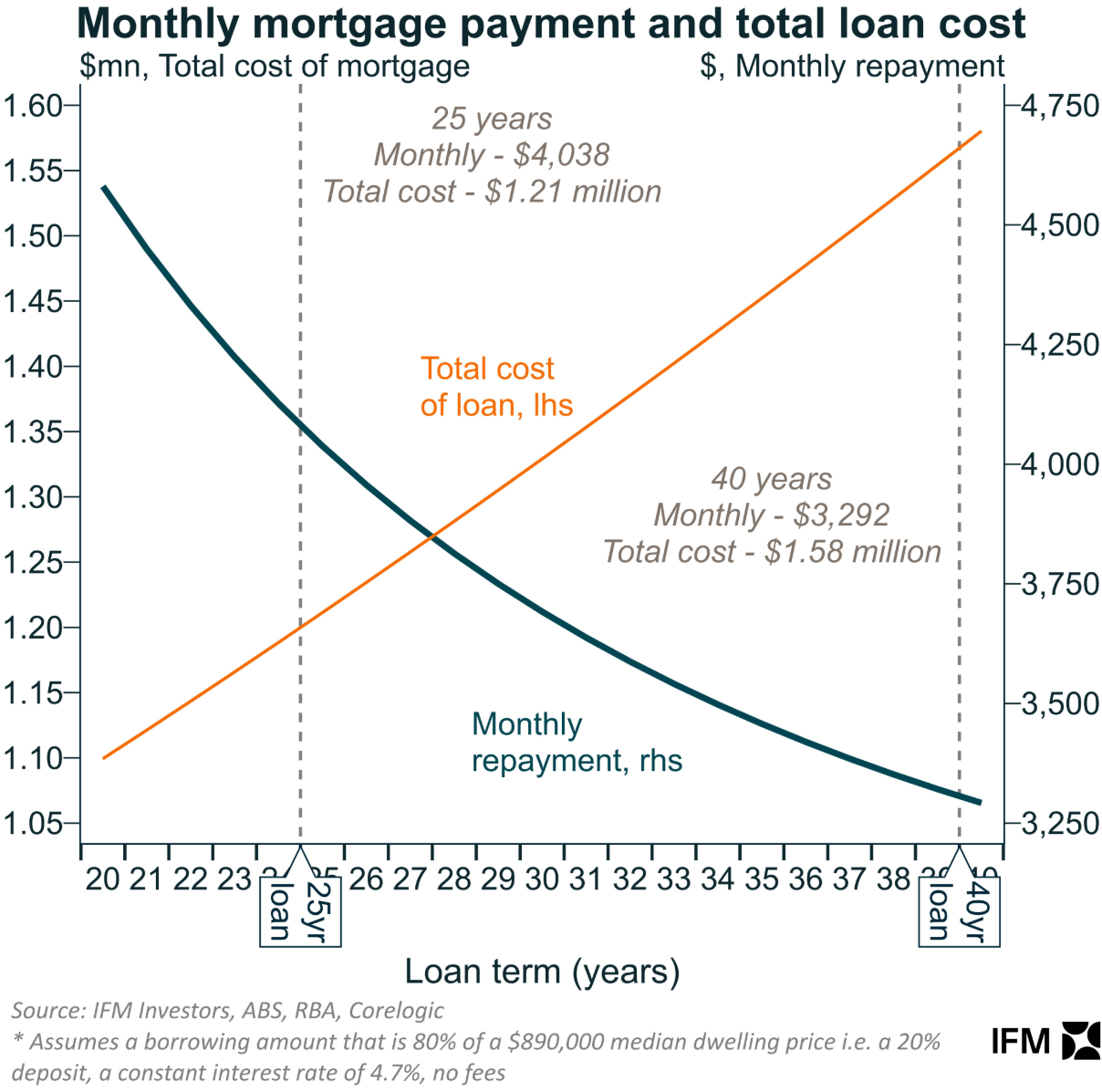

Adding further to the housing bonfire, several lenders in Australia have begun offering 40-year mortgages, two of which are solely for first-time purchasers.

This week, The AFR’s Wealth reporter Jessica Penny questioned whether the 40-year mortgage, by offering lower monthly repayments, is “a path to wealth or a lifelong debt trap?”.

“The idea is that by extending their loan term, borrowers will bear an easier burden when it comes to monthly repayments”, Penny wrote. “But a 40-year mortgage introduces a new kind of trade off – because it also means locking yourself into an extra 10 to 15 years of housing debt”.

“While a 40-year mortgage offers the immediate benefit of lower monthly repayments, it’s important to recognise that over the long term, borrowers will pay significantly more interest, and it will also take longer to build up equity in the property”, Kylie Moss from comparison site Mozo added.

Penny then cited research from Great Southern Bank showing that around 29% of Gen Z and Millennials and 19% of Gen Xers would consider taking out a home loan for up to 40 years if it meant lower repayments.

“For some Australians having lower monthly repayments is the difference between renting and buying their first home”, Rolf Stromsoe, Great Southern Bank’s chief customer officer, argued.

According to Canstar, an individual on a median full-time wage is eligible to borrow up to $24,000 more on a 40-year mortgage than they would on a 30-year term, while a couple working full-time can borrow up to $48,000 more.

The following chart from Alex Joiner at IFM Investors shows how a lengthier 40-year mortgage term increases borrowing capacity.

Longer loan terms decrease monthly repayments, but total payback costs grow, and more Australians will carry mortgage debt into retirement.

The reality is that these types of mortgage products inevitably increase borrowing capacity, household debt, and ultimately home prices.

When combined with demand-side policies such as Labor’s 5% deposit scheme, these mortgage products exacerbate the housing crisis and ultimately undermine financial stability and affordability.

First-home buyers in Australia are excluded from the market because prices are too high relative to incomes. They are also paying a record share of their incomes on rent while they save for a deposit.

The obvious solution is to restrict immigration, which is a double whammy for first-home buyers because:

- Excessive immigration increases the costs of renting, making it more challenging for prospective first-home buyers to save a deposit.

- Excessive immigration puts upward pressure on home prices, pushing ownership further out of reach.

The federal government should also ‘make room’ for first-home buyers by dampening investor demand via winding back negative gearing and capital gains tax concessions.

I discussed these themes in this week’s Treasury of Common Sense on Radio 2GB/4BC.