DXY is not going away.

AUD is at the top of its recent range.

CNY has given up the ghost.

Gold is still vumnerable in my book.

AI metals to the moon.

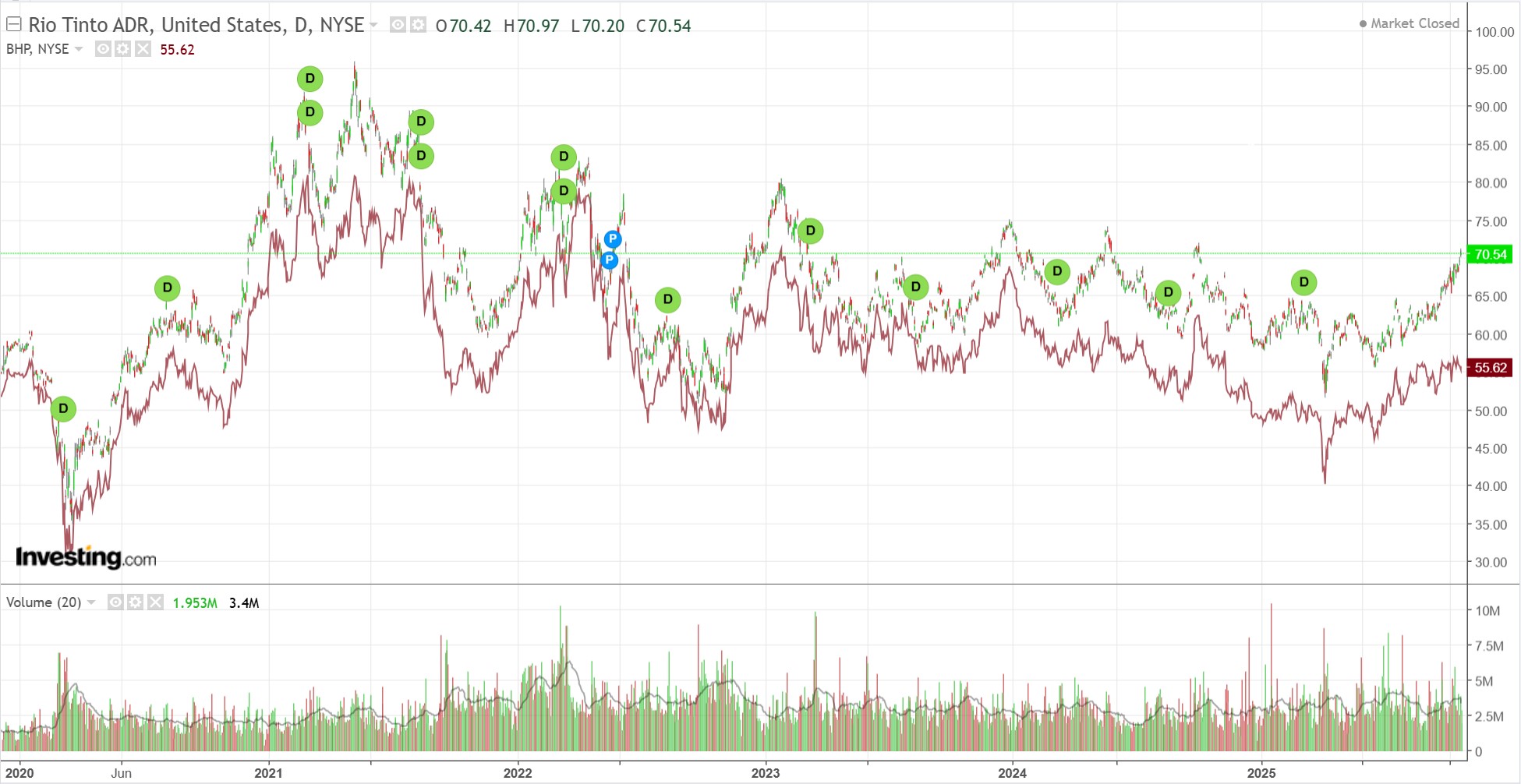

Rio is the chosen one.

EM breaking higher.

Junk is back at the core but not the periphery.

Yields stalled on oil.

Stocks ATH.

US inflation was weak but questionable with the government shutdown. DXY will resume falling, says Goldman Sachs.

USD: Absence makes the Dollar grow stronger.

We think the labor market headwinds from the US government shutdown should contribute to Dollar downside, but so far it seems that the US data “time out” has helped markets focus on challenges abroad.

We wrote earlier that realized FX vol tends to fall during government shutdowns, which we attributed to limited data releases, and there has been some element of that this time around as well (Exhibit 1).

However, implied vols have stayed somewhat elevated in response to political developments in Japan, France and the UK (Exhibit 2).

This is also reflected in spot markets and investor sentiment, with much of the Dollar’s recent resilience coming in response to news about Japan’s fiscal plans or European data that have revived expectations for some rate cuts in the near term.

We think some of this is misplaced.

It is likely that the government shutdown is at least temporarily restraining activity, while also causing the limited visibility, and our economists believe it is better to follow the softer signals from the labor market, including what they are able to extract from the available surveys.

We also note that the return of trade tensions has revived the Dollar’s negative response to global tariff worries, which we think is justified.

We expect this to also be on the minds of longer-term asset managers as they consider their global allocation mix for next year, which should be a continued source of Dollar depreciation pressure.

We also think the Dollar’s recent pro-cyclical correlations should be in focus again next week.

Meh, I’m not so sure. Why would the end of government shutdowns sink DXY? This is an easing of risk, not intensification.

Trade likewise. If there is a US-China deal or some framework to produce it, the pressure on the DXY comes off.

And then there’s rising oil. Although I do not think a big spike is in the cards, the short-term squeeze adds a thermal under DXY as a boost to shale and a headwind for the Fed (though it would need to push through $75 to become inflationary year on year).

My own view is that DXY has more work to do before it can resume falling.

That leaves AUD in the recent range.