DXY fell away.

This time AUD enjoyed relief.

CNY resumed the plod higher.

Oil is in trouble. Gold finally popped.

Metals too.

And miners.

EM at the highs.

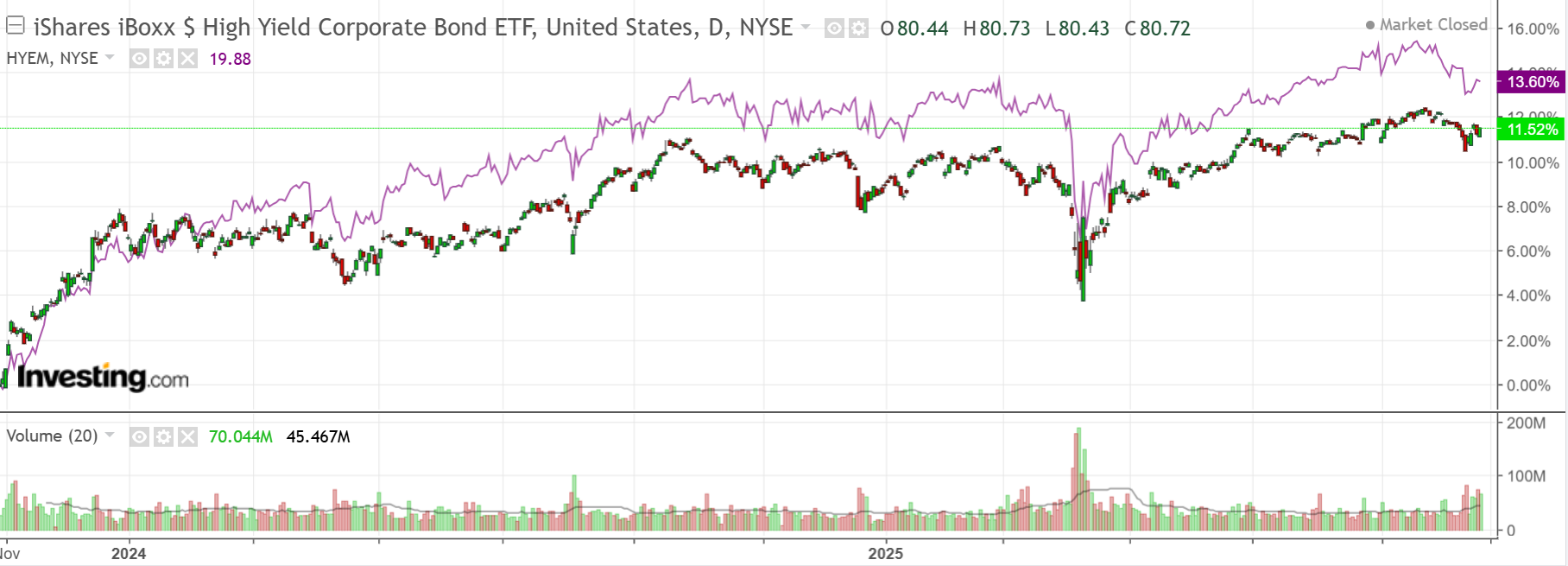

Junk still worried.

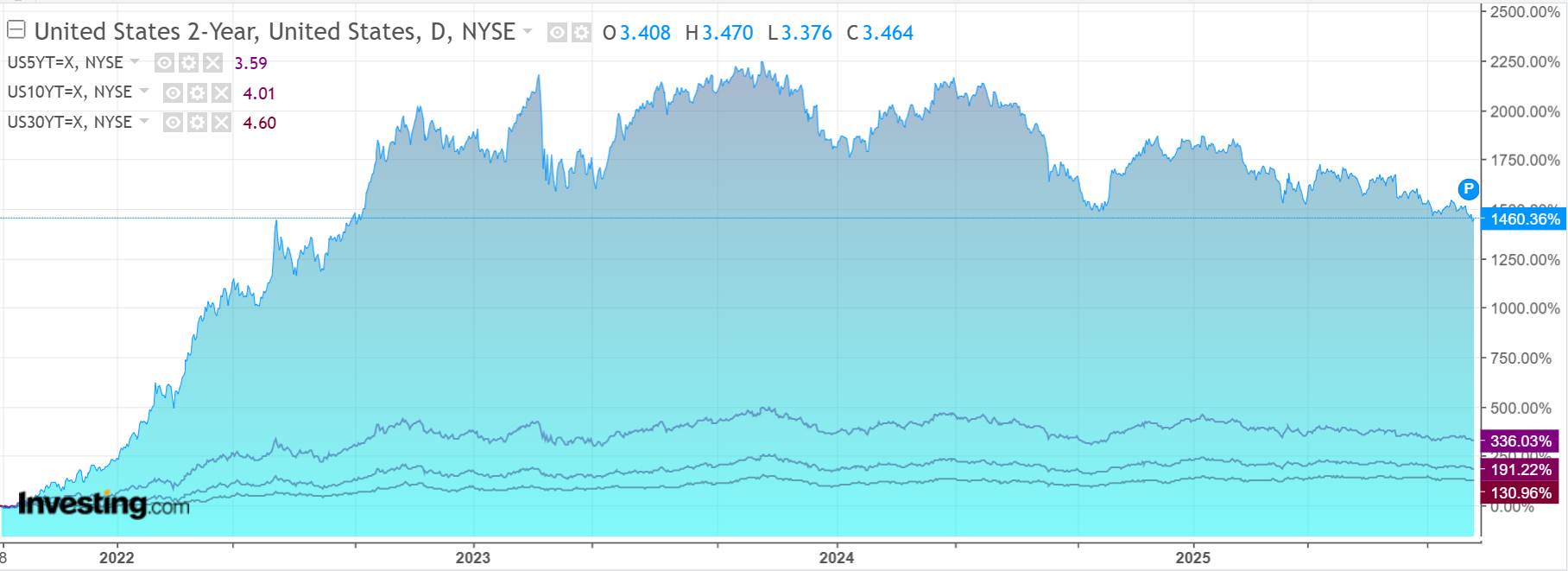

The bond rally paused.

Stocks lifted a bit.

Trump eased the rhetoric on China. As usual, the loon is predictable only in the unpredictability that he needs to be the daily headline. Not much data with the government shutdown.

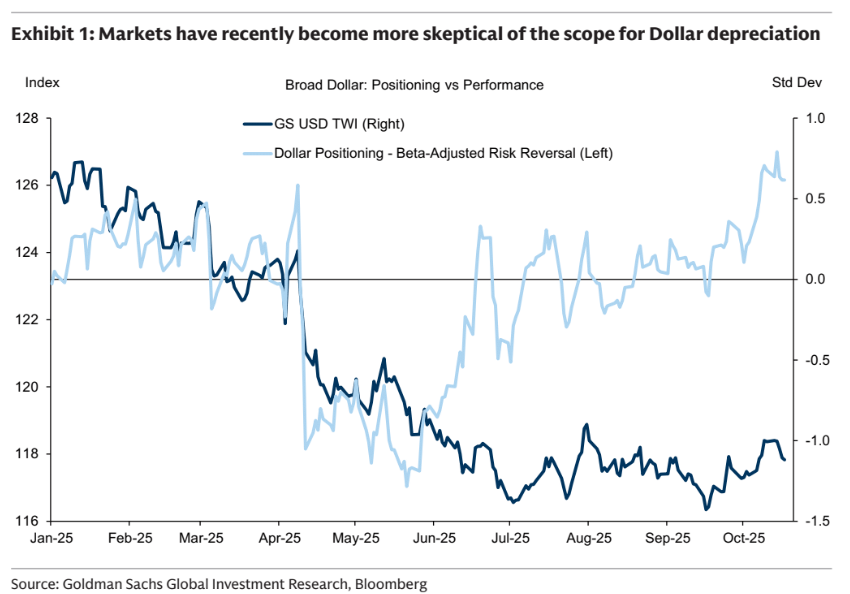

Goldman reckons DXY is going lower.

USD: Three risks return.

For much of the year, we have argued that the Dollar should decline because US outperformance will narrow, and that means the Dollar should lose some of its high valuation.

First, the return of tariff threats is negative for the Dollar.

Our research points to several channels at work where the size and scope of these tariff threats weighs on the Dollar via weaker terms of trade and confidence effects.

Second, the cumulative effects of an extended shutdown can weigh on the Dollar by adding another headwind to the labor market and raising the likelihood of more disruptive fiscal cuts.

Third, new concerns of a “credit crunch” can be negative even for the safe-haven Dollar.

Our research shows that tighter credit conditions are negative for the currency because they weigh on investment intentions, diminish the appeal of US assets, and can necessitate easier monetary policy settings.

A few points:

- Tariffs are bullish for a currency. However, inept tariffs are bearish.

- Yes, there are US growth headwinds. This will probably narrow its relative performance.

- So long as any credit crunch remains contained, it is bearish for the currency.

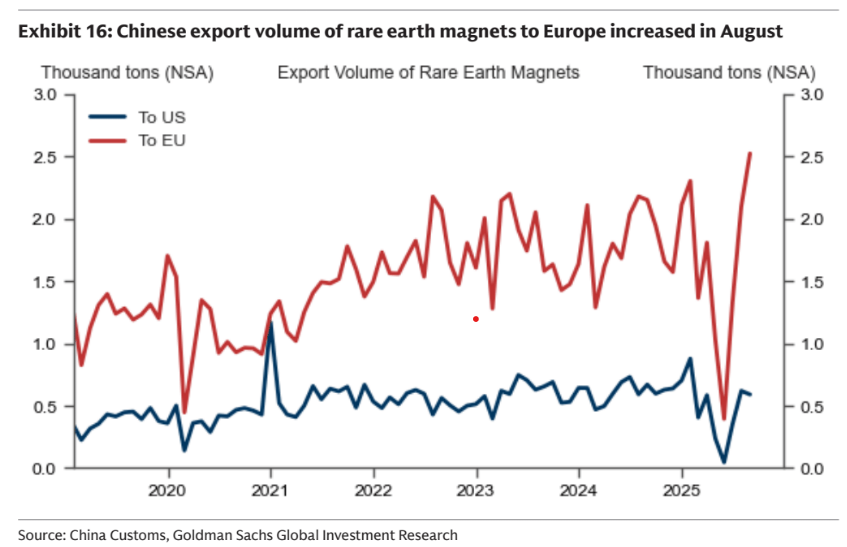

The great variable is Trump. With the G7 revving up, he is more likely to get China to back down on rare earths. It can’t afford to alienate Europe, which is fast turning into a rare earths way station.

But Trump is not going to get concessions beyond unwinding recent hawkishness.

At home, after three weeks, the government has to reopen soon.

As he climbs down at home and abroad, Trump will need a new scandal to attract attention.

Invasion of Venezuela, anyone? That’s unlikey to go well and would weigh on DXY via the fiscal channel.

When the current Trump funk clears, the new one may be worse. Or not.

Goldman sees AUD at 0.69 in 2028, which is not worth the paper it is printed on.

Whichever way the loon leans, it will set the course.