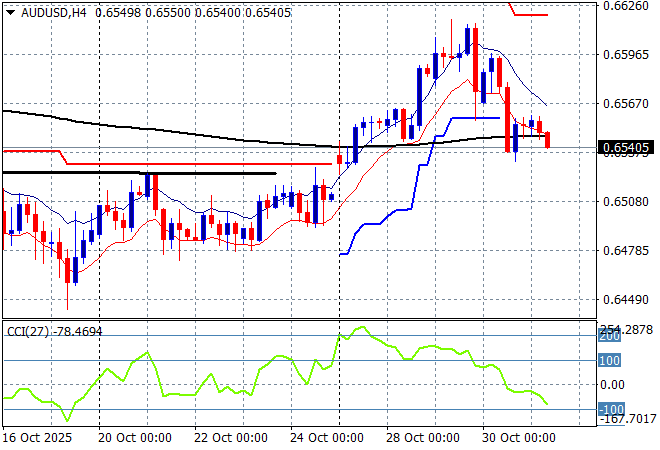

Asian markets are generally lower although the latest Tokyo inflation numbers saw Japanese stocks rise swiftly with another BOJ rate hike now on the cards while the outcome of the Trump-Xi summit is not inspiring confidence in other risk markets. In currency land, the USD is getting stronger again with the Australian dollar pulled back to the 65 cent level.

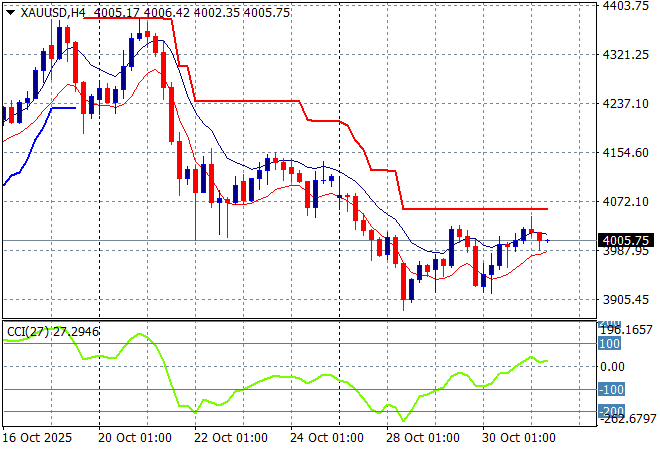

Oil markets are barely holding on to their recent breakout with Brent crude stuck at the $63USD per barrel level while gold is also struggling at the $4000USD per ounce level but might be building some support here for a potential breakout:

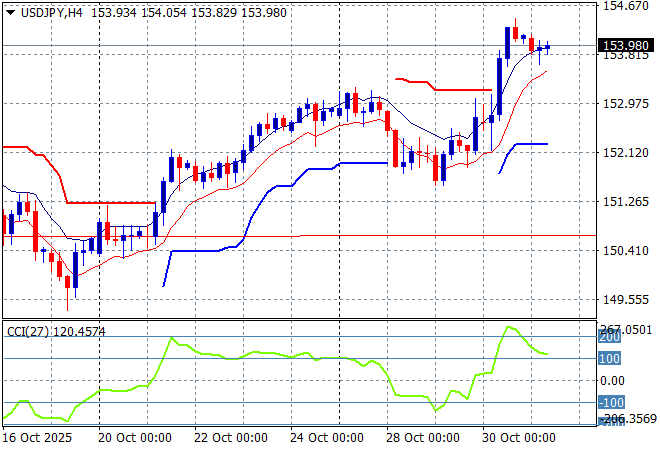

Mainland Chinese share markets are falling again going into the close with the Shanghai Composite down more than 0.6% to retreat well below the 4000 point barrier while the Hang Seng Index has reopened after its holiday to slide more than 1% lower. Japanese stock markets are the odd ones out with the Nikkei 225 up nearly 2% at 52300 points while the USDPY pair has seen a stable session after almost breaking out above the 154 level:

Australian stocks are unable to find any positive momentum with the ASX200 closing dead flat at 8881 points while the Australian dollar has slid slightly after a volatile session overnight to just below the mid 65 cent level against USD as Fed rate cut expectations vanish:

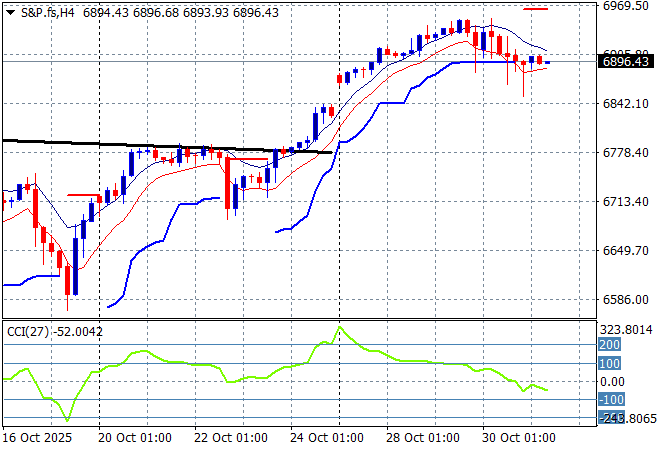

S&P and Eurostoxx futures are steadying but seeing increased volatility as we head into the London session with the S&P500 four hourly chart showing the market holding on at the 6900 point level but could be ready to breakdown here:

The economic calendar finishes the trading week with a few European inflation datasets then the closely watched (and probably to be “managed”) core PCE numbers from the US.

Happy Halloween or Samhain for the Celts out there for actually invented it – or “Big Fucking Storms Every Afternoon” Season if you live in SEQ….