Risk markets are again pivoting on more tantrums from the Oval Office as the Trump regime lashes out at Canada and Venezuela via the usual online 12-year old boy tantrums from the Mango Mussolini. Asian share markets brushed off the histrionics and are seeing strong bids to finish the trading week but all eyes will be on tonight’s CPI print from the US as the USD firms against Yen and the Australian dollar in today’s session.

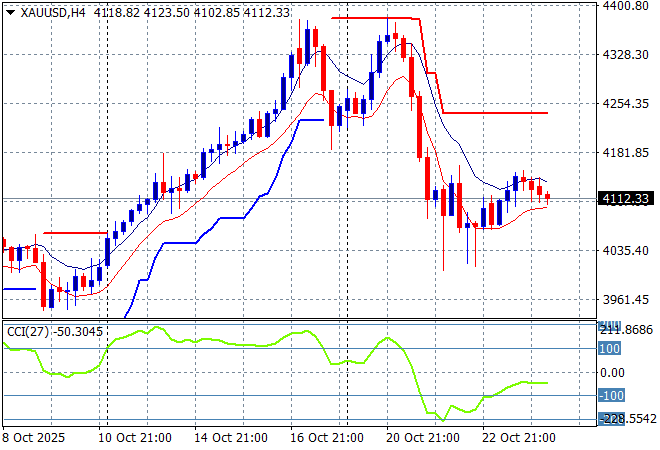

Oil markets are holding on to their recent breakout with Brent crude staying above the $65USD per barrel level while gold has tried to stabilise after its correction, holding just above the $4100USD per ounce level:

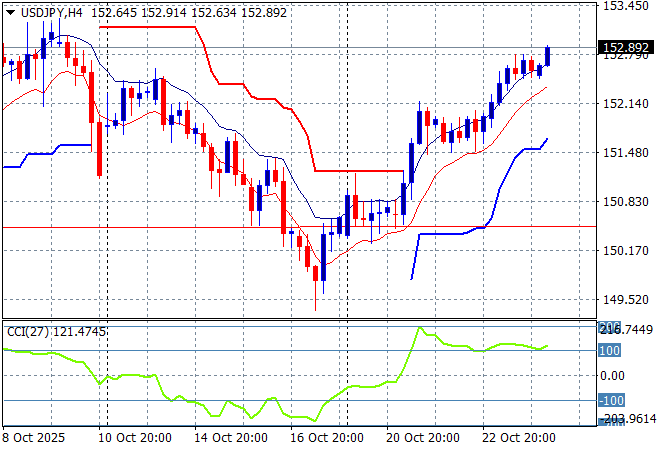

Mainland Chinese share markets are lifting going into the close with the Shanghai Composite up more than 0.3% at 3983 points while the Hang Seng Index is up 0.6% to 26122 points. Japanese stock markets are rebounding with the Nikkei 225 up more than 1.5% to 49402 points with the USDPY pair almost pushing above the 153 level:

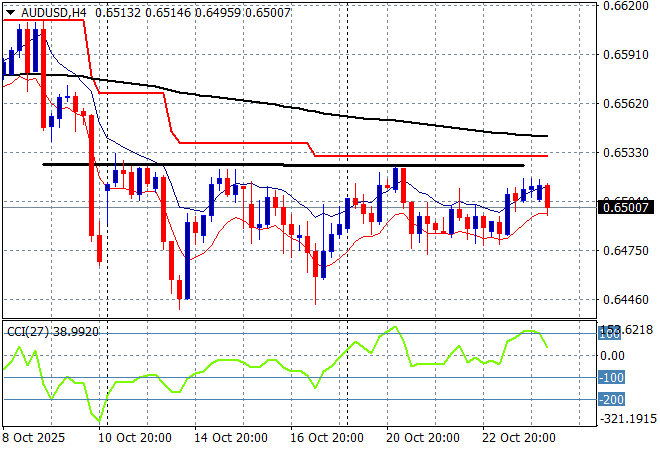

Australian stocks were the standout with the ASX200 actually alone in closing in negative territory finishing 0.1% lower at 9026 points while the Australian dollar has again failed to breach resistance above the 65 cent level against USD:

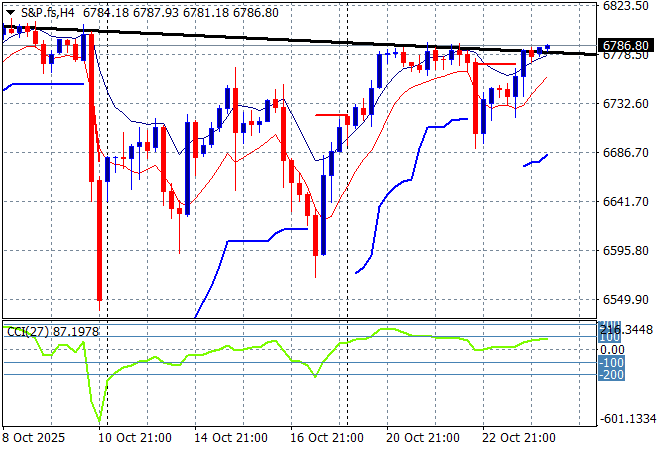

S&P and Eurostoxx futures are heading slightly higher as we head into the London session with the S&P500 four hourly chart showing the market getting back on track after the slump from the previous Friday session, as the TACO trade builds again:

The economic calendar will focus squarely on the latest US CPI print tonight.