Energy superidiot fiddles while global gas burns

The IEA has done an analysis of the immense looming global gas glut. It is even bigger than I thought.

Following the supply shock of 2022/23, natural gas markets moved towards a gradual rebalancing in 2024 and 2025. During this period, supply fundamentals remained tight and prices stayed well above their historic levels. This limited demand growth, especially in price-sensitive Asian markets.

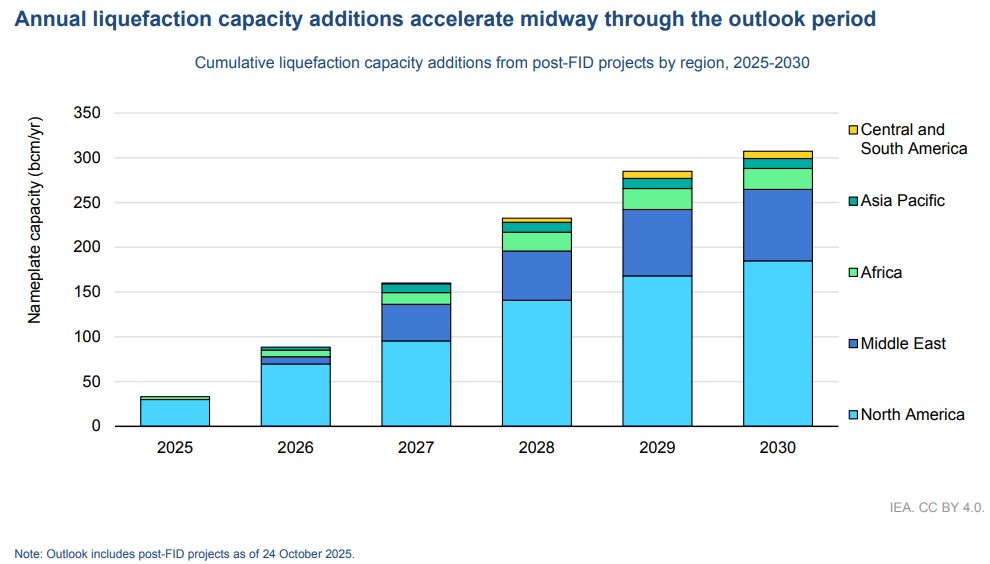

Around 300 billion cubic metres per year of new liquefied natural gas (LNG) export capacity is expected to be added worldwide by 2030, primarily supported by liquefaction capacity expansions in the United States and Qatar. This wave of new LNG production capacity is set to profoundly transform global gas market dynamics. The scaling up of LNG supply will play a key role in enhancing supply security and improving the affordability of natural gas – including in price-sensitive emerging import markets.

The analytical framework underpinning the medium-term outlook in this report is structured around a base case, which is complemented by a high case that explores the potential for greater demand response to possible price changes. The base case reflects current project plans, policy settings and economic growth projections, as well as prices informed by the current forward curve.

The high case assumes that LNG import prices move closer towards the short-run marginal cost of US LNG supply and unlock additional gas demand, especially in price-sensitive Asian markets. However, Asia Pacific, Central and South America, Eurasia, Europe and North America weaker macroeconomic environment, together with a slower buildout of natural gas infrastructure and contractual rigidities, might limit the scope of the price-adjusted demand response.

A prolonged period of lower LNG prices could reduce the incentive for project developers to invest in LNG liquefaction projects and in upstream and midstream infrastructure. This, in turn, could lead to a potential tightening of global gas markets post-2030, especially if demand growth follows a higher trajectory.

Yes, the gas glut will end. But only by crashing prices to release new demand.

Whatever path of gas reservation Albo’s idiots choose, this is the window of opportunity to find a way out for Australia’s gas market wreckage.

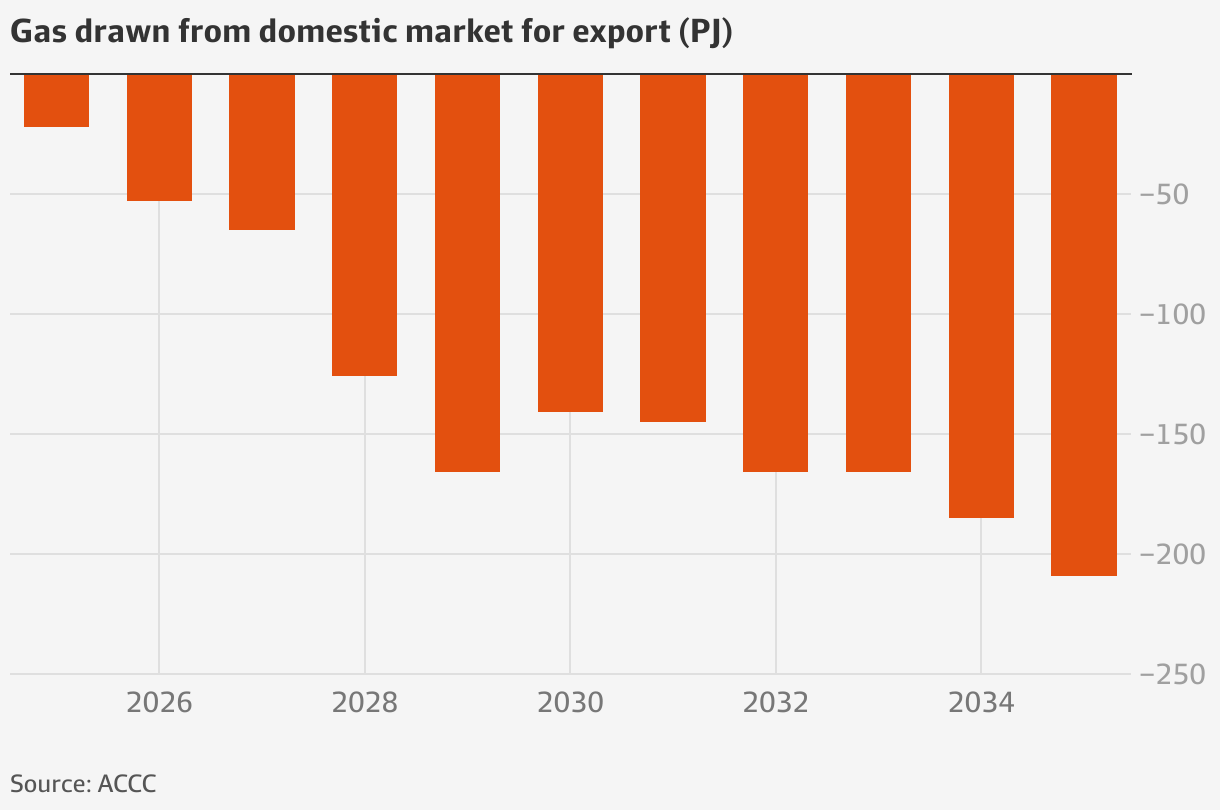

The East Coast gas cartel—notably GLNG—must recontract for future gas supplies to its customers later this decade from international markets so that the gas it currently draws locally is returned to Australian users.

Re-contracted prices will be cheap given the looming glut; they will need a force majeur trigger to re-contract, and local prices will crash as GLNG volumes stay in Australia.

The impact on everybody east of WA will be enormous as energy deflation replaces relentless energy inflation. Richard Holden.

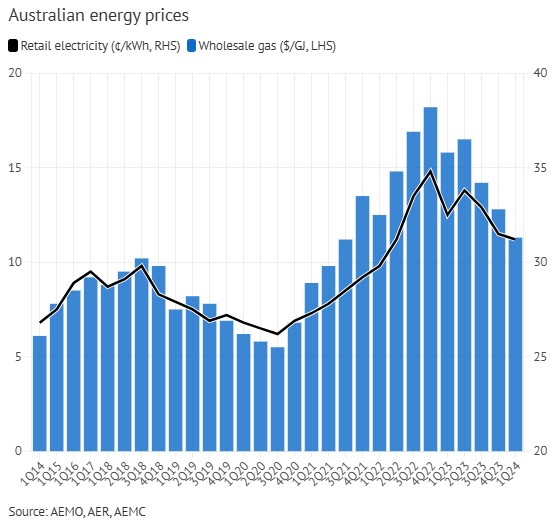

To see why, just look at the relationship between wholesale gas and retail electricity prices between 2014 and last year. Higher gas prices mean higher electricity prices. Period. In fact, the correlation is almost perfect – 0.945.

Why? Because gas is what economists call the “marginal supplier” of energy. It’s the thing you can switch on, what you can turn to when other energy sources are not available.

But even when other energy sources are available, gas effectively sets the electricity price. This is a hard-wired design feature of electricity pricing. Prices are set based not on the cost of the energy source being used, but on what alternative energy source could be used. In other words, it’s all about opportunity cost.

Nothing I haven’t said a million times, but at least it’s gotten through in some corners.

There’s more.

Speaking exclusively to The Daily Telegraph, AWU National Secretary Paul Farrow warned Australia risks losing its industrial base without action from the Albanese Government.

“Right now, Japan buys our gas under favourable long-term contracts that our domestic manufacturers can’t access – and it sells it on to other countries for over a billion dollars in profit.”

“You have to wonder what the government is waiting for. The choice has become stark. Introduce a comprehensive gas reservation scheme right now or watch Australia’s capability to make things completely evaporate on your watch.”

“You don’t have to interfere with existing export contracts, so anyone crying ‘sovereign risk’ is crying wolf. All you have to do is make sure additional gas resources go to Australians first.

The polling – conducted by Demos and commissioned by Asia Pacific LNG (APLNG) – found 73 per cent of those who support a national gas reservation want it to begin immediately.

Eighty-two per cent back the AWU’s call to require gas giants to contribute to the domestic market in order to qualify for an export permit.

You don’t have 82% agreement on the world being round. The failure to act on this for so long indicates a failing state.