In last week’s monetary policy decision, the Reserve Bank of Australia (RBA) decided to keep the official cash rate on hold, citing resurgent inflation risks.

The RBA’s statement noted that “the decline in underlying inflation has slowed”, with “recent data, while partial and volatile, suggest[ing] that inflation in the September quarter may be higher than expected at the time of the August Statement on Monetary Policy”.

Following the decision, economists and financial markets have tempered their expectations of rate cuts, with the latest interest rate futures pricing suggesting that only one further 25 bp reduction will be delivered:

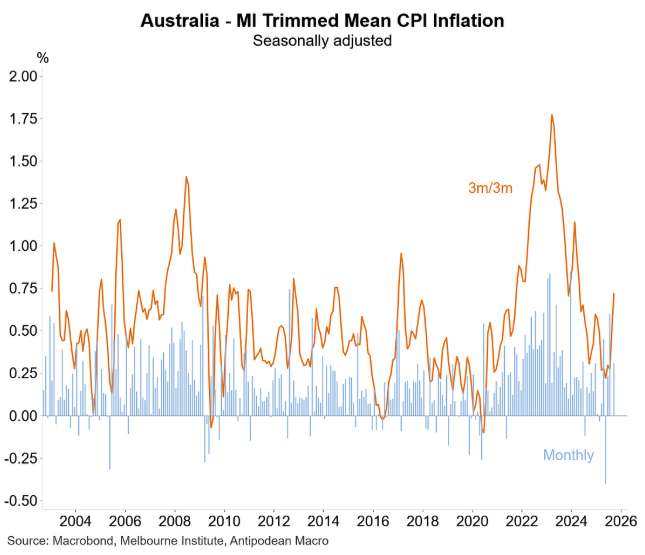

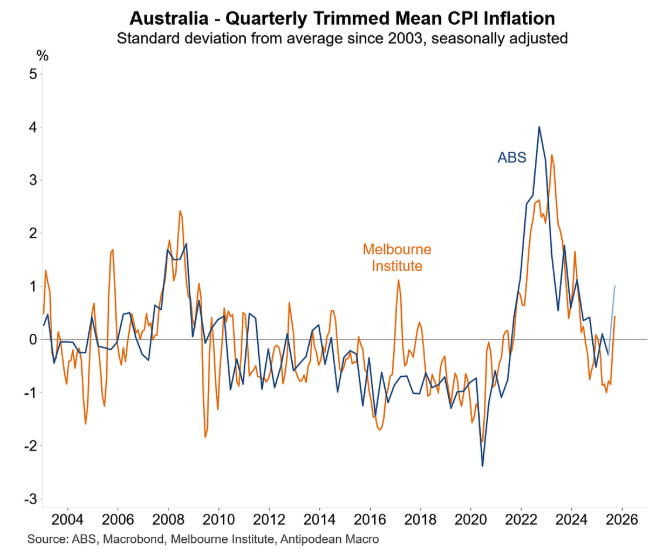

The Melbourne Institute’s inflation gauge for September, presented below by Justin Fabo from Antipodean Macro, reported that trimmed mean inflation has reaccelerated over the past few months.

“The signal from the Melbourne Institute series is consistent with our expectation for sharply higher Q3 trimmed mean inflation”, Fabo wrote.

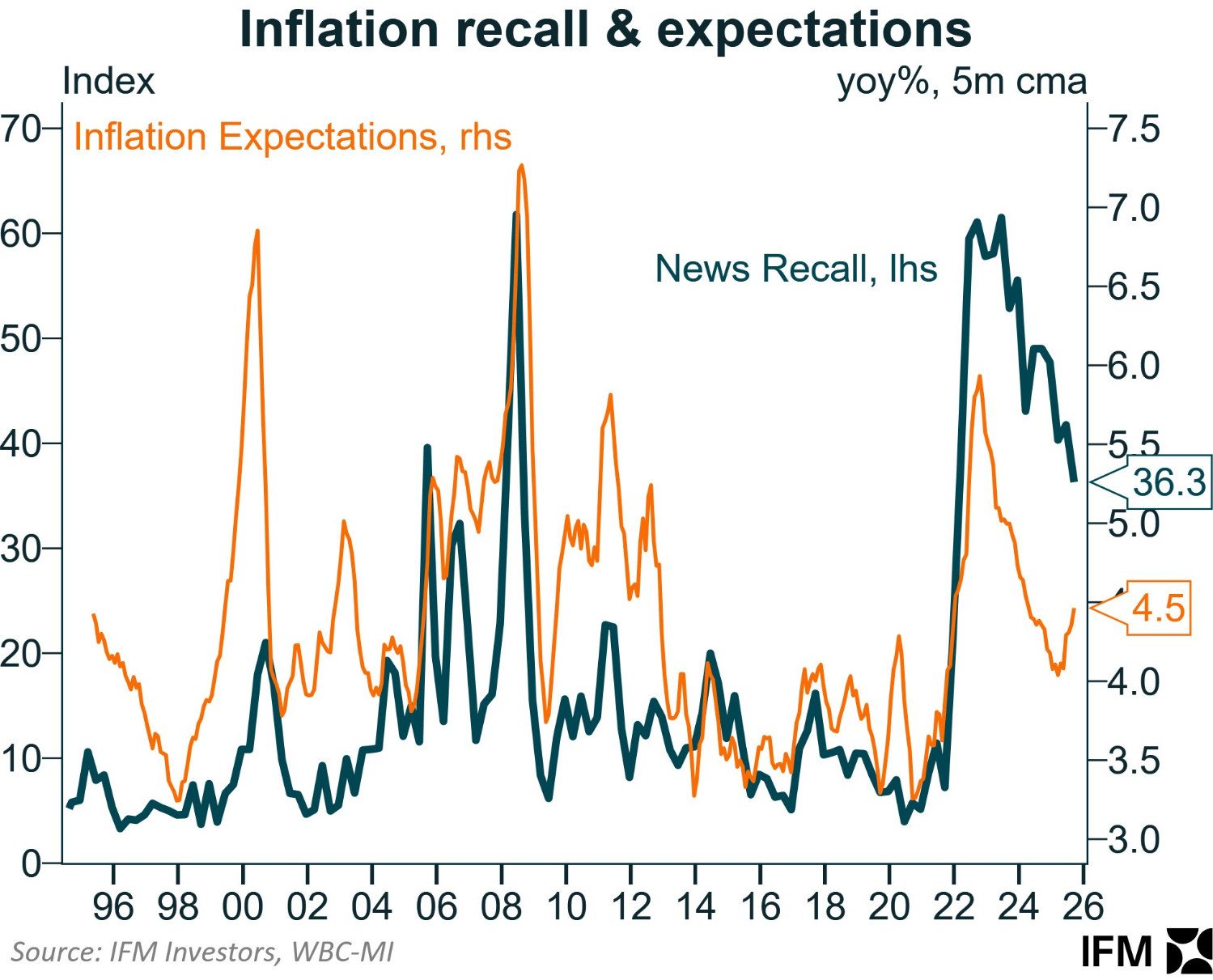

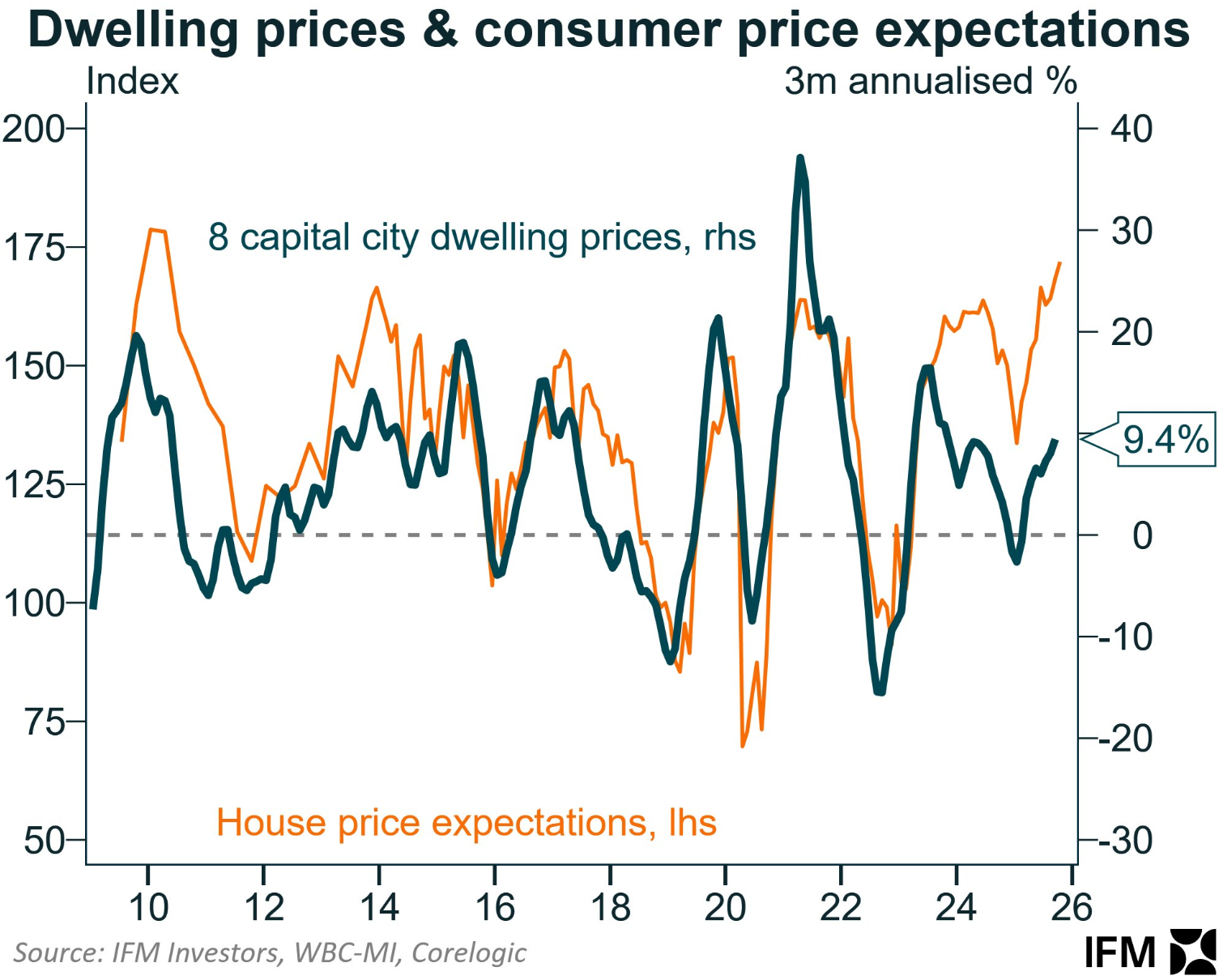

As Alex Joiner from IFM Investors shows below, Westpac’s latest consumer sentiment report shows that household inflation expectations have also rebounded:

While the RBA does not try to control house prices directly, it would also be somewhat concerned by the reacceleration of price growth and price expectations, which are tracking at a 15-year high amid feverish first-home buyer and investor demand.

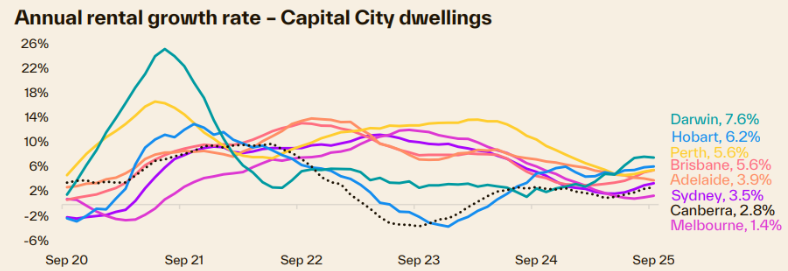

Advertised rents are also reaccelerating, which is a leading indicator for the “rents paid” component of the CPI.

Source: Cotality

“Along with some renewed upwards pressure from the cost of new dwellings, the potential for inflation to be higher than RBA forecasts could see the cash rate holding high for longer”, noted research director Tim Lawless in Cotality’s latest Quarterly Rent Review.

All of which suggests that the window for rate cuts is narrowing.

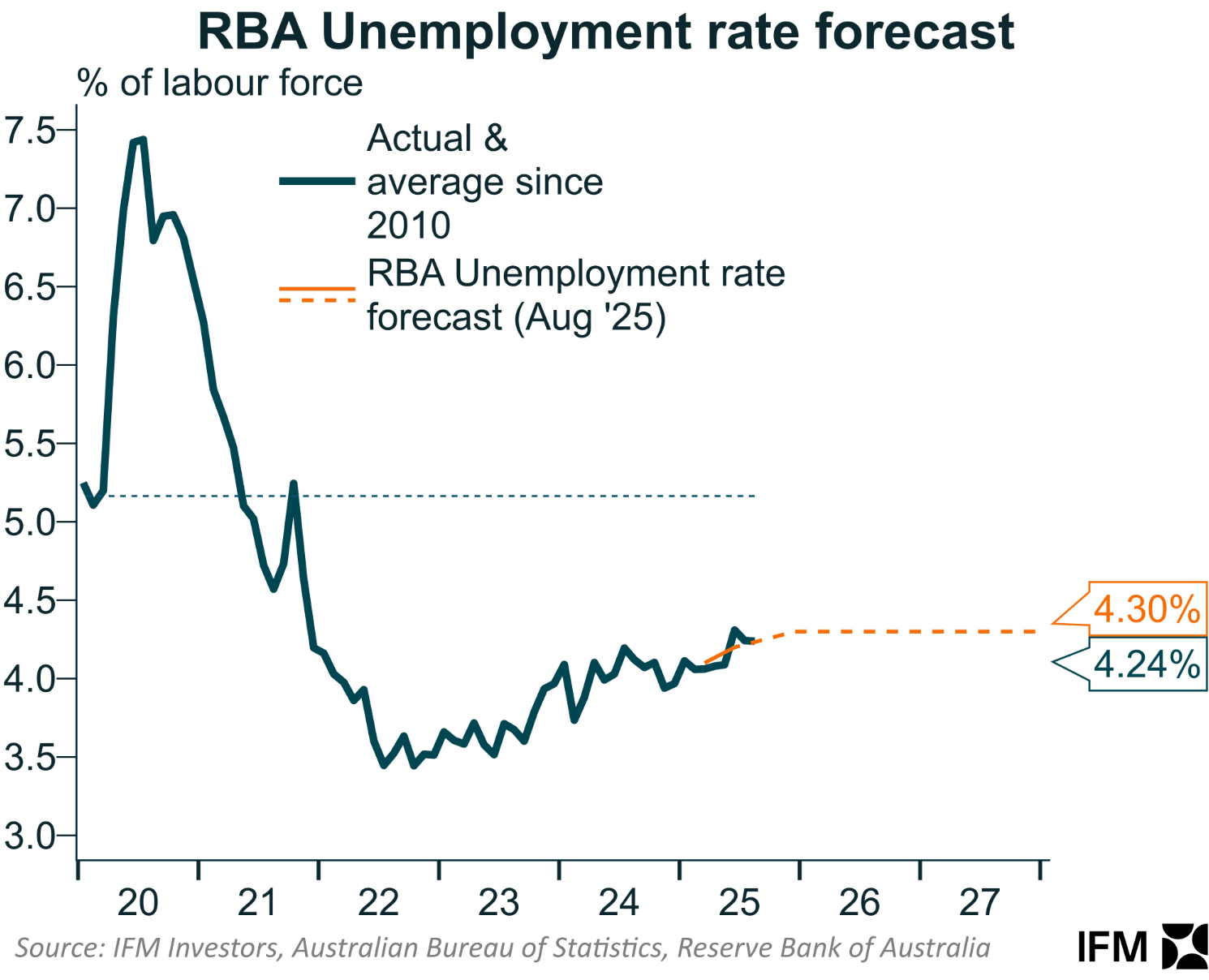

The saving grace would be a deterioration in the nation’s job market, given that the RBA forecasts that the unemployment rate will remain at its current level for the next two years.