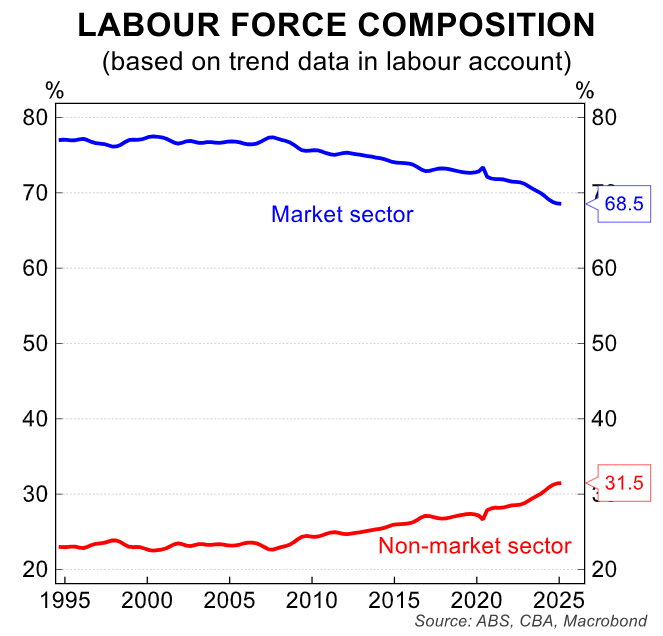

Since the pandemic kicked off in early 2020, around 60% of the nation’s job growth has been driven by the non-market (largely government-funded) sector, which comprises healthcare, social assistance, education, and public administration and safety.

As a result, the non-market sector now comprises a record high 31.5% of the Australian labour force.

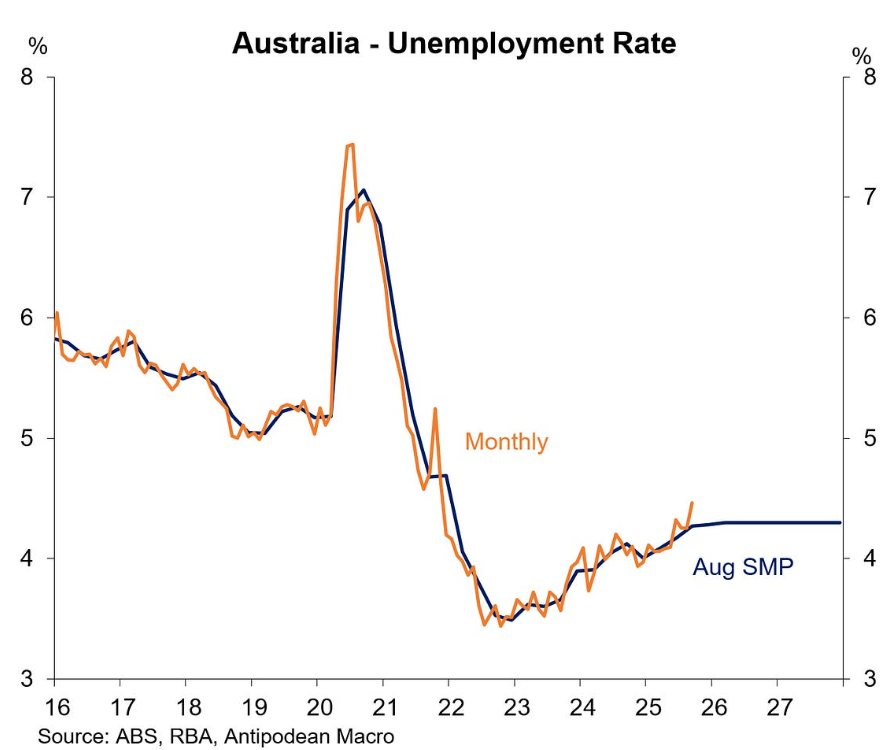

Last week’s Labour force release from the Australian Bureau of Statistics (ABS) reported that the nation’s headline unemployment rate rose to 4.5% in September, the highest rate since November 2021.

The seasonally adjusted unemployment rate of 4.5% is well above the peak rate of 4.3% projected by the RBA in its August Statement of Monetary Policy.

With the debt-ridden states now embarking on austerity measures and the federal government trying to curb the cost of the National Disability Insurance Scheme (NDIS), Australia needs the market sector to take over job creation from the non-market sector.

Westpac senior economist and former Treasury official Pat Bustamante told The AFR’s John Kehoe that Australia now faces a period of “jobless growth”. This is because private sector industries such as real estate services, professional services, and manufacturing are less labour-intensive than taxpayer-funded industries, such as healthcare and social assistance.

As a result, job growth will likely weaken despite an improvement in GDP growth, driven by the market sector.

“While the pick-up in private demand is expected to more than offset the slowdown in public demand in GDP terms, there are downside risks to the extent that this shift sees a material slowing in labour markets”, Bustamante noted.

If true, this implies that the unemployment rate will rise well above the RBA’s expectation, prompting additional rate cuts.

“The bottom line though is that if the gradual slowdown in labour markets becomes more abrupt then the consumer-led recovery could easily falter, requiring more rate cuts down the track”, Bustamante said.

Bustamante warns that Australia’s unemployment rate could rise to 4.75% by early 2026, although Westpac’s current forecast is 4.5%, the same rate as currently.

Westpac’s bearish assessment of Australia’s labour market explains why it has forecast three further 0.25% rate cuts by mid-2026, which is well below the median financial market forecast of only 1.5 more rate cuts:

Futures Market Cash Rate Pricing

Ultimately, the evolution of the labour market will be the key determining factor of how many further rate cuts the RBA delivers.