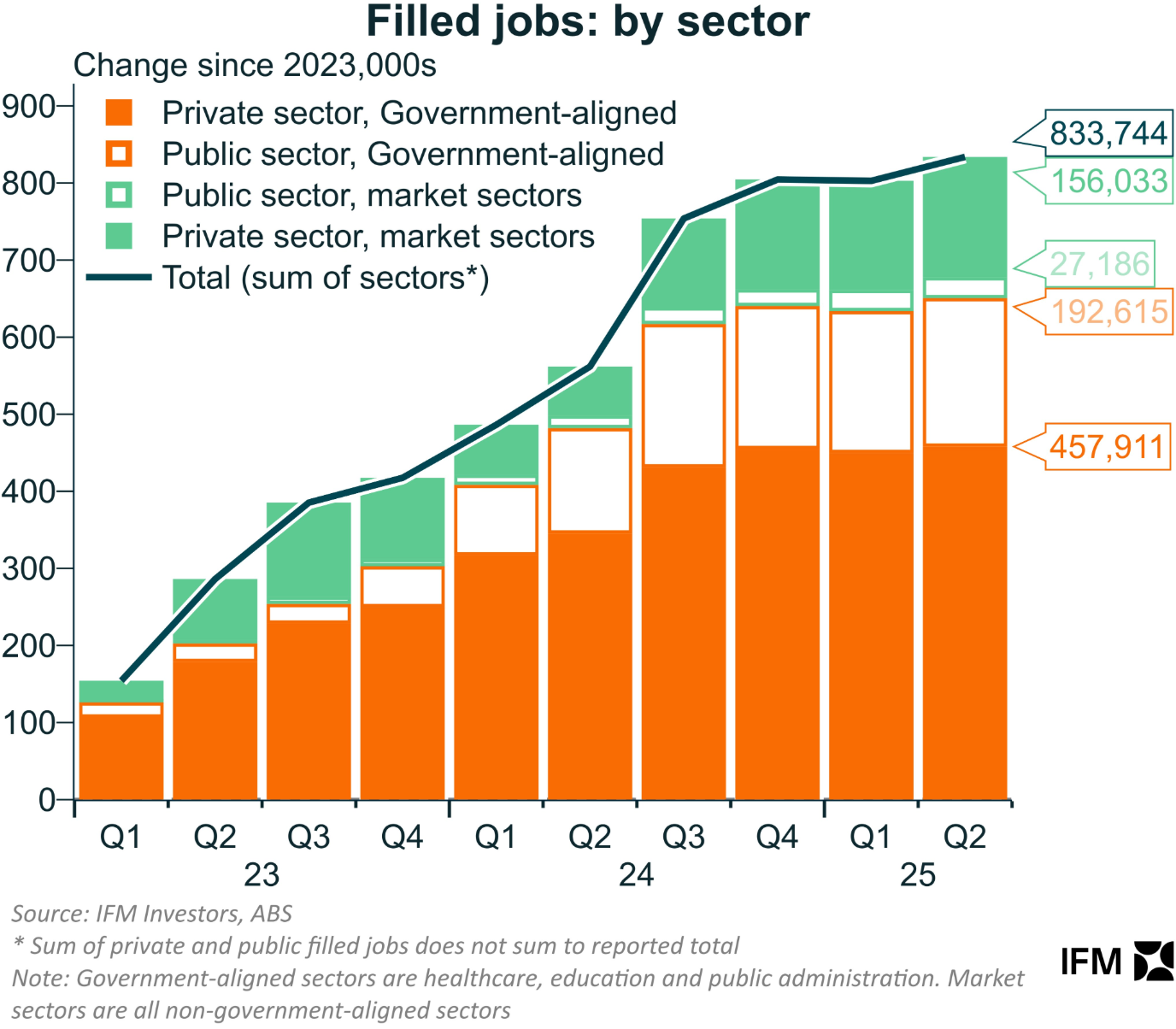

It was never a boom in the traditional sense. It was a fiscal stimulus into bedpan jobs, and it has ended.

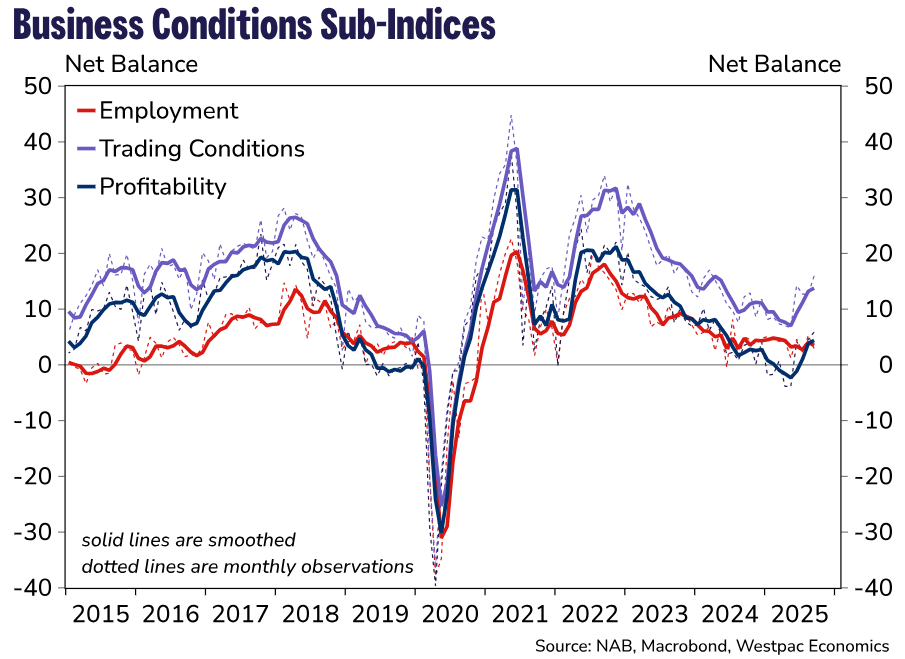

Owing to a far too slow RBA, the private sector is not well-positioned to pick up the slack. The NAB business survey is still consistent with weak hiring intentions.

More from Goldman.

Today’s update adds to evidence that labour market conditions have gradually softened this year and a further decline in the job-finding rate supports our view that conditions are not currently inflationary.

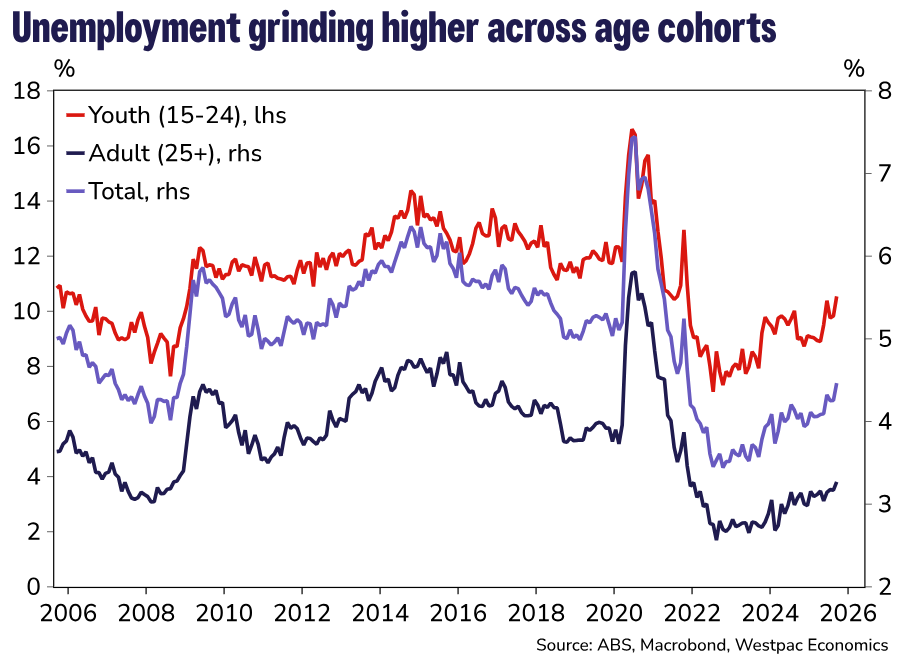

Youth unemployment is on the march higher.

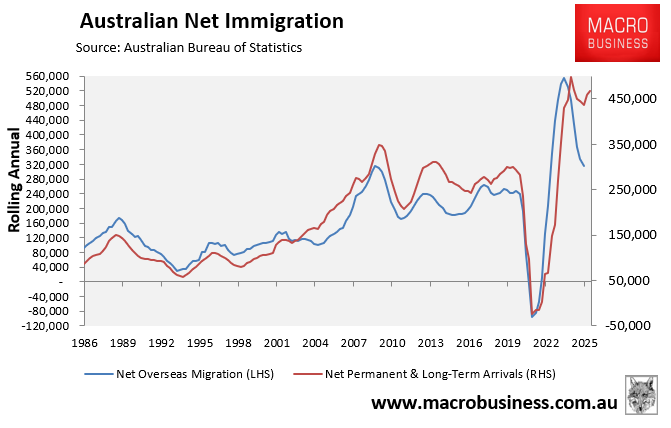

As Indian Albo pours in the cheap foreign competition for entry-level jobs. Don’t mention AI.

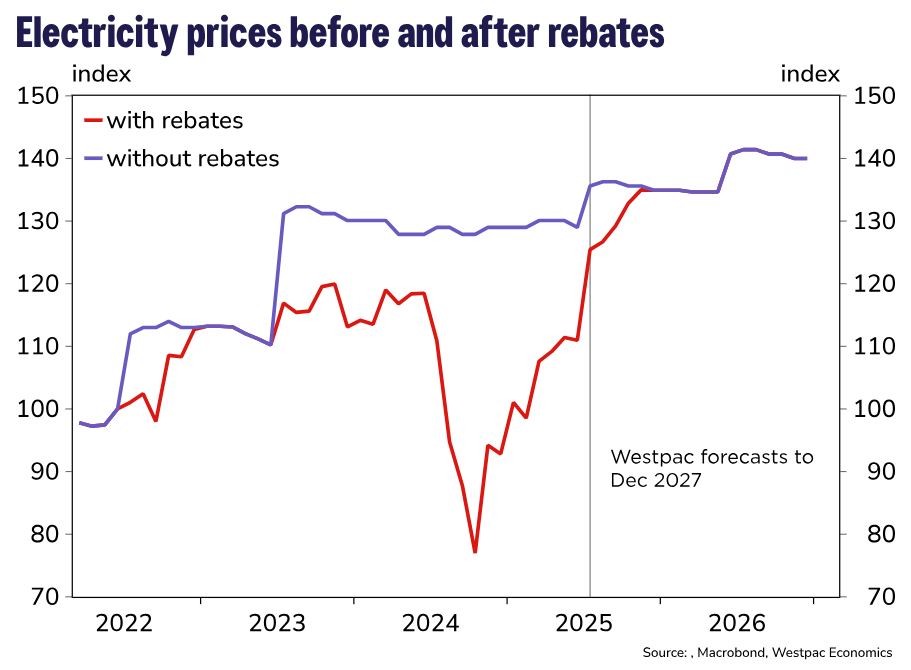

Australia’s two most important interest-rate-sensitive sectors to drive the rebound are not doing well, either. Consumers are burdened with an energy shock.

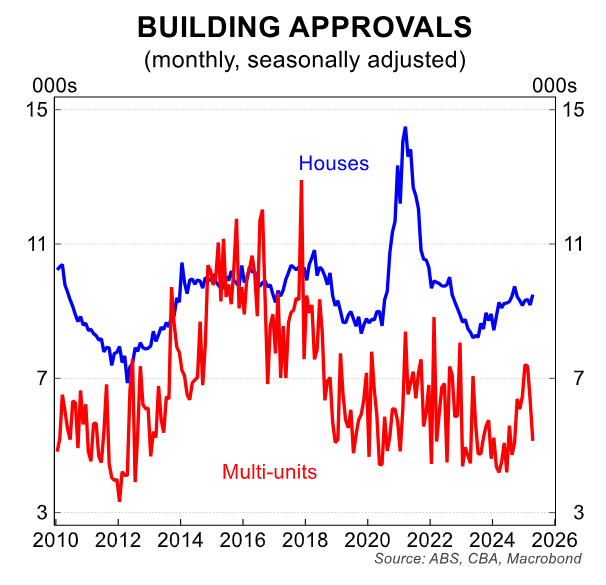

And the same has destroyed housing construction via building materials inflation.

Without an investment boom external to the native economy, like mining capex or fiscal stimulus, the immigration-led economy reverts to its basic form, which is excess labour supply, wage suppression, weak productivity and GDP.

The last cycle of this stupid economic model was made palatable by disinflation in rents and rock-bottom interest rates, materially driven by Chinese capital in apartment construction.

With Alboflation wrecking dwelling supply and rents sticky this time, the RBA has less room to go that low, though it will be forced lower into a handle 2-handle.

Unemployment is going to overshoot everybody’s forecasts.