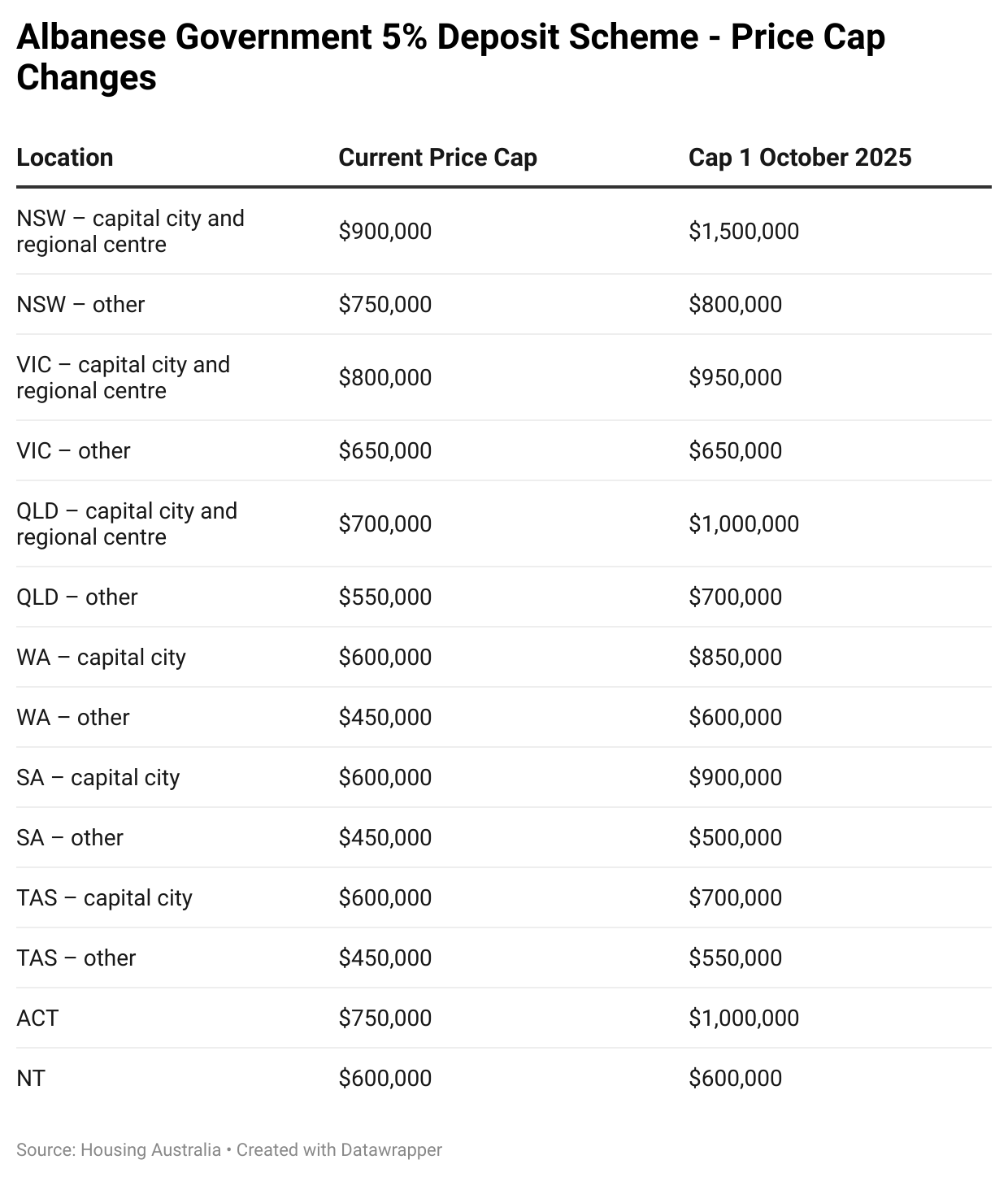

The Albanese government’s First Home Guarantee scheme came into effect on Wednesday, allowing almost all first home buyers to purchase a home with only a 5% deposit, without requiring lenders’ mortgage insurance, as taxpayers will guarantee 15% of the mortgage.

Analysis by Lateral Economics suggested that the 5% deposit scheme could increase home prices nationally by an additional 3.5% to 6.6% in 2026 and for several years afterwards.

However, in segments targeted by first-home buyers, which are defined as those below the scheme’s generous price caps, the impact is expected to be even greater, with home prices tipped to rise by an additional 5.3% to 9.9%.

“What that’s likely to do is add demand into a red-hot property market. Without a correlating increase in supply, prices are likely to go up even further, particularly fuelled by the three cash rate cuts we’ve already had this year”, Canstar’s director of data insights, Sally Tindall, warned.

“Certainly, being a member of this Home Guarantee scheme is one strategy to help these banks grow their lending books”.

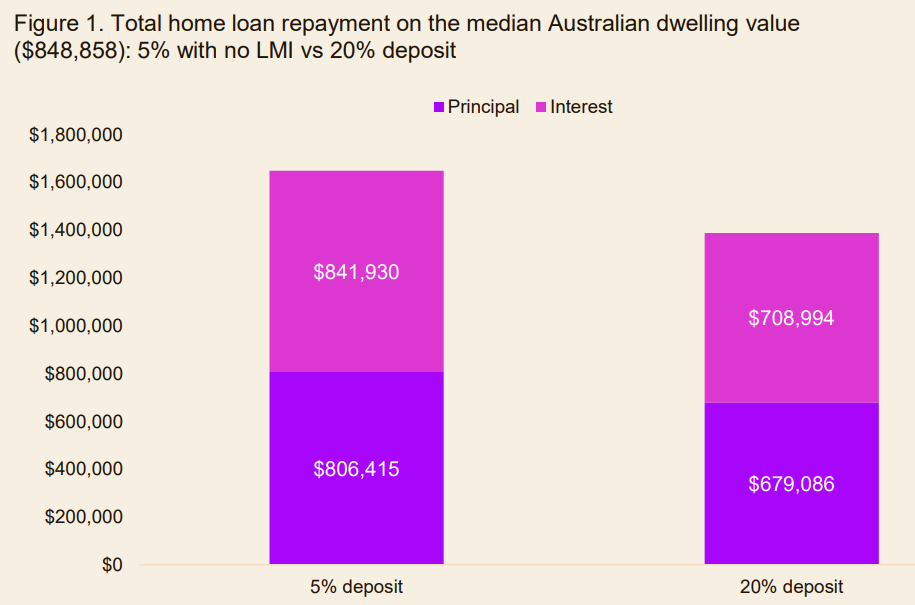

As illustrated below by Cotality, a buyer who purchases the median-priced home using the scheme would pay more than $130,000 in additional interest over the life of a 30-year loan, assuming an average mortgage rate of 5.5% per annum throughout the loan term.

Source: Cotality

The First Home Guarantee scheme is already proving very popular, with property industry professionals reporting strong interest from prospective first home buyers.

Sydney mortgage broker Nathaniel Truong told The ABC that higher-earning first-home buyers, previously locked out by income caps, are now flooding into the market.

“Even existing clients that have looked at property or had pre-approvals, we’re reworking from the 1st of October”, he said.

Truong said competition is heating up, with buyers able to borrow more under the Home Guarantee Scheme.

“I have a client who had a budget of about $1.15 million … but because of this new scheme, the property he ended up buying is $1.3 million”.

“Even though he saved about $30,000 to $40,000 in LMI, the property price did go up. So my question is: did you really save, or did you just spend more?”, he said.

Cotality’s head of research, Eliza Owen, warned that the First Home Guarantee scheme is a sugar hit that will benefit the first cohort of buyers but will disadvantage future first home buyers.

This is because early users of the scheme will ‘get in’ to the market before prices climb.

However, a few years later, after prices have risen, future first home buyers will be entering a market that is substantially more expensive than it would otherwise be. They will have lower deposits and substantially greater mortgage debt than they would otherwise.

“It’s encouraging first home buyers to go into more debt and ultimately making it harder for the next cohort of first home buyers”, Owen warned.

Given such small deposits, these buyers will also face the prospect of falling into negative equity if there is ever a significant correction in home prices.

Owen added that because the government will have encouraged first-home buyers to enter the market with skinny deposits and has guaranteed 15% of their mortgages, the government will be incentivised to implement policies that support rising home values.

“It also creates more skin in the game”, Owen said. “If you’ve got this cohort of first home buyers going in with debt levels of 95% on the value of their property, they’re going to want home values to go up over time”.

“That makes it harder to influence policy that would actually bring prices down in the future”, she said.

In other words, Australia’s housing market will become state-sponsored and supported.

I discussed these issues in an interview with Radio 3AW’s Tony Jones on Wednesday: