If you want bona fide proof that the Australian Treasury has become a propaganda arm of the federal government, look no further than its modelling of the impact of Labor’s 5% deposit scheme for first home buyers.

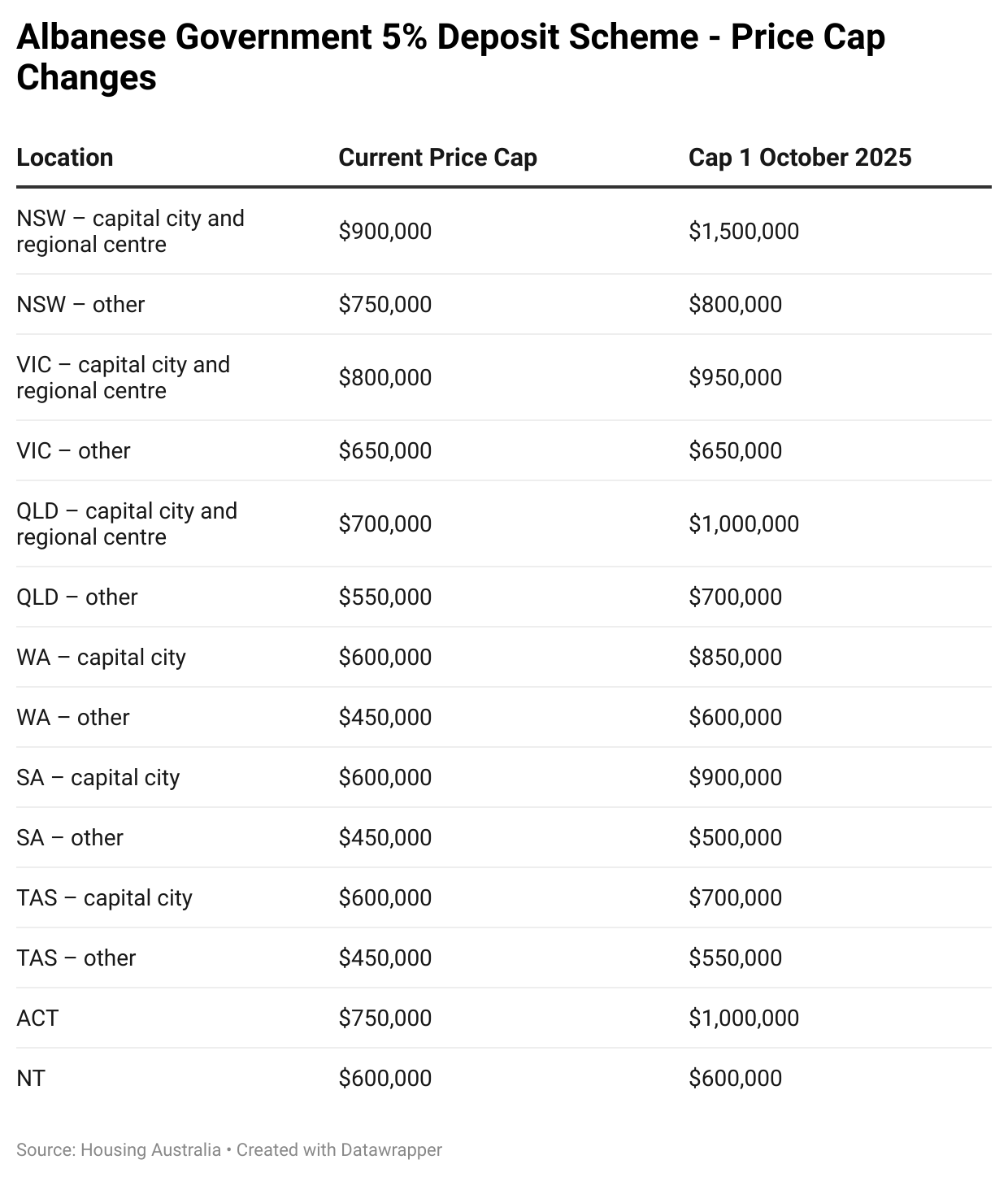

Under Labor’s First Home Guarantee scheme, which came into effect on Wednesday, almost all first home buyers can purchase a home with only a 5% deposit, without requiring lenders’ mortgage insurance, as taxpayers will guarantee 15% of the mortgage.

Treasury modelling released ahead of the scheme suggested the policy would only lift values by 0.5% over six years.

When questioned this week on the impact of Labor’s First Home Guarantee scheme, Prime Minister Anthony Albanese pointed to Treasury’s modelling to claim there will “be a slight increase” from the policy.

No analyst believes Treasury’s modelling.

For example, Lateral Economics forecast that the 5% deposit scheme could increase home prices nationally by an additional 3.5% to 6.6% in 2026 and for several years afterwards.

However, in segments targeted by first-home buyers, which are defined as those below the scheme’s generous price caps, the impact is expected to be even greater, with home prices tipped to rise by an additional 5.3% to 9.9%.

Canstar’s director of data insights, Sally Tindall, warned that the scheme will “add demand into a red-hot property market”, meaning “prices are likely to go up even further”.

Meanwhile, mortgage brokers and real estate agents have recorded a massive increase in interest from first home buyers seeking to take advantage of the scheme.

Sydney mortgage broker Nathaniel Truong told The ABC that higher-earning first-home buyers, previously locked out by income caps, are now rushing the market.

“Even existing clients that have looked at property or had pre-approvals, we’re reworking from the 1st of October”, he said.

Truong said that competition is heating up, with buyers able to borrow more under the scheme.

“I have a client who had a budget of about $1.15 million … but because of this new scheme, the property he ended up buying is $1.3 million”.

“Even though he saved about $30,000 to $40,000 in LMI, the property price did go up. So my question is: did you really save, or did you just spend more?”, he said.

Sydney eastern suburbs mortgage broker James Watson told The AFR that he had already submitted three applications on the first day of the scheme and would process dozens more over the coming weeks.

“There is unprecedented demand and people are literally queuing up to submit the application”, he said.

However, Watson warned that the First Home Guarantee scheme is a sugar hit that will benefit the early movers but will disadvantage future first home buyers.

“It’s really only going to benefit the first movers because I think prices are going to adjust higher given the amounts of people who are inquiring”, he said.

Meanwhile, Nicola Powell, chief of research and economics at Domain, warned that the policy would drive up prices in more affordable areas typically targeted by first-home buyers, such as apartments and fringe housing estates.

“We’re going to see higher prices for more affordable homes from this first home buyer incentive”, she said.

Nerida Conisbee, chief economist at national real estate firm Ray White, agreed arguing that the scheme will “lead to faster growth for the more affordable part of the market up to the price point where the 5% scheme cuts out for each capital city”.

The reality is that, just like every other demand-side policy stimulus implemented over the past 25 years, it will quickly get capitalised into higher prices and larger mortgages, making the scheme self-defeating from an affordability perspective.

The only way that Treasury’s 0.5% price impact over six years would come true is if, after the inevitable boom, prices correct lower.

However, this scenario would result in recent first-home buyers having negative equity and taxpayers bearing the burden of any mortgage default.

Moreover, because the government will have encouraged first-home buyers to enter the market with skinny deposits and will have guaranteed 15% of their mortgages, the government will be incentivised to implement policies that support rising home values.

Australia’s housing market will effectively become state-sponsored and supported.

I discussed these issues on this weekend’s Treasury of Common Sense on Radio 2GB/4BC.