DXY is fading again.

AUD has bounced but not very convincingly.

CNY stable.

That is a golden parabola.

AI metals not so much.

RIO has broken the big bear downtrend.

EM strong bounce.

Junk not so much.

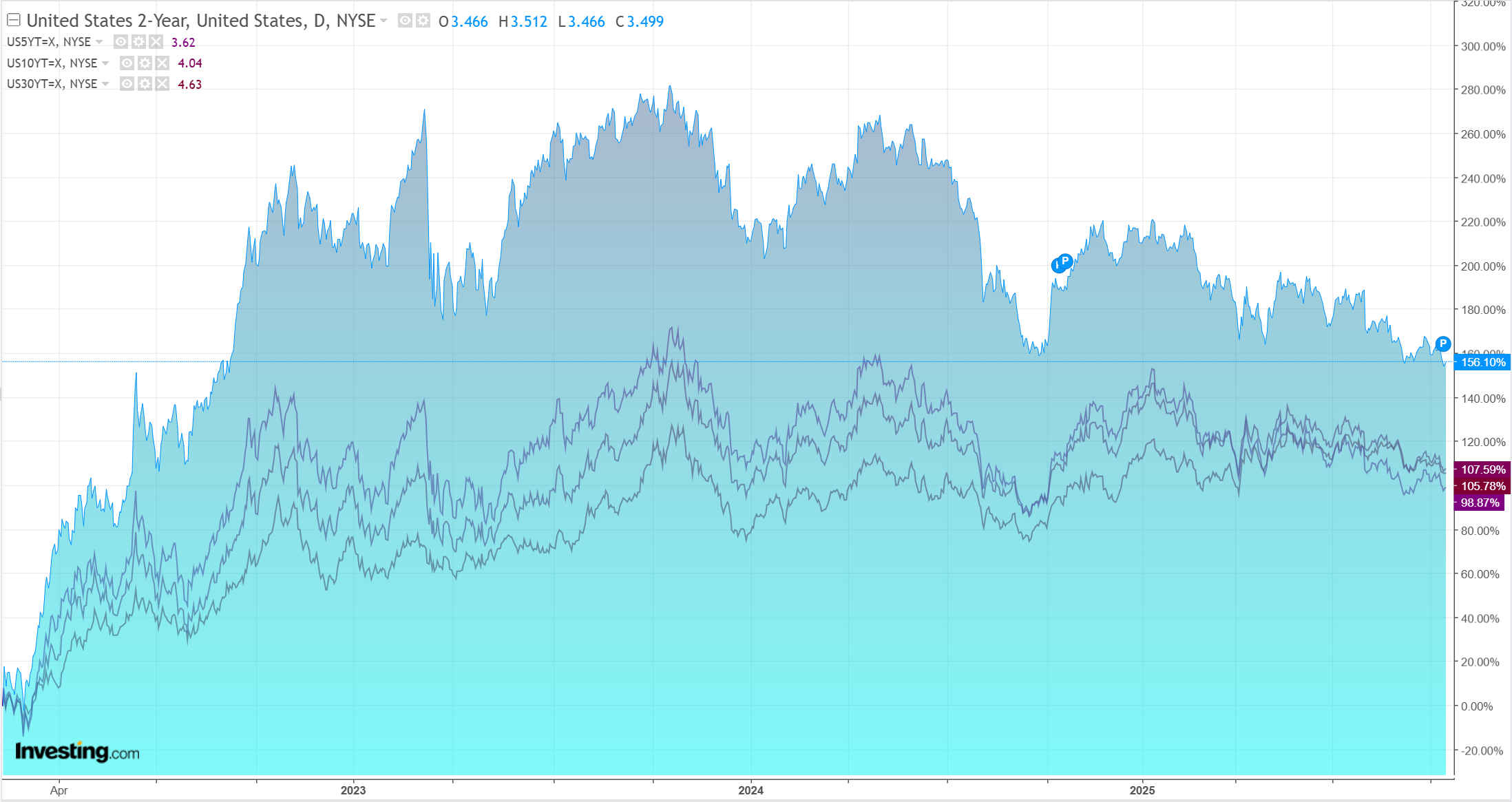

Yields firmed.

Bulls returned.

One should expect more volatility as we approach the Trump/XI walkover. The balance of power has clearly shifted with Scott Bessent rolling over.

- Treasury Secretary Scott Bessent proposed a longer pause on high US tariffs on Chinese goods in return for Beijing putting off its plan to tighten limits on critical rare earths.

- US Trade Representative Jamieson Greer cast doubt that Beijing would go ahead with the plan, which he said would choke off trade in a wide variety of consumer products that contain even a trace of rare earths.

- Bessent predicted a coordinated response to China’s move from the US and several allies, saying “We’re going to have a fulsome, group response to this, because bureaucrats in China cannot manage the supply chain or the manufacturing process for the rest of the world.”

Why not? They’ve been doing so for over twenty years now. They seem to be willing to give it a try.

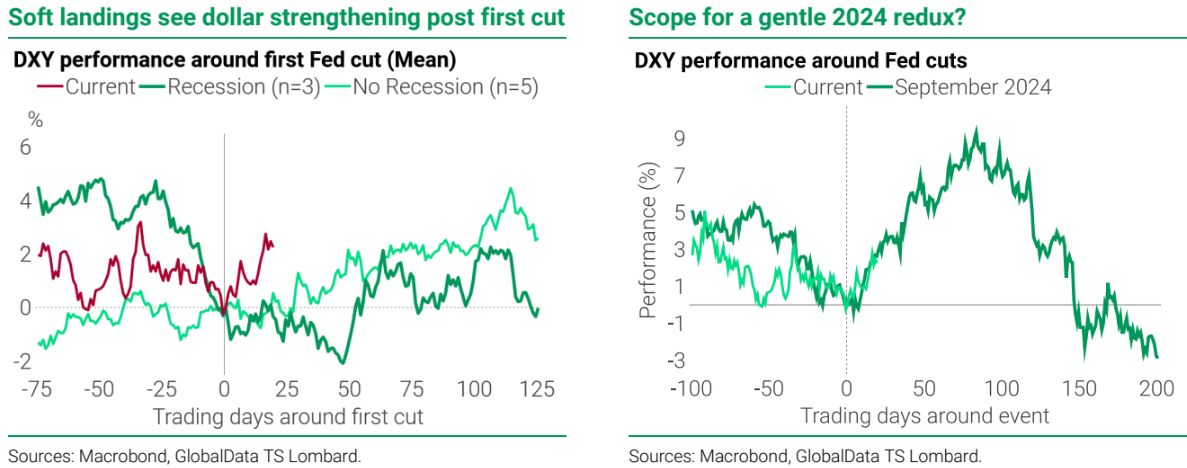

I am still of the view that it will be difficult for AUD to rise into any of this, and DXY has stopped falling. TS Lombard sees it rising next.

USD: Cyclical strength into year end.

The DXY index has rebounded over the past month, and we think the current bout of USD strength has more room to run.

Fed cuts are not necessarily USD bearish, judging from cutting cycles since 1984; in fact, in non-recessionary easing cycles the dollart ends to strengthen in the first six months following the first cut.

As a meaningful easing campaign is already priced into USD STIR markets (two more Fed cuts by year end),

US growth will have to underwhelm expectations for the dollar to fall from here (H2 US GDP expectations still imply a low bar for beats, with Q3 and Q4 expected at 1.7 and 1.4% q/q SAAR,respectively).

Moreover, Fed speak has become more hawkish recently(from several FOMC members–including Musalem, Goolsbee and Hammack), which will matter beyond October.

US hiring is set to pick up again over the coming months.

As far as the US labour market is concerned, the breakeven job rate has likely dropped significantly, which means the labour market might not be as weak as feared (FRB Dallas research currently puts the breakeven rate at~30k net job gains a month).

As the fiscal impulse will flip positive next year (OBBBA tax cuts start to kick in) and major US macro imbalances are few and far between, we think hiring will pickup over the coming months, obviating the need for the Fed to cut aggressively amid unresolved inflationary pressures.

That looks a solid argument to me. With no immigration, a 30k job breakeven rate is phenomenal.

In Aussie terms, that would translate to a 3k jobs per month breakeven rate.

Yeh, nah, import the warm bodies!

AUD has headwinds.