Well, that escalated quickly. DXY fell.

But AUD crashed.

Gold held, oil was murdered.

AI metals were deleted.

The big bear is back.

EM ouch.

Led by junk is bearish.

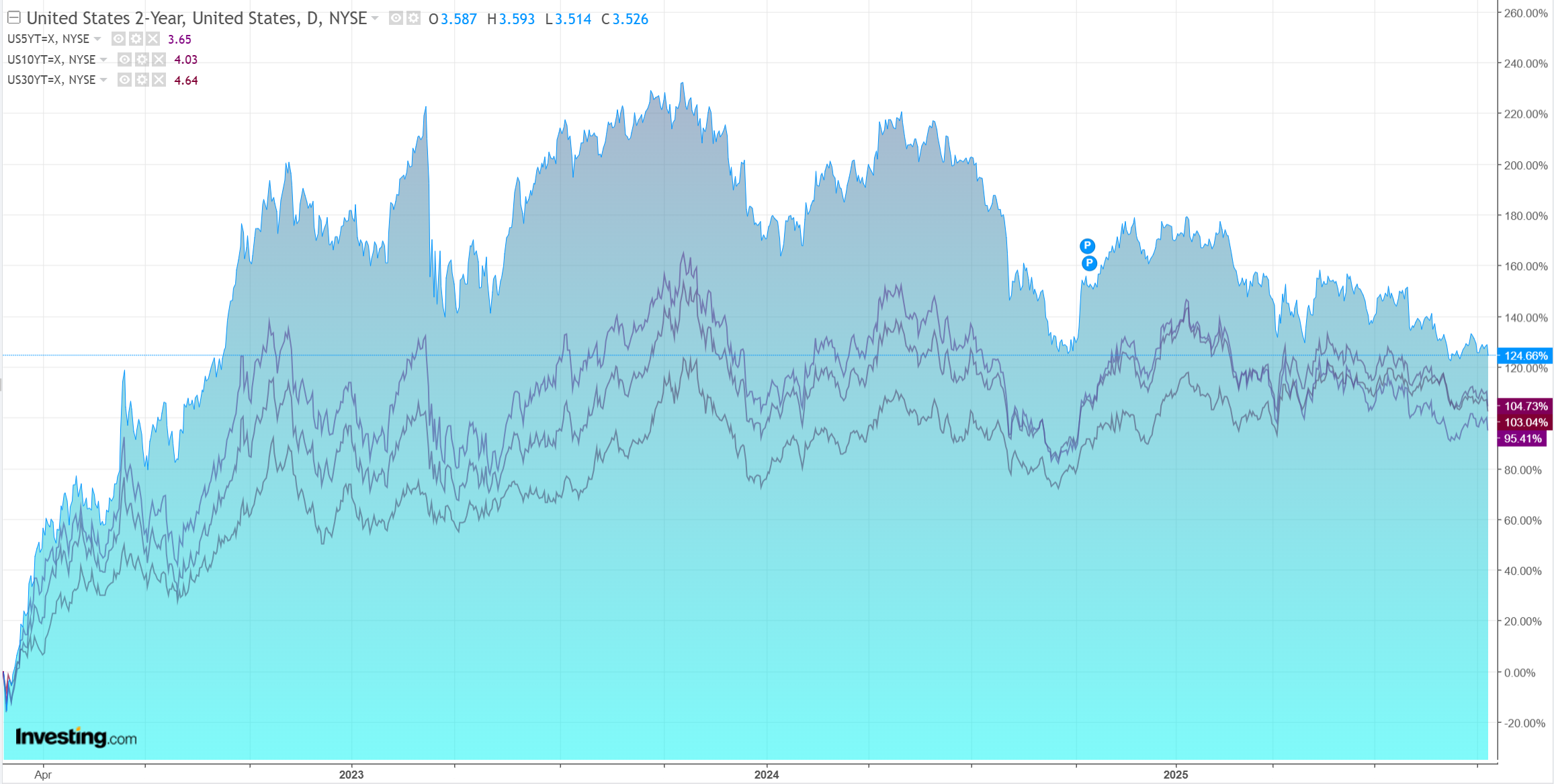

Despite a weak DXY , the full bond curve was bid. This will be critical as tariffs return.

The stock bubble just burst.

It’s not complex.

US President Donald Trump said he would impose an additional 100% tariff on China as well as export controls on “any and all critical software” beginning Nov. 1, hours after threatening to cancel an upcoming meeting with the country’s leader, Xi Jinping.

Yet, underneath that, there is something else going on in credit markets.

Demand for risky debt has softened in the past few weeks for a number of reasons. Primarily, debt offerings tied to acquisitions and buyouts have picked up, giving investors an opportunity to get better returns than those offered on repricings.

Some investors have also been spooked by the bankruptcy of auto-parts supplier First Brands, which filed after failing to complete a $6 billion refinancing. And concerns about higher costs in the chemical sector impacted demand for Nouryon’s offering.

Secondary-market prices, meanwhile, have fallen almost every day for the last two weeks, a Bloomberg index shows.

I’m not overly alarmed by this for now, but the chance of a feedback loop between junk spreads and geopolitics can’t be ignored.

As we know, equities are pumped so fat that it’s not going to take much to get a pretty sizeable VaR shock going.

Watch the long end of the bond curve. So long as it stays anchored, then the latest Trump tantrum will be contained in forex.

That said, if there is no spread widening in long-end yields like there was after Liberation Day, then Trump will feel less pressure to back off China.

Until the fear of a growth shock pops the stock bubble.

AUD is in the gun!