Australia the world leader in loading households with debt

Australia is the world’s leader in creating products and policies that load households with debt.

This year, we have seen the federal Labor government introduce its 5% deposit scheme for first home buyers as well as exclude student debts from loan servicing calculations.

We have also seen Australian lenders announce new stimulatory mortgage products, including 40-year mortgage terms and 10-year interest-only terms without reassessment.

The above policies and mortgage products are aimed squarely at boosting borrowing capacity, mortgage demand, and home prices.

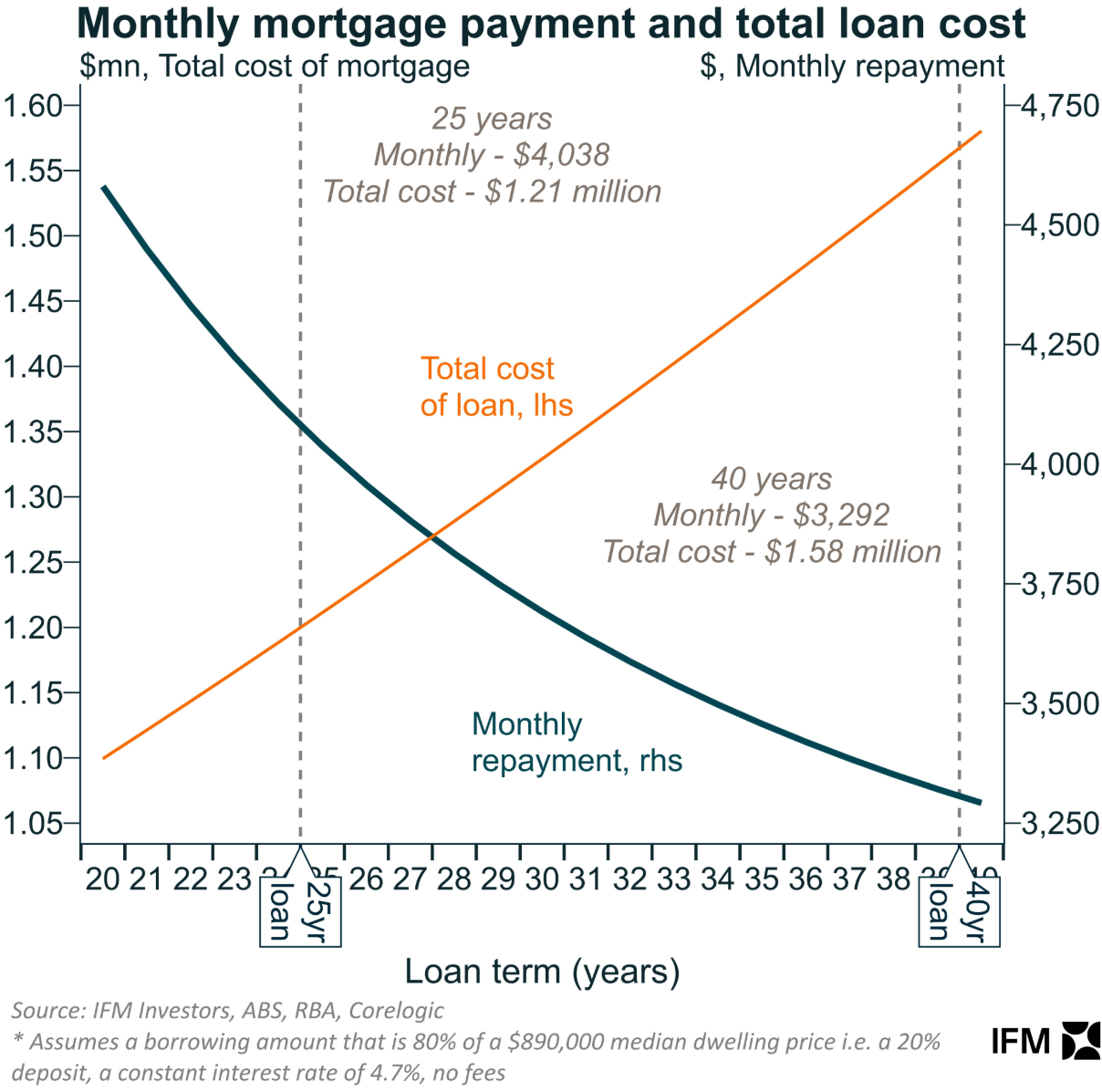

For example, the following chart from Alex Joiner at IFM Investors shows how a lengthier 40-year mortgage term increases borrowing capacity:

A longer loan term decreases monthly repayments. However, total payback costs will increase, and more Australians will carry mortgage debt into retirement.

The added stimulus from increased mortgage borrowing will also bid up dwelling values, making housing structurally less affordable.

Indeed, this has been the Australian story this century, with demand-side policies forever being capitalised into higher home prices:

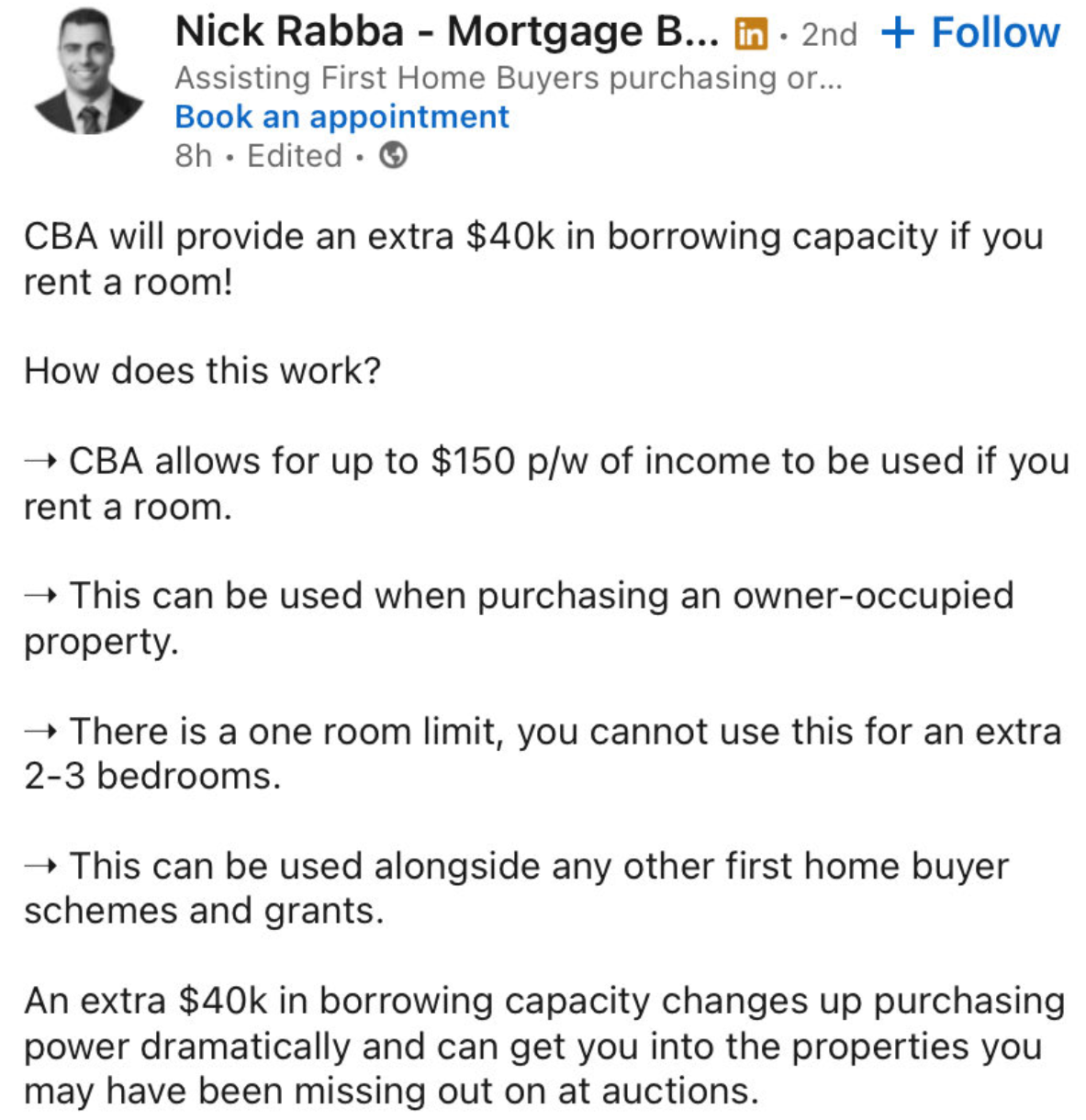

The latest “innovation” designed to load Australian households with debt and pump home prices comes from CBA, which will provide buyers with $40,000 in extra borrowing capacity if they rent out a room:

This product from the CBA could be easily gamed by buyers. All they need to do is say that they intend to rent a room out and then not follow through.

Moreover, if they do formally rent a room out, wouldn’t such an arrangement raise a tax obligation, both income tax and potential CGT on sale?

Regardless, it appears that the banks have free rein to pump mortgage demand. Australia’s financial regulators will not stop them.

Who knows how far house prices can inflate amid simultaneous pump priming from the federal government, banks, and the RBA?

At some point there will be a reckoning, like in New Zealand and Canada. But not before home prices bubble higher.