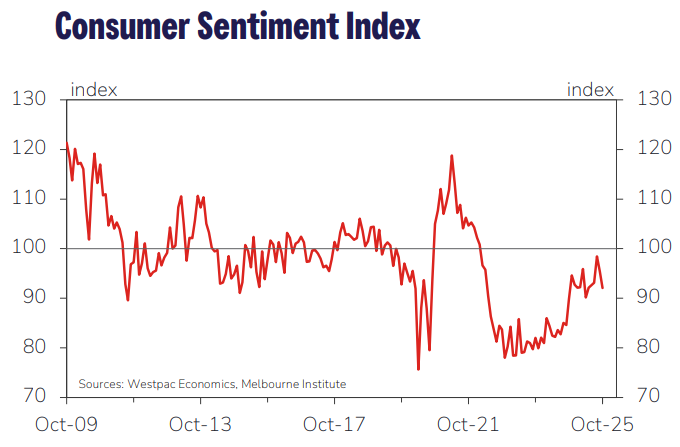

After a months-long rebound, Westpac’s monthly consumer sentiment index crashed back to a 6-month low in September as hopes of deep interest rate cuts faded.

Westpac’s Head of Australian Macro-Forecasting, Matthew Hassan, explains the results below.

Key Points:

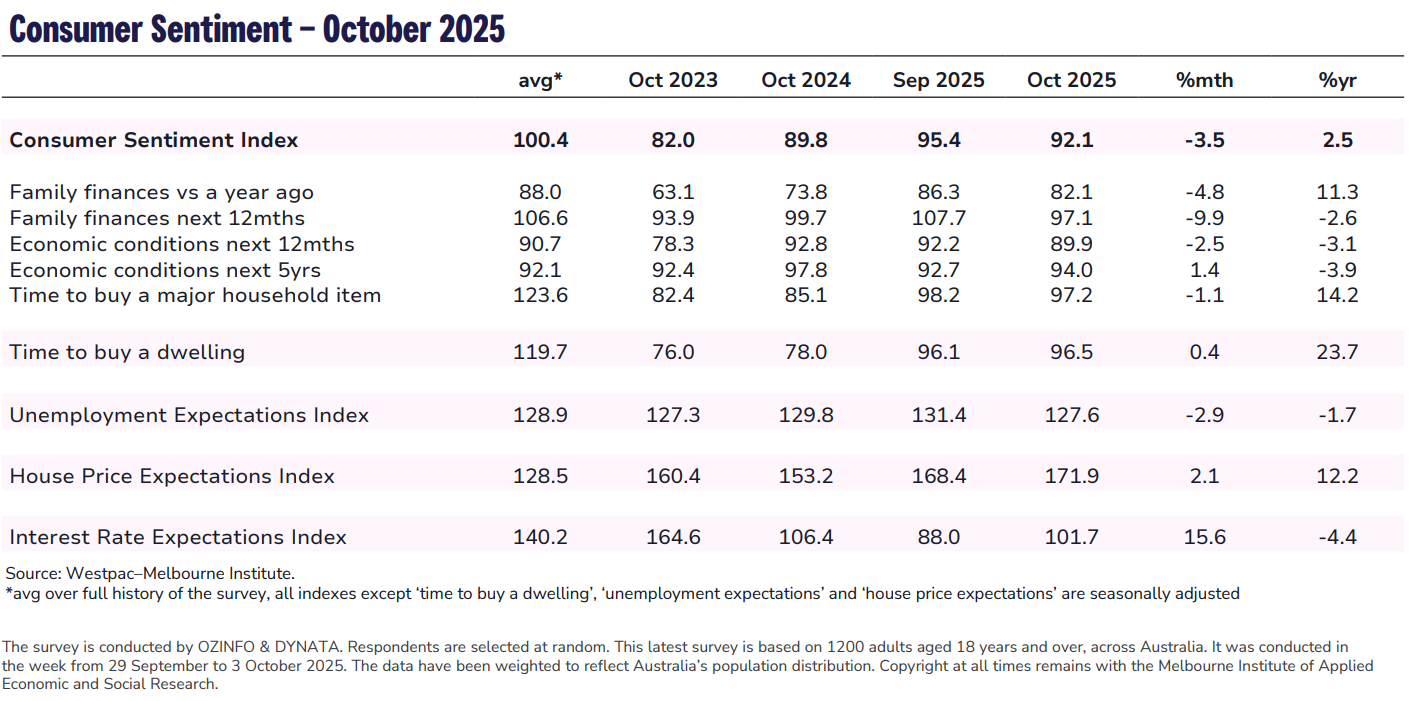

- Westpac Consumer Sentiment Index declines 3.5% to 92.1 in October.

- Optimism about outlook for family finances fades.

- Consumers less certain about direction of interest rates.

- Unemployment expectations hold firm around average levels.

- House price expectations hit new 15-year high.

The Westpac–Melbourne Institute Consumer Sentiment Index declined 3.5% to 92.1 in October from 95.4 in September.

Consumer confidence has fallen 6.5% over the last two months, giving back all of the gains seen between May and August when rate cuts were giving a clear boost. At 92.1, the October Index read is now at firmly pessimistic levels, albeit still well above the very weak reads seen during the extended ‘cost-of-living’ crisis.

Consumers appear to have been rattled by recent updates on inflation. ‘Partial’ measures released over the last month suggest annual inflation has lifted back towards the top of the RBA’s 2–3% target range. This news, and signs of firmer consumer demand and a pick-up in housing markets, looks to have sparked

renewed doubts about the path of interest rates, weighing on near-term expectations for family finances and the economy.

Interestingly, responses over the course of the survey week show the RBA’s decision to leave rates on hold at its September meeting went some way towards calming these fears.

Sentiment was 2–3pts lower amongst those surveyed prior to the RBA decision with this sub-group clearly bracing for a more hawkish decision. Just over half expected mortgage interest rates to rise over the next 12 months, compared to about a third of respondents surveyed after the announcement.

For the survey as a whole, the component detail showed the latest weakening centred on more downbeat views on the near-term outlook, especially prospects for family finances.

Recall that the Consumer Sentiment Index is a composite measure based on five sub-indexes: two tracking assessments of family finances, two tracking expectations for the economy and one on whether consumers see now as a good time to buy a major household item.

Four of the five sub-indexes recorded declines in October.

Assessments of family finances recorded the biggest falls.

Forward views saw a particularly marked deterioration, with the ‘family finances, next 12 months’ sub-index down nearly 10% to 97.1. This is the weakest read in just over a year and only the second ‘net pessimistic’ sub-100 read since November.

Current assessments were also downgraded, suggesting some of the support coming from policy—both this year’s interest rate cuts and last year’s tax cuts—may be starting to wane.

The ‘family finances vs a year ago’ sub-index was down 4.8% to 82.1, unwinding just over half of the gain over the previous two months.

Consumers were also more downbeat on near-term prospects for the economy. The ‘economic outlook, next 12 months’ subindex declined 2.5% to 89.9, the weakest read in a year. Medium to longer-term expectations were more resilient, though. The ‘economic outlook, next 5 years’ sub-index nudged 1.4% higher

to 94, a touch above the long-run average of 92.

Attitudes towards spending remain cagey. The ‘time to buy a major item’ sub-index dipped 1.1% to 97.2 in October, staying in slightly pessimistic territory after a brief nudge into positive in August. Despite a 22% rise since June last year,the sub-index is well below its long-run average read of 124.

Consumers may be less constrained financially but they still look likely to be very value-conscious heading into the peak retail sales periods in November–December.

The Westpac–Melbourne Institute Mortgage Rate Expectations Index, which tracks consumer expectations for variable mortgage rates over the next 12 months, jumped 15.6% to 101.7. As noted, there were big swings over the course of the survey week with much more hawkish responses early on.

Amongst those surveyed after the RBA decision, just over two-thirds of those with a view expected mortgage rates to be the same or lower in a year’s time. That compares to 61% across the full sample in October and 69% in the September survey.

While sentiment has been shakier, consumers are still not concerned about the outlook for jobs. The Westpac–Melbourne Institute Unemployment Expectations Index declined 2.9% to 127.6 in October (recall that lower index reads mean more consumers expect unemployment to fall over the year ahead). That takes the index slightly below its long-run average but still broadly consistent with a stable labour market.

Homebuyer sentiment was largely unchanged in October, with the ‘time to buy a dwelling’ index up only slightly by 0.4% to 96.5. The state breakdowns continue to show homebuyer sentiment relatively positive in Victoria (108) and about neutral in New South Wales (98) but more downbeat and choppier month to month in Queensland (86) and Western Australia (87). Even so, all state measures remain well below longer-run averages in the 116–124 range.

In contrast, the bullish consensus on house price expectations has continued to strengthen. The Westpac–Melbourne Institute Index of House Price Expectations rose another 2.1% in October, hitting a fresh fifteen-year high of 171.9.

Just over three-quarters of consumers expect prices to rise over the next 12 months. Expectations are stronger still in Queensland (184) but lagging a touch in Victoria (165) and Western Australia (166).

The Reserve Bank Monetary Policy Board (MPB) next meets on November 3–4. With inflation within the target range and monetary policy still a little on the restrictive side, the next rate move can reasonably be expected to be down. However, the MPB remains cautious, especially after the stronger than expected result for the August CPI indicator, and it will be sensitive to the flow of data from here.

A cash rate cut in November is far from assured, though neither is it off the table. And the longer the MPB delays further cuts, the more likely it is that it will end up cutting by more than it currently envisages.