The Albanese government launched its 5% deposit scheme for first-home buyers at the start of the month.

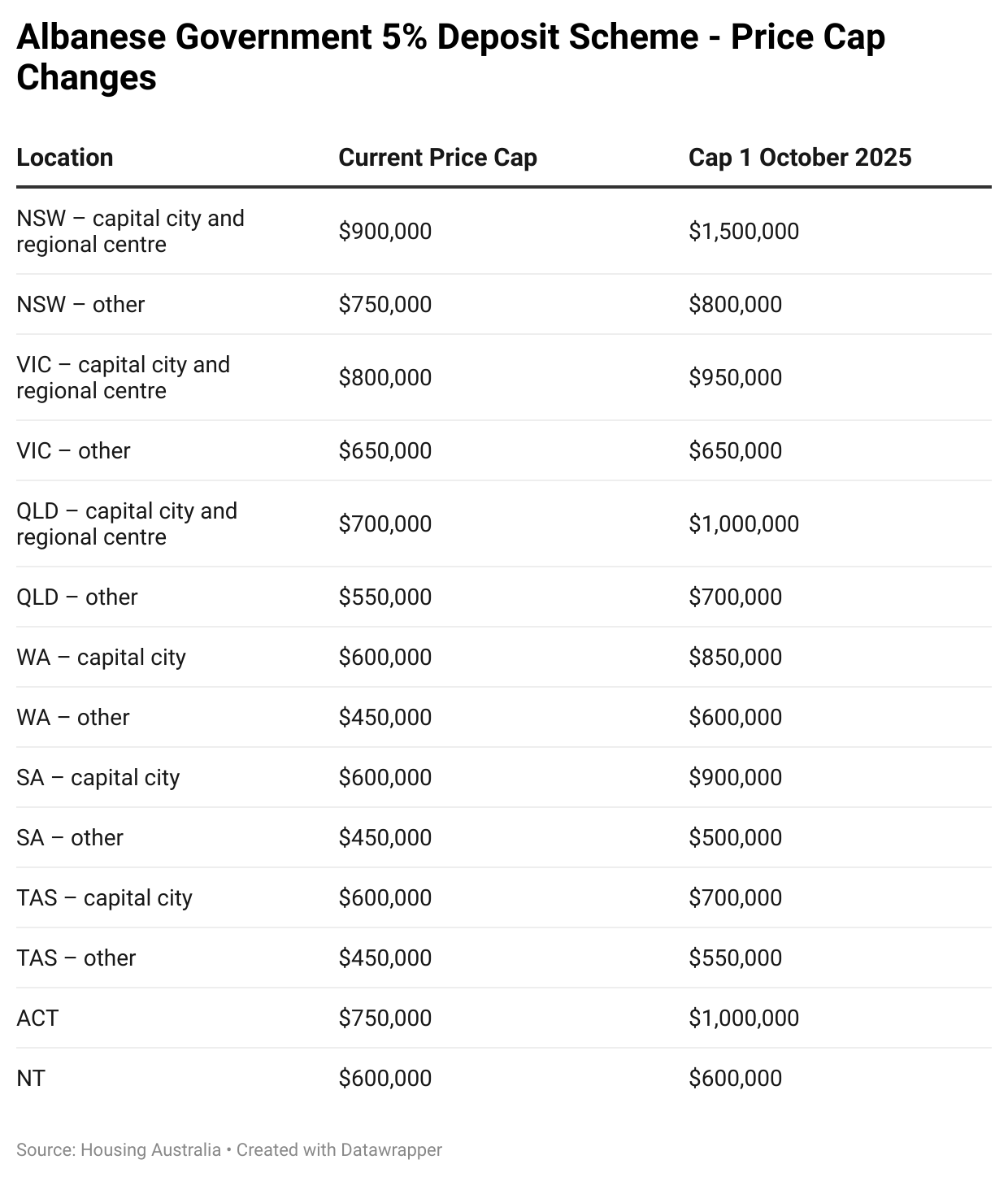

The First Home Guarantee scheme allows an uncapped number of first-home buyers to purchase a home using only a 5% deposit, provided they do not exceed the generous price caps illustrated in the following table.

For every home bought under the scheme, the government will guarantee 15% of the purchase price, therefore avoiding the need for low-deposit buyers to purchase lenders’ mortgage insurance.

Thus, Labor’s First Home Guarantee is a state-sponsored low-deposit mortgage scheme.

Lateral Economics forecasts that the 5% deposit scheme could increase home prices nationally by an additional 3.5% to 6.6% in 2026 and for several years afterwards.

However, in segments targeted by first-home buyers, which are defined as those below the scheme’s generous price caps, the impact is expected to be even greater, with home prices tipped to rise by an additional 5.3% to 9.9%.

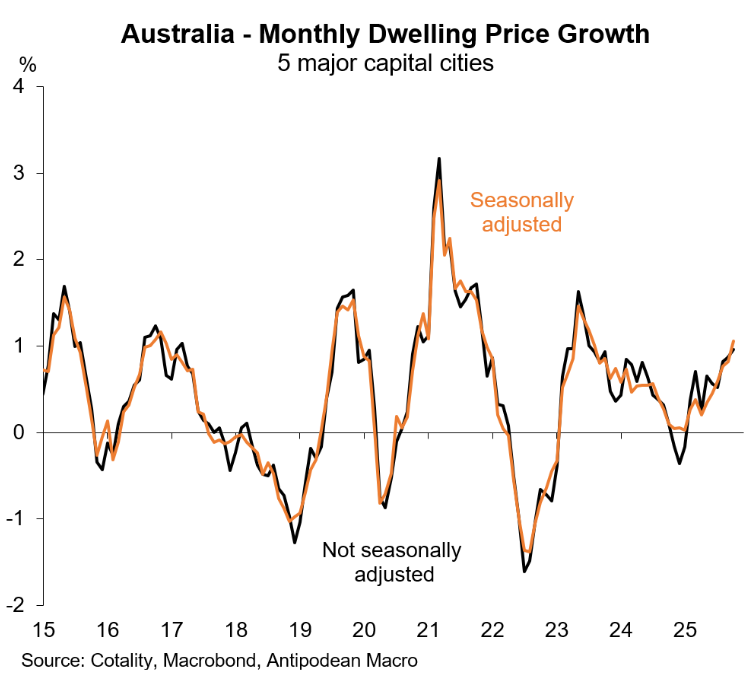

Cotality’s daily dwelling values index suggests the First Home Guarantee is already working to inflate prices.

As illustrated below by Justin Fabo from Antipodean Macro, seasonally adjusted price growth has surged to its highest level in two years:

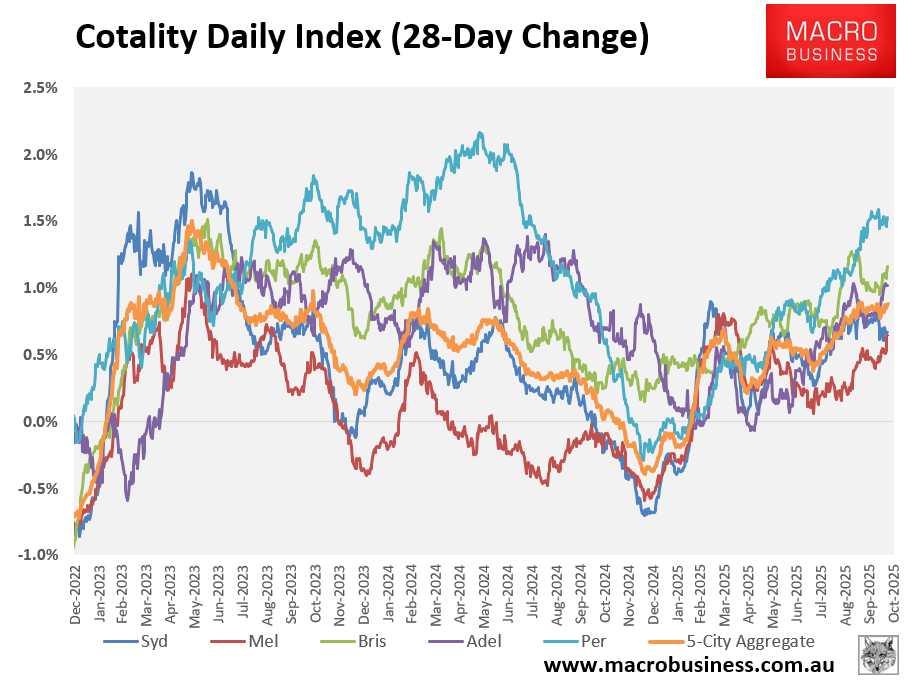

The following chart, which plots the same series in raw terms across the five major capital city markets, shows that prices are trending higher:

At the 5-city aggregate level, values have risen by 0.9% over the past 28 days, which is the strongest growth since October 2023.

To add more fuel to the bonfire, financial markets are now tipping that the Reserve Bank of Australia (RBA) will deliver a further 0.25% interest rate cut by the end of 2025, either at the RBA’s November or December meeting.

Markets are then tipping another 0.25% rate cut by mid-2026.

The weight of stimulus, therefore, suggests that Australian home prices will rise strongly into 2026 and become even more absurdly expensive.