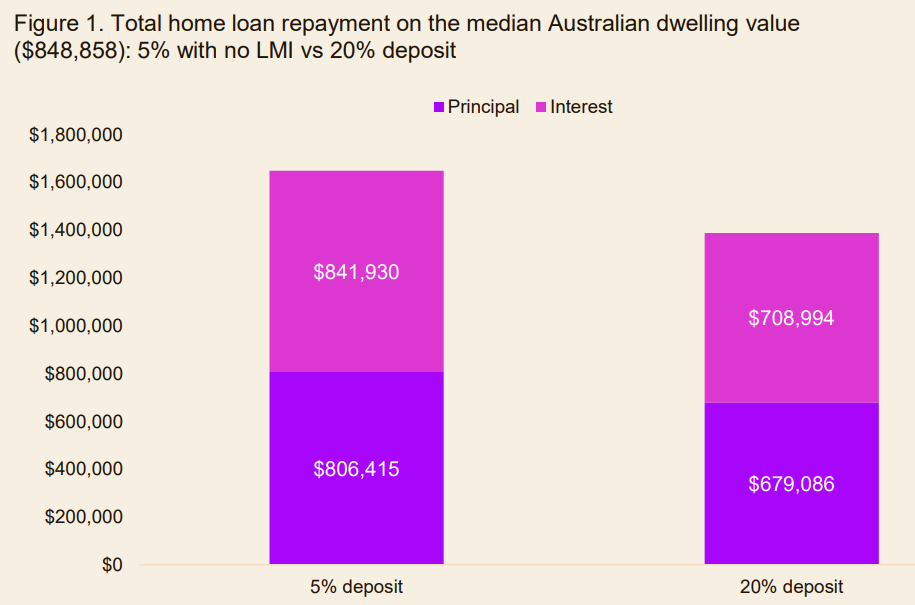

Eliza Owen, head of research at Cotality, has published the following chart on the amount of principal and interest repayments for the median Australian dwelling value ($848,858) under the Albanese government’s 5% deposit scheme for first-home buyers, which comes into effect on Wednesday.

Source: Cotality

Under Labor’s First Home Guarantee scheme, purchasers will be able to buy a home with only a 5% deposit without requiring lenders’ mortgage insurance, with the government (taxpayers) guaranteeing 15% of the mortgage.

As illustrated above, a purchaser who buys the median-priced home using the scheme would pay more than $130,000 in additional interest over the life of a 30-year loan, assuming an average mortgage rate of 5.5% per annum throughout the loan term.

However, Eliza Owen notes that buyers who enter the market earlier will also save on rent, which could offset the extra mortgage interest paid.

“Even though a smaller deposit means paying more interest over time, it could still work out cheaper for renters”, Owen wrote. “Getting into a home sooner may mean spending less time paying rent, and those savings can add up”.

“The biggest savings across the capital cities are estimated to be in Sydney, where a 5% deposit reduces time to save a deposit by an estimated six years, and $251,000 on rent at $801 per week”.

However, any benefits will likely be exhausted once the extra buyer demand from the scheme is capitalised into higher home prices.

“With expansion of the schemes’ places, price caps and incomes, there will almost certainly be a short-term boost to home values up to the threshold of the scheme, coinciding with interest rate falls and tight levels of housing supply”, Owen noted.

“While individuals on the scheme could leap over the deposit hurdle faster, this policy is ultimately a demand-side stimulus”.

Early users of the scheme will likely be okay, since they will ‘get in’ to the market before prices have risen.

However, fast forward a few years after prices have surged higher, and future first-home buyers will be entering a market that is significantly more expensive than it otherwise would have been. They will be purchasing with smaller deposits and carrying far larger mortgages than they would have otherwise.

Given such small deposits, these buyers will also face the prospect of falling into negative equity in the event of a significant decline in house prices.

Australia’s most similar economies—New Zealand and Canada—have both experienced house price declines of more than 15% from their most recent peaks.

Any similar decline for Australia could see thousands of first-home buyers facing negative equity, with mortgages that exceed the value of their homes.

It would also see Australian taxpayers, who have guaranteed 15% of first-home buyer mortgages, carrying billions of dollars’ worth of contingent liabilities.