I reported last week how New Zealand is facing an employment crisis.

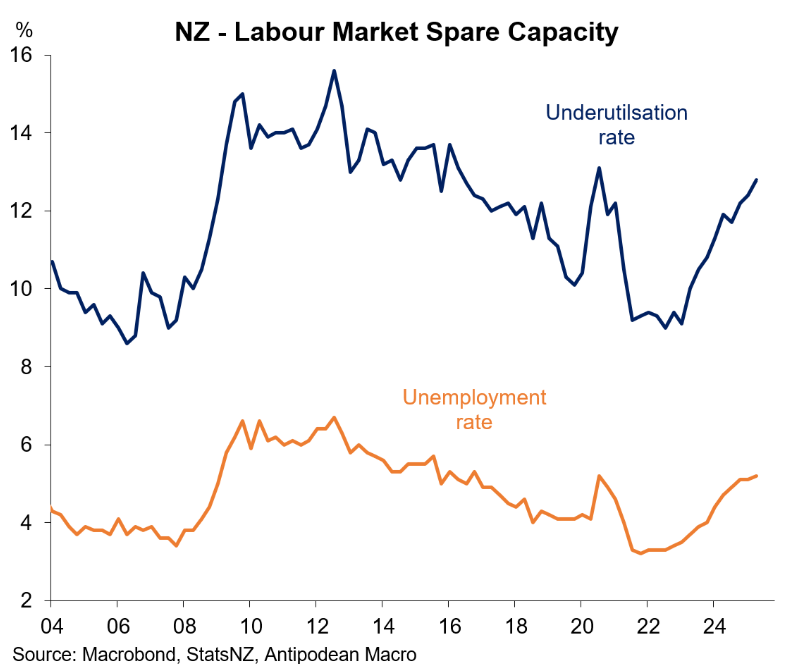

The official Q2 labour force survey from Stats NZ showed that New Zealand’s unemployment rate increased to 5.2% in the second quarter of 2025, up from 4.7% in Q2 2024. The underutilisation rate also rose by 3.5% over the year to 12.8%.

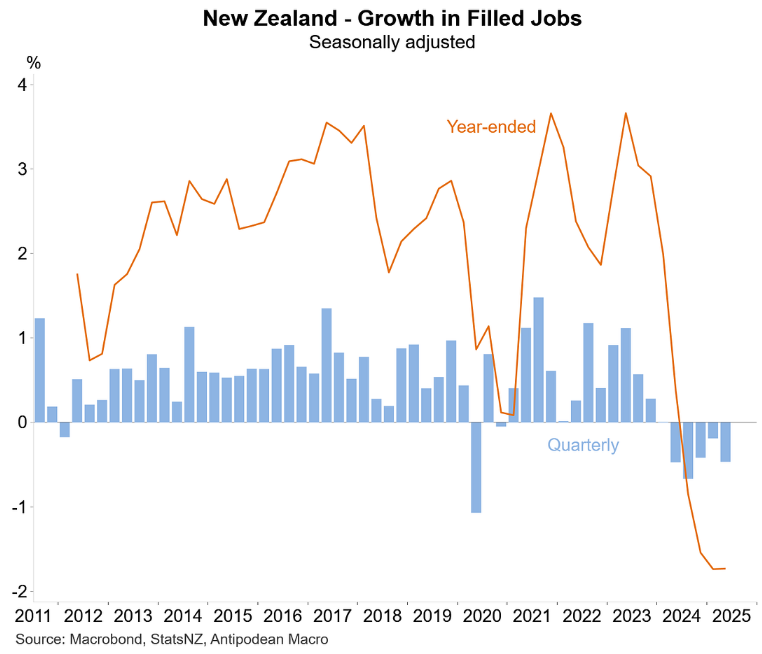

As illustrated below by Justin Fabo from Antipodean Macro, Stats NZ’s filled jobs data for Q2 2025 also fell by 0.5% over the quarter and by 1.7% year-on-year.

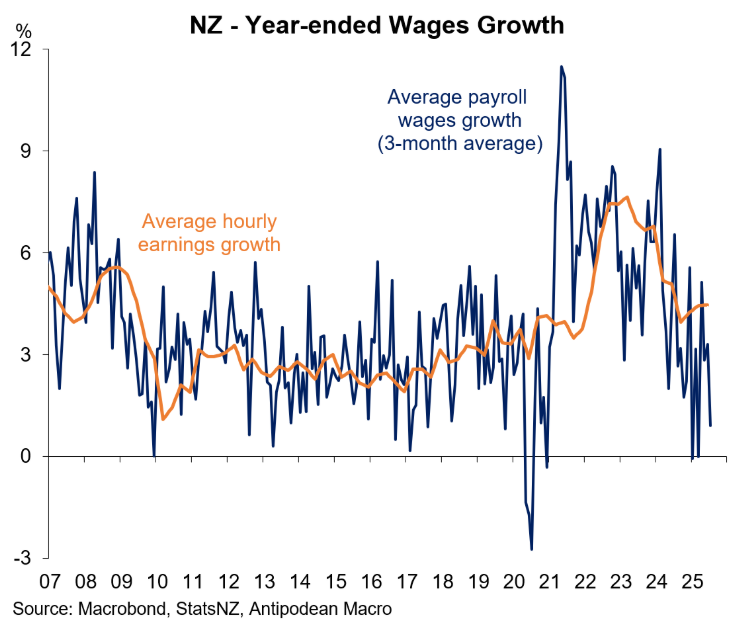

New Zealand wage growth has also collapsed as the supply of workers far outstrips demand from employers.

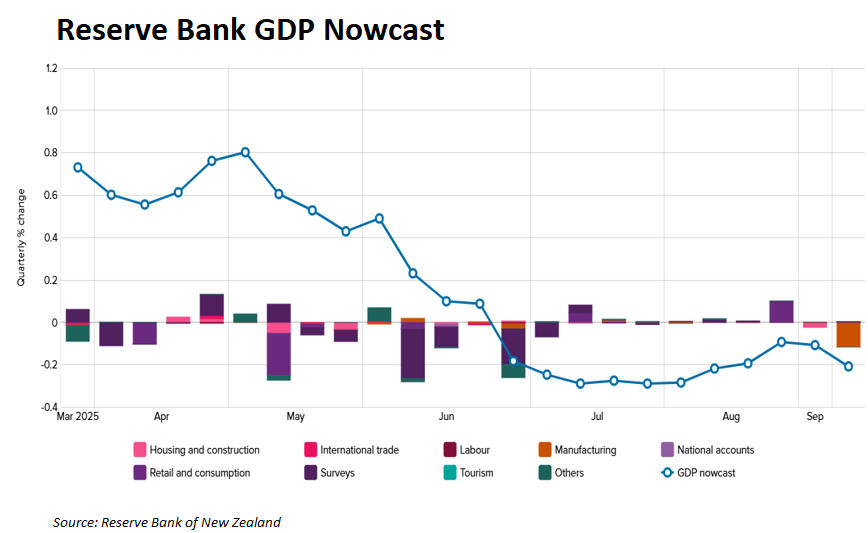

This week, Stats NZ will release the Q2 national accounts for New Zealand, which is expected to record a contraction in GDP.

The Reserve Bank’s latest Kiwi-GDP Nowcast, which is updated every Friday, forecasts that New Zealand’s GDP contracted by 0.4% in Q2 2025.

The Reserve Bank’s nowcast was revised lower following the final partial GDP indicators released last week, which showed the manufacturing sector in retreat in Q2 and negligible growth in a range of services industries.

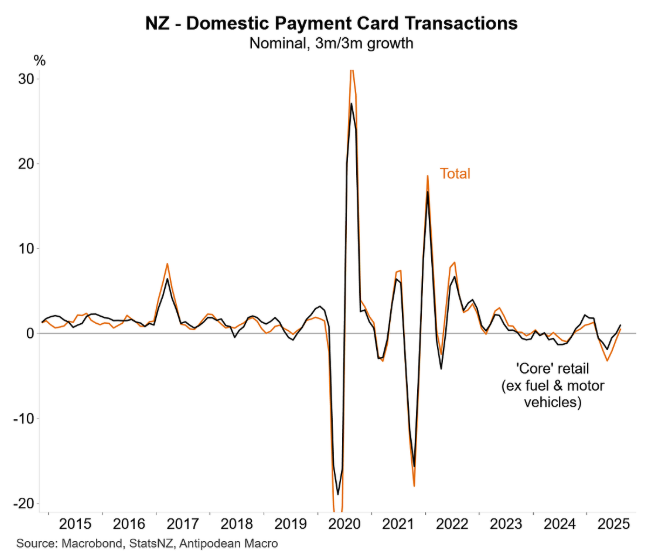

The good news is that the high-frequency data suggests that growth has returned in Q3.

The Performance of Manufacturing and Performance of Services indexes have improved recently and some discretionary spending types in the Stats NZ and bank card-spending data are showing signs of life.

That said, housing momentum has remained weak, with prices and dwelling construction continuing to fall.

As a result, New Zealand’s economy continues to operate with considerable spare capacity.

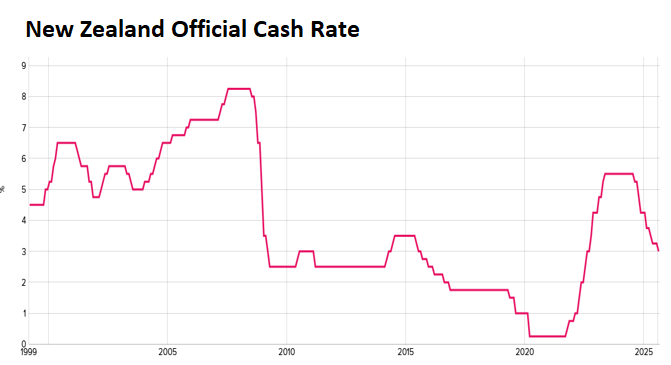

This is why the Reserve Bank signalled two further 25 bp rate cuts at the August MPS, which would lower the official cash rate to 2.50% from a peak of 5.5%.