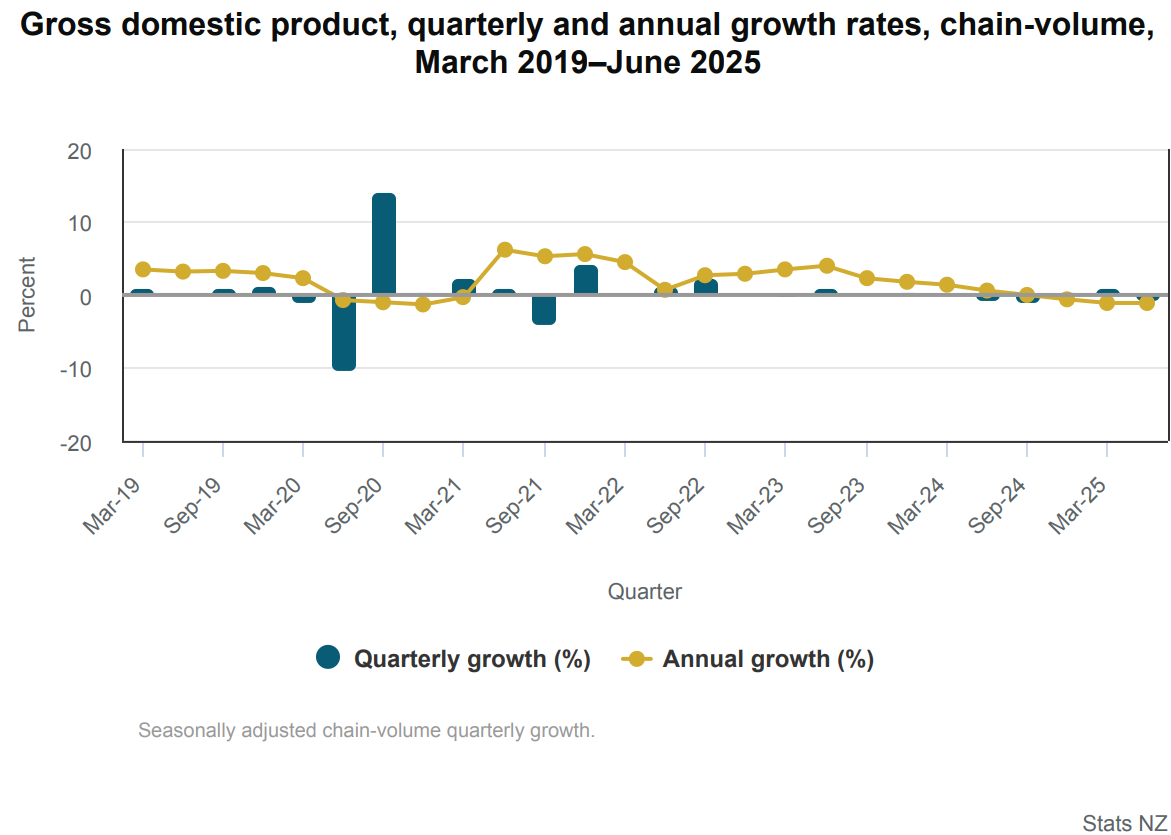

On Thursday, Stats NZ released the Q2 national accounts, which revealed a sharper-than-expected decline in real GDP.

New Zealand’s GDP declined 0.9% in the June 2025 quarter and was down 1.1% year over year. For the third consecutive quarter, annual GDP fell.

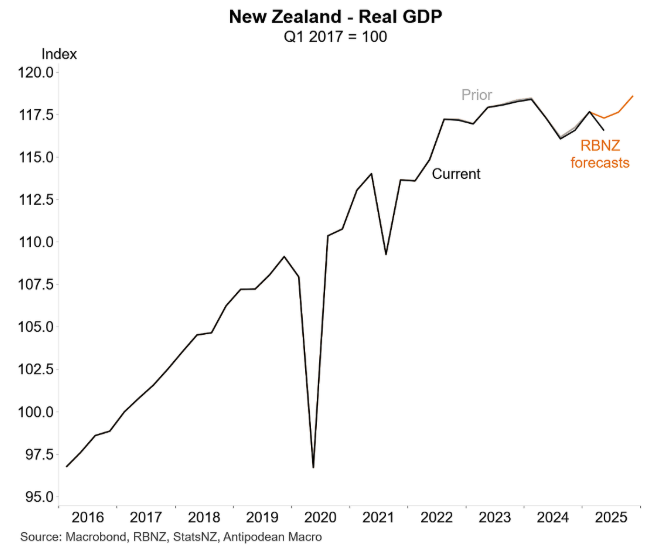

The following chart from Justin Fabo from Antipodean Macro shows that New Zealand’s GDP is tracking well below the Reserve Bank’s forecast from its latest Monetary Policy Statement:

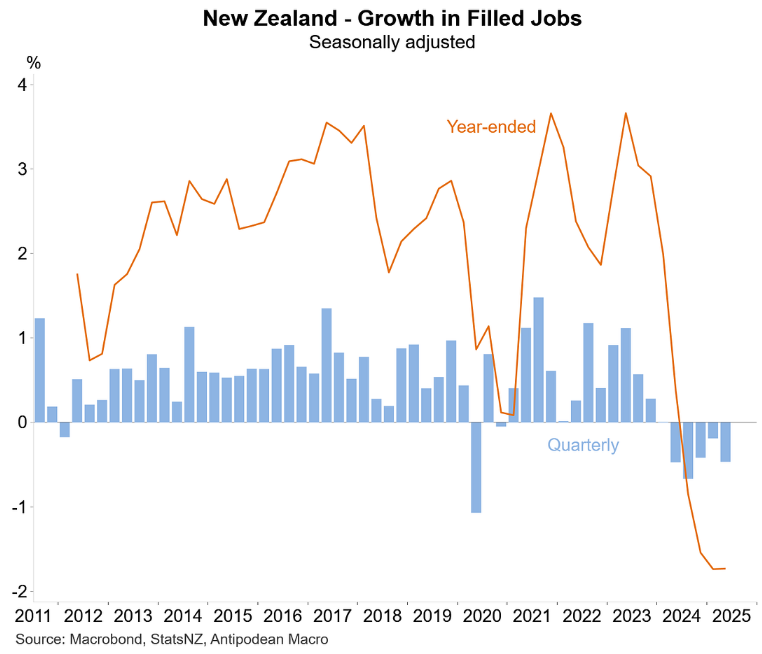

Stats NZ’s filled jobs data for Q2 2025 also posted a quarterly decline of 0.5% and a year-on-year decline of 1.7%:

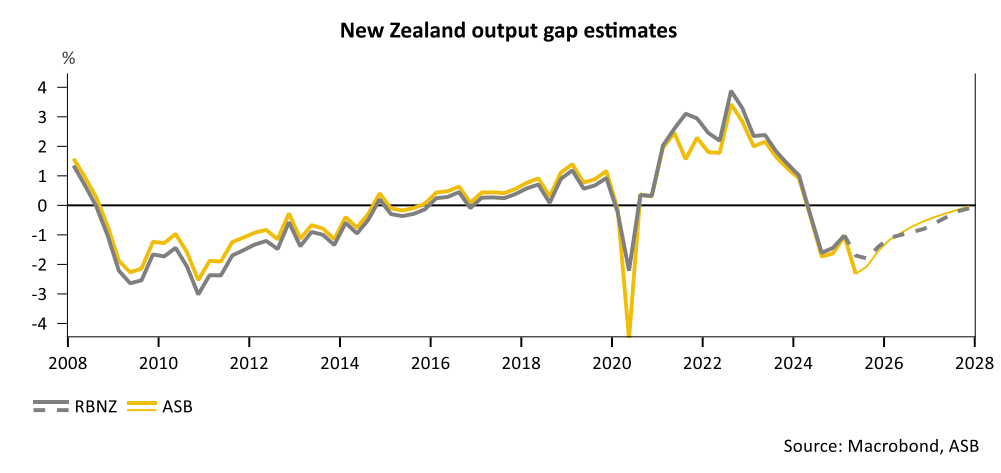

In its commentary following the Q2 national accounts release, major bank ASB stated that New Zealand’s “economic hole is big”, and with the nation “lacking any real economic tailwinds”, the Reserve Bank will need to slash the official cash rate:

“After disentangling the data, we have adjudged the amount of spare capacity in the economy to be significantly larger than the RBNZ assumed during the August MPS”.

“We deem this to be a larger deflationary impulse than previously assumed. With New Zealand lacking economic tailwinds, the onus falls on the OCR to support the economy”.

“The economy is in a deep hole and more supportive (i.e. lower) OCR settings will be needed to generate a period of above trend growth to narrow the negative output gap and to move the New Zealand unemployment rate lower to the 4 to 4.5% Goldilocks zone”.

“We are also more comfortable that pressures on medium-term inflation will continue to subside with the risk of core inflation falling below 2% in the absence of further OCR cuts”.

“We now expect a 50bp OCR cut in October, and a 25bp cut in November to bring about a 2.25% year-end OCR as the RBNZ moves to more actively support the economy”.

A 2.25% year-end OCR would represent an enormous 3.25% of easing since July 2024, when the OCR was 5.50%.