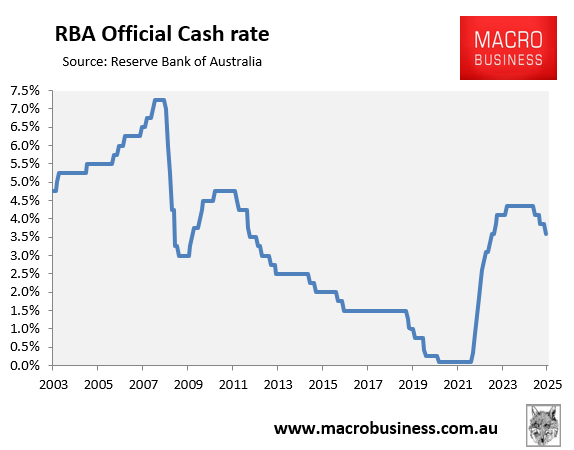

Last month, the Reserve Bank of Australia (RBA) lowered the official cash rate (OCR) by 0.25% to 3.60%. This marked the third 75 bp rate cut this year.

Most economists and financial markets have tipped the RBA to deliver another two 25 bp rate cuts by mid-2026.

The associated decline in mortgage rates has improved housing affordability, as measured by the proportion of income required to service a median-sized mortgage.

The Real Estate Institute of Australia’s (REIA) Housing Affordability Report for June 2025 shows that the proportion of the median family income required to meet average loan repayments fell to 47.7% in the June quarter. This represents an improvement of 0.3 percentage points over the quarter and 0.5

percentage points compared with a year ago.

“With another rate cut possible later this year and affordability now showing two consecutive quarters of improvement, the outlook for buyers is brighter than it has been in some time”, REIA President Leanne Pilkington said.

However, any relief is likely to be short-lived.

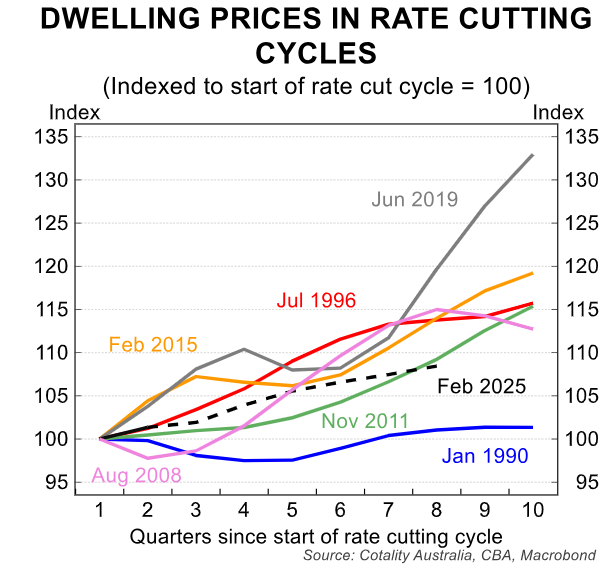

The following chart from CBA shows that dwelling prices typically rise by double-digit rates two years after the commencement of an interest rate-cutting cycle.

The rate cuts will also be accompanied by stimulatory policies from governments, including the Albanese government’s 5% deposit scheme for first home buyers, which comes into effect on 1 October 2025, as well as the expansion of federal and state government shared-equity programs.

The combination of these policies and rate cuts will inevitably drive up homebuyer demand and prices.

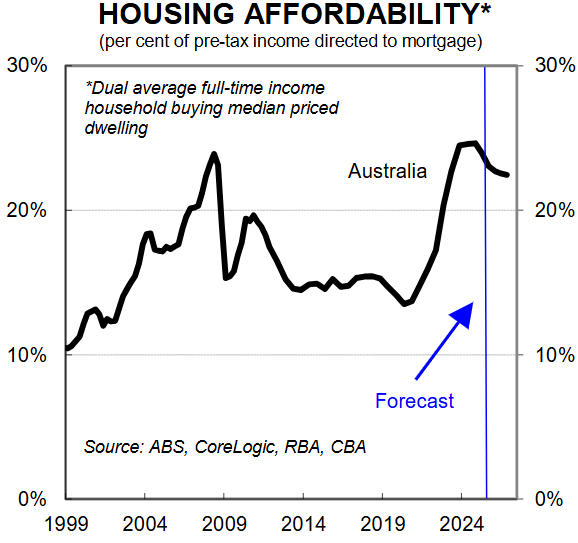

The following CBA housing affordability chart highlights the conundrum facing first home buyers in Australia.

Despite projecting further interest rate reductions and a relatively modest national dwelling value increase of 6% in 2025 and 4% in 2026, the CBA projects that Australian households will spend a historically high proportion of their incomes on mortgage payments for the median-priced property.

This result underscores the unavoidable truth in Australia: lower mortgage rates and other demand-side policies tend to translate into larger mortgages and higher housing values.

Increasing purchasing power, whether through reduced interest rates, shared equity schemes, or other first home buyer programs, does not improve structural housing affordability.

To make housing more affordable, prices must fall in relation to income.