New Zealand’s economy and housing market remain in a funk.

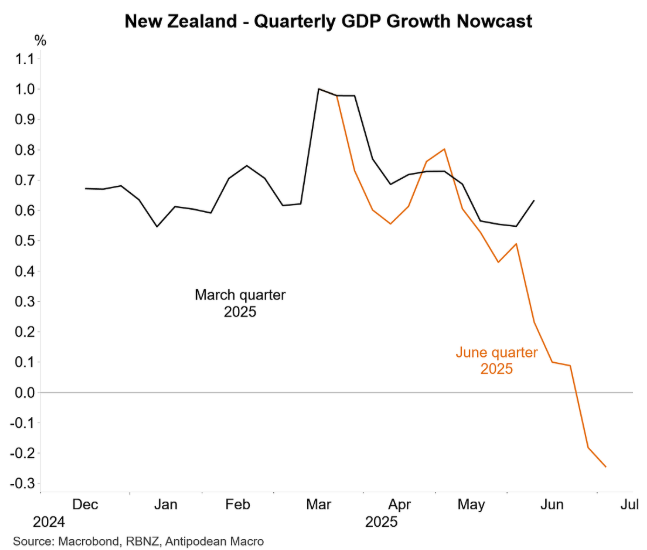

As illustrated below by Justin Fabo from Antipodean Macro, the Reserve Bank of New Zealand’s Kiwi-GDP nowcasting model suggests that the nation’s GDP may have declined in Q2 2025 by 0.3%.

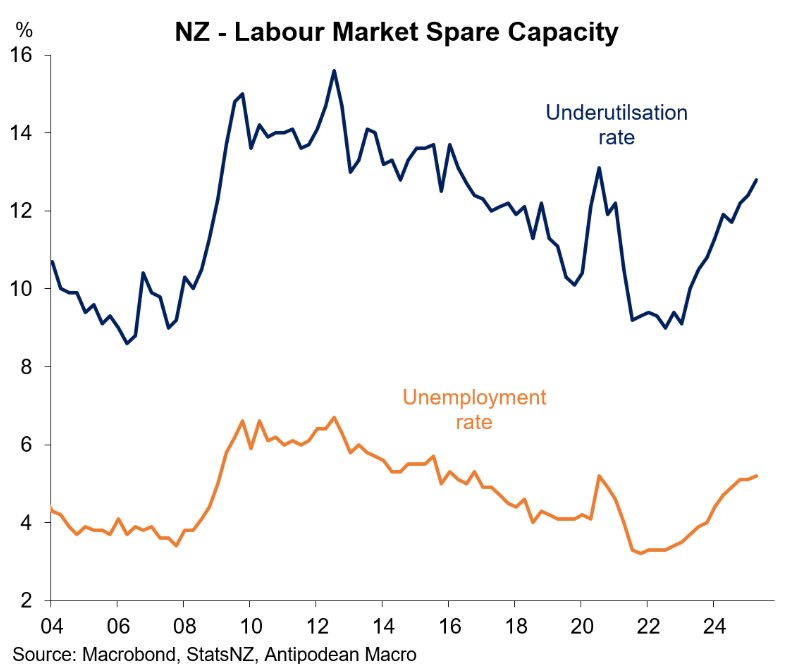

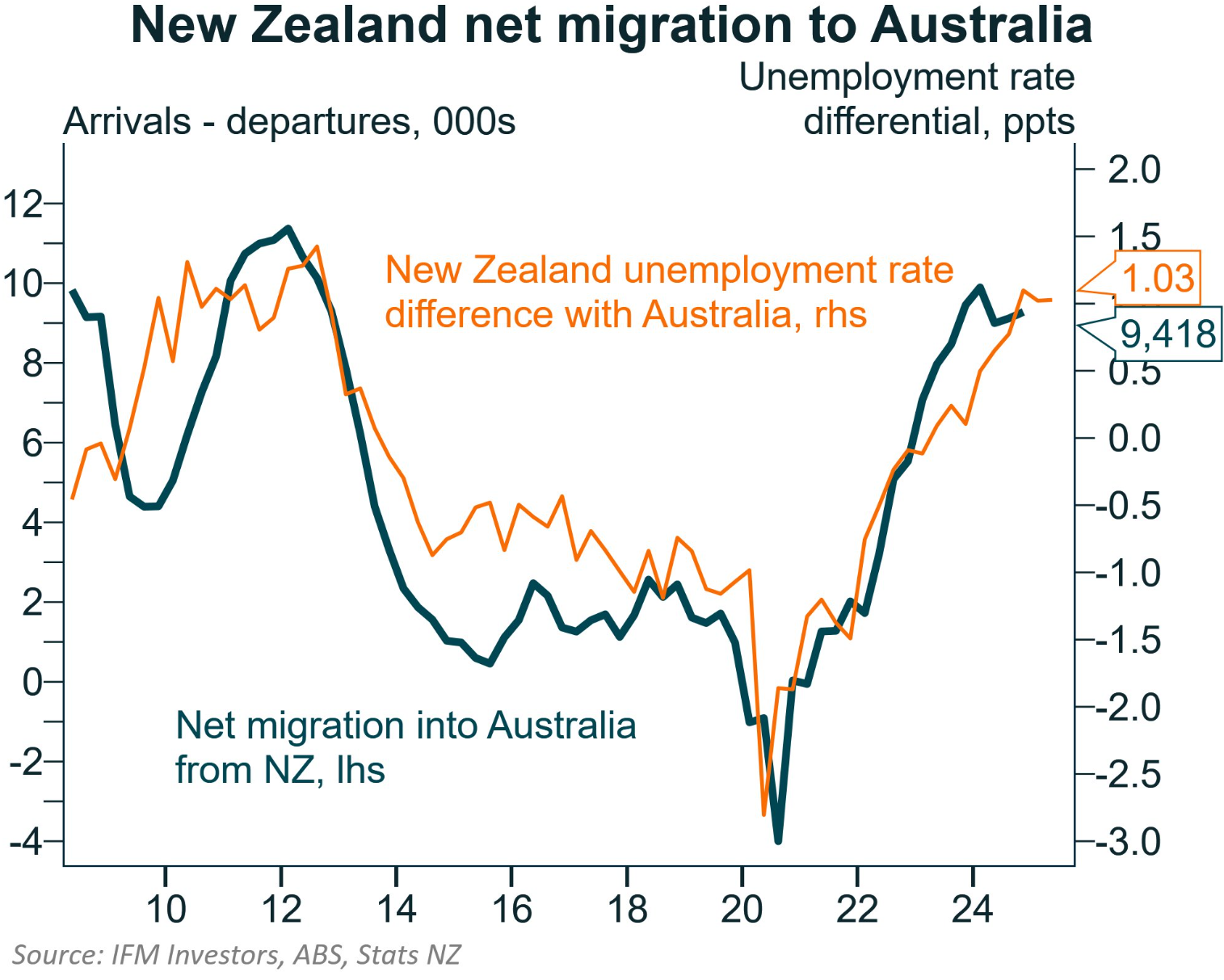

New Zealand’s labour market is also suffering its weakest conditions in a decade outside of the pandemic.

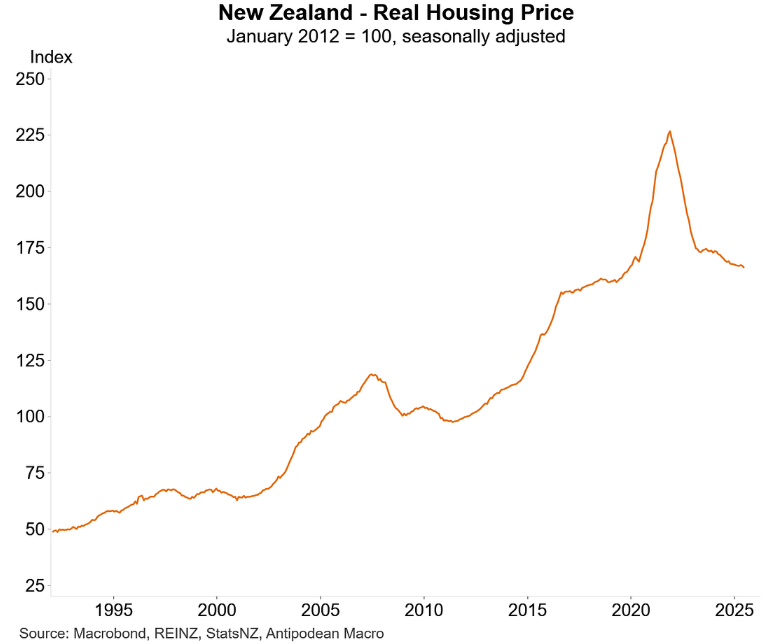

Part of the reason why New Zealand’s economy is so weak is because it isn’t getting the usual stimulus from rising home prices and the ‘wealth effect’, which is keeping consumer spending in check.

New Zealand home values have crashed back to 2019 levels in real inflation-adjusted terms.

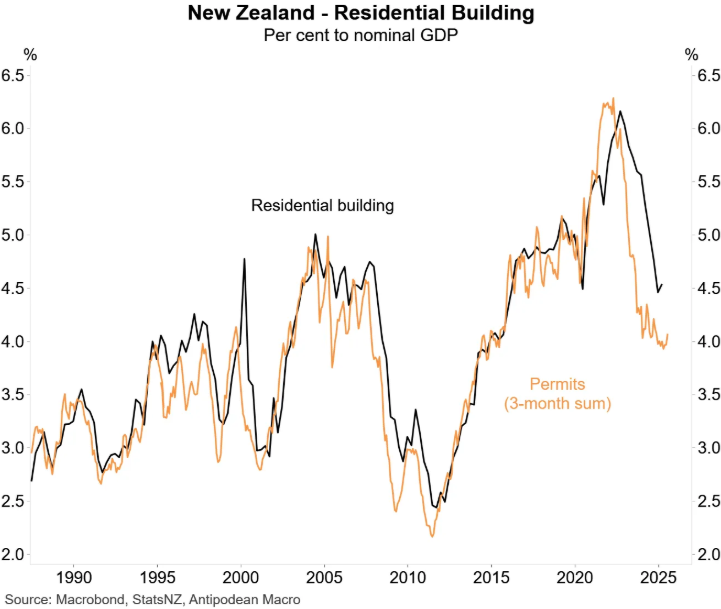

Residential building permits and construction rates have also fallen sharply, dragging on growth.

Meanwhile, the sharp rise in unemployment has seen net overseas migration to New Zealand fall to a 2½-year low and is tracking around half the historical average, with lots of residents emigrating to Australia.

In 2018, the former Labour government of New Zealand imposed a foreign buyer ban, preventing non-residents from purchasing existing residences, with exceptions for Australian and Singaporean residents.

The National Party promised that it would lift the foreign buyer ban if elected.

Leader Chris Luxon pledged that National would enable foreigners to buy homes worth more than NZ $2 million as long as they paid a 15% purchase tax.

When National won the election in October 2023 and Luxon became Prime Minister, discussion of a repeal faded. As part of a coalition government agreement with New Zealand First, Winston Peters, New Zealand’s deputy prime minister, allegedly persuaded National to abandon the repeal effort.

However, as reported by Bernard Hickey on Tuesday at The Kākā, the National government has “completed phase one to fire up house prices”:

The Government yesterday completed phase one of its operation to revive house price inflation before the election, opening up the top end of the market to foreign buyers. Agents said it would fire up activity in Auckland and Queenstown as the spring open home season begins.

The Government has already overseen the Reserve Bank’s review of its capital upgrade engineered by Adrian Orr before he departed mysteriously. That review has watered down Orr’s higher capital requirements for banks, freeing them up to pump more credit into the market.

The RBNZ will soon have a new Governor and new Chair appointed simulataneously by Finance Minister Nicola Willis and PM Christopher Luxon, both of whom have ignored the previous political consensus about not expressing views on what the RBNZ should do.

These moves add to a stalling of housing supply growth after the Government stopped Kāinga Ora’s programme to build over 3,700 new houses, reversed RMA and Three Waters reforms and froze capital grants for new infrastructure needed for new housing.

The next phase will depend on whether it can cajole a Reserve Bank with a new Governor and new Chair to relax LVR and DTI controls soon enough to get prices rising in a sprightly fashion through early and mid-2026 in time for a re-election.

The national government also aims to increase immigration using three visa pathways.

First, the government introduced the new ‘Parent Boost’ visa, which allows migrants to bring their parents to New Zealand for up to ten years.

The government introduced a new foreign investor visa to attract wealthy individuals and boost economic growth.

The government has loosened visa regulations, reducing the minimum required cash for the category that focuses on higher-risk investments to NZ$5 million (US$3 million) from NZ$15 million and eliminating the English language barrier.

New Zealand has already seen a surge in applications for the new visas from the United States, mainland China, and Hong Kong, many of whom intend to acquire property.

Third, in an effort to increase enrolments, the government increased the number of hours permissible for international students to work during the academic semester from 20 to 25 hours per week.

In a Press conference last month, New Zealand Housing Minister Chris Bishop argued that his country needs to decouple economic growth from house prices, no matter how difficult it would be in the short term.

Bishop argued that the Kiwi economic recovery should be driven by broad-based productivity growth rather than by growing house prices.

“We’ve got to decouple the idea that the economy is linked to house price growth. It’s not.”

“Destroying the idea that the New Zealand economy should just be based on house price growth is a fundamental formula this government is trying to embed into the New Zealand psyche and also into the arteries of the economy. It will take some time but I’m pleased with the process we’re making,” Bishop said.

Bishop went on to share his frustration that so much media and public attention is focused on the notion that home prices need to rise.

Bishop’s sage comments are at odds with the government’s actions on foreign buyers and migration.

The government seems intent on reigniting New Zealand’s housing market.