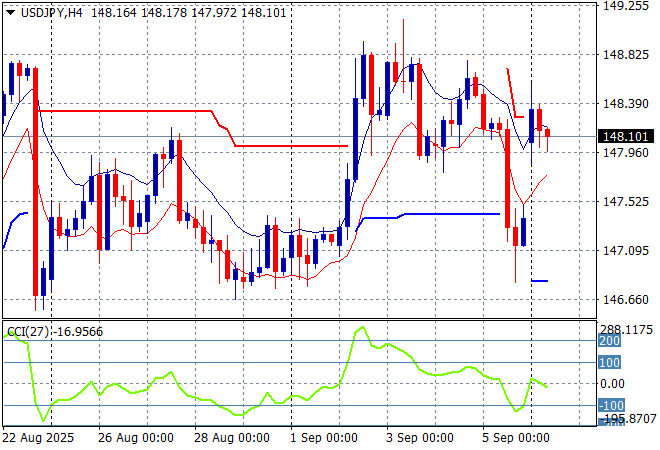

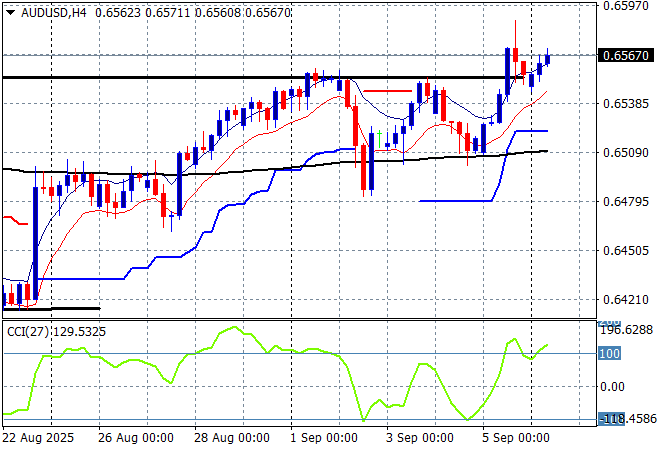

Asian share markets are mostly higher across the board as traders anticipate more Fed easing after Friday night’s US jobs print showed the Trump regime’s economic malaise continues although local stocks had a little stumble. Meanwhile bond markets are trying to recover with many long dated yields across the UK, Japan and USA backing off from their recent new highs as the USD is pushed lower against almost everything but Yen as the resignation of PM Ishiba over the weekend causes Yen to gap lower. The Australian dollar has lifted further above the 65 cent level as the interest rate differential looks set to widen.

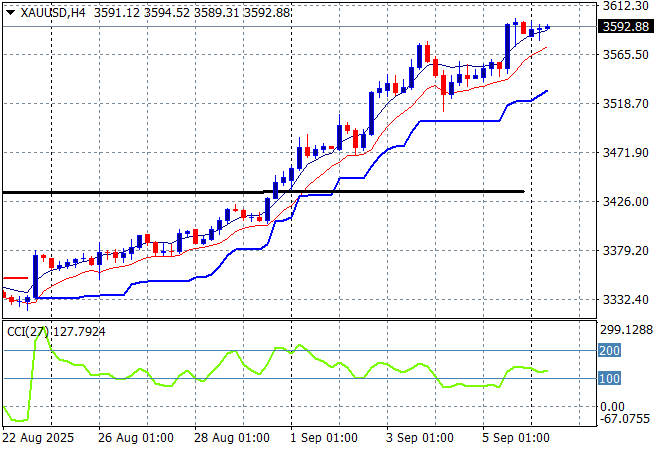

Oil markets are failing to get out of their recent depressed mood with Brent crude keeping well below the $67USD per barrel level while gold had a little further lift higher over the weekend gap as it closes in on the $3600USD per ounce level:

Mainland Chinese share markets are lifting going into the close with the Shanghai Composite up more than 0.4% to extend further above the 3800 point level while the Hang Seng Index is up 0.7% to close at 25640 points. Japanese stock markets are also doing well with the Nikkei 225 closing nearly 1.4% higher at 43626 points with the USDPY pair gapping over the weekend on the IShiba resignation, starting above and staying at just above the 148 level:

Australian stocks were the odd ones out and sold off slightly with the ASX200 closing 0.2% lower to 8849 points while the Australian dollar has again lifted to a new high above the mid 65 handle against USD:

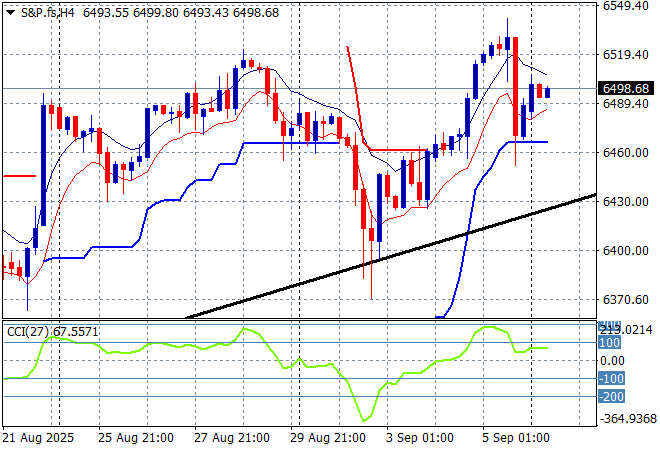

S&P and Eurostoxx futures are rising going into the London session with the S&P500 four hourly chart showing the market wanting to crack through the 6500 point level with momentum wanting to return to overbought levels as traders have already dialed in the certainty of yet another put from the Fed:

The economic calendar slows down after Friday’s NFP print with German industrial production the only event of note tonight.