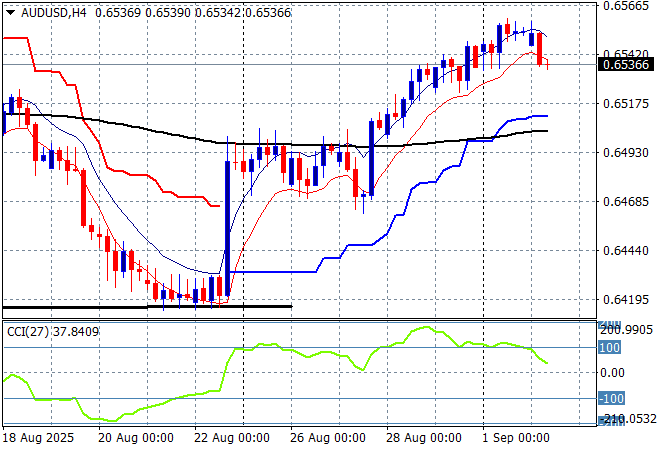

Asian share markets are seeing mixed results as traders await the return of US markets from their long weekend with the latest news about a US/Japan trade deal sending Yen lower without any real action. The chance of more rate cuts from both the BOJ and ECB firmed with the ratings agencies today but that is not stopping USD lifting slightly after being against a wall of selling against the majors as the Trump regime seems hell bent on removing opposition in the Federal Reserve. The Australian dollar has pulled back slightly but still remains above the 65 cent level.

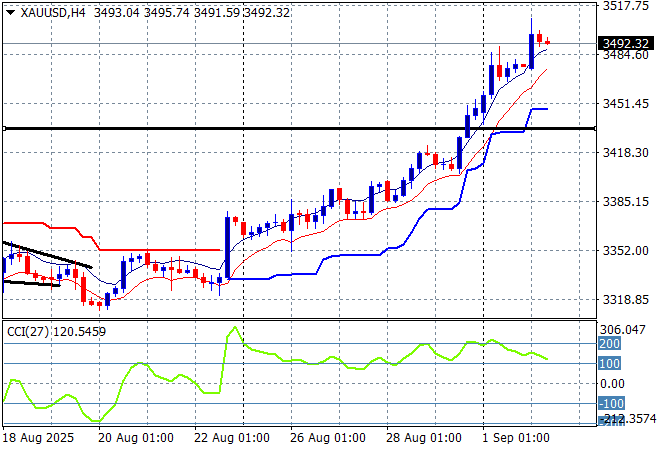

Oil markets are trying harder to get out of their recent depressed mood with Brent crude pushing through the $68USD per barrel level while gold has decisively broken out above the $3400USD per ounce level to make a new record high close to the $3500 level:

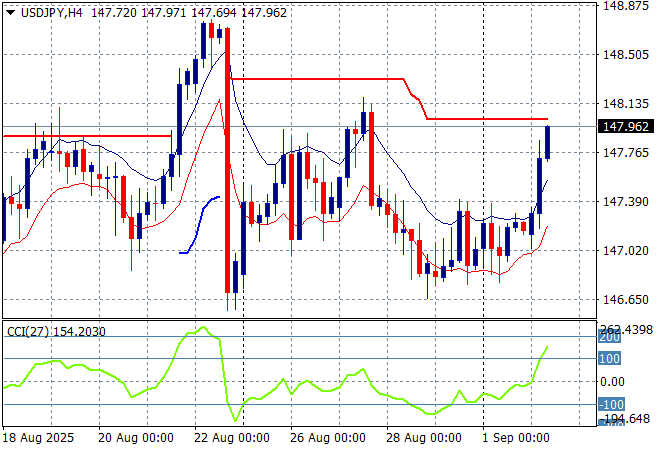

Mainland Chinese share markets are pulling back sharply going into the close with the Shanghai Composite down more than 0.6% while the Hang Seng Index is down just 0.2% to remain above the 25000 point level. Japanese stock markets are up slightly on the weaker Yen with the Nikkei 225 closing 0.2% higher at 42310 points with the USDPY pair launching back up to the 148 level for a near two week high:

Australian stocks sold off again with the ASX200 closing 0.3% lower to 8893 points while the Australian dollar has slid back slightly after stalling out above previous resistance at the 65 handle to give back some of its new weekly high:

S&P futures are suggesting a flat start after the long weekend while Eurostoxx futures are down slightly going into the London session with the S&P500 four hourly chart showing the market unable to stay above the 6500 point level with momentum now retracing back to slightly negative levels as it fails to exceed the early August highs:

The economic calendar includes the latest European flash CPI print but the real interesting one tonight will be the US ISM measure, with manufacturing employment the one to watch.