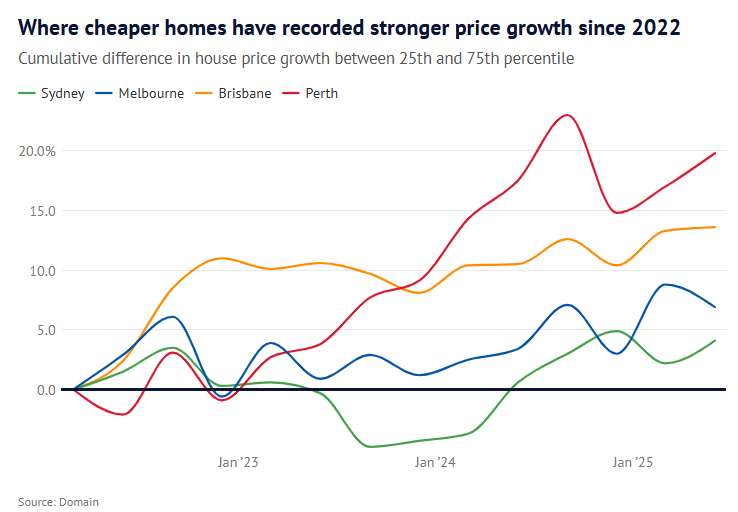

According to Domain, Australian home values are soaring at the lower end of the market, putting immense strain on affordability for first home buyers.

Domain data shows that property prices in the bottom quarter of the market have increased faster than the top quarter during the last three years in most capital cities.

“What it demonstrates is there is a dwindling pocket of affordability”, Domain chief of research and economics, Dr Nicola Powell said. “More people are competing for those affordable homes because there is a lack of them”.

“What it shows is really that affordability is at a breaking point. It takes a significant time to save a deposit, but it also takes a significant amount of money to pay the repayments”.

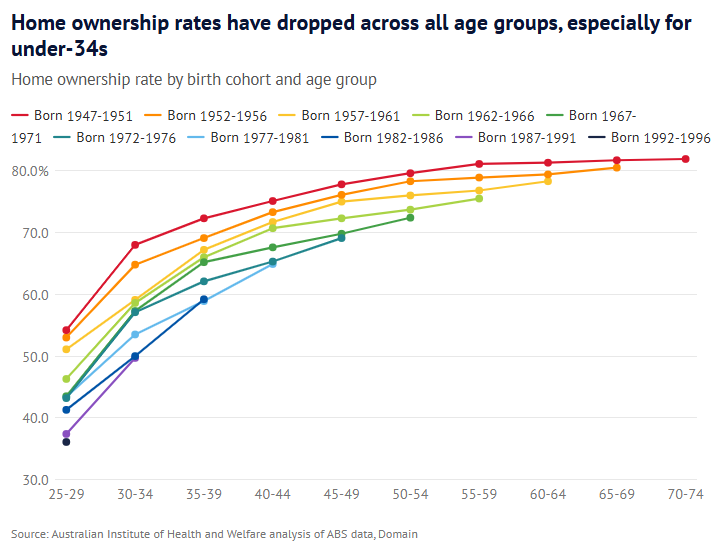

“There is the generational divide that has occurred. Home ownership under 34 has fallen dramatically. Those who were born in the late ’80s are much less likely to own a home when compared to those in the post-war era”, she said.

The situation will worsen for first home buyers after the Albanese government’s 5% deposit scheme comes into effect next month.

Under the First Home Guarantee scheme, almost every first home buyer will be able to purchase a home with a 5% deposit without needing lenders’ mortgage insurance, with the government (taxpayers) guaranteeing 15% of all mortgages.

While this policy will help to bridge the deposit gap, it will also lift borrowing capacity and buyer demand, driving up values, especially at the lower end of the market.

The end result will be that future first home buyers will be required to take out larger mortgages in order to purchase homes that are significantly more expensive than they would have been without the First Home Guarantee policy.

Every time that governments have implemented policies aimed at making it easier to purchase housing, it has been capitalised into higher home prices requiring larger mortgages.

Labor’s First Home Guarantee scheme is a case of history repeating.