Yet another major bank is on board. Credit Agricole.

After years of resistance, the RBA has lowered its productivity growth assumption. This has not led to higher inflation forecasts or the risk of tighter monetary policy.

The RBA is assuming lower productivity growth will not only weaken supply but also demand via lower income growth.

◼The Australian government hosted a productivity roundtable to find ways to boost productivity growth and flagging living standards. The common theme to come out of the roundtable was the intergenerational unfairness of thetax system that taxes the working age population too heavily while lightly taxing wealthy retirees.

◼While the right noises were made by the roundtable, the Australian Labor Party government has not committed to tax reform until the next election in 2028. There is a risk it uses the sentiment from the roundtable to justify hiking taxes on the wealthy to fund its high spending rather than cut corporate and income taxes to encourage work and investment and boost productivity.

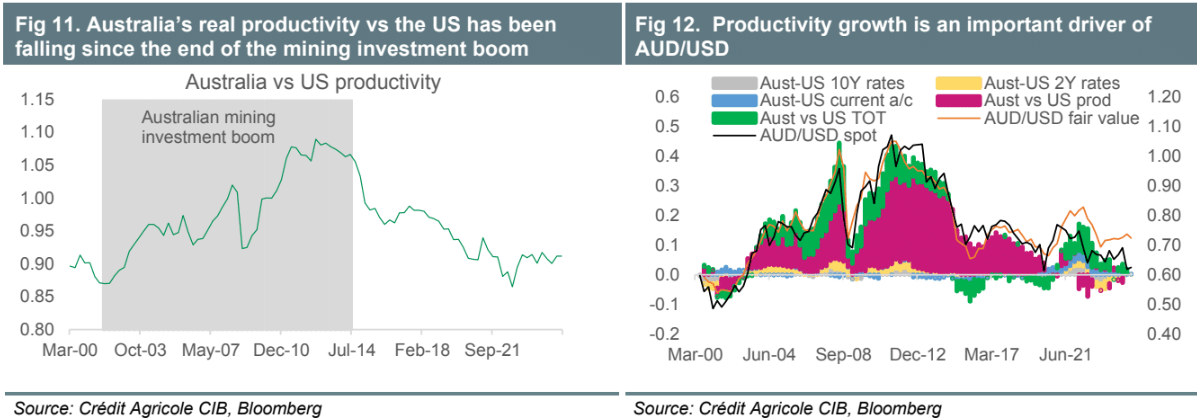

◼Productivity is an important factor for AUD/USD. Along with the terms of trade, ithas been the strongest driver of the exchange rate for the past quarter of a century. While strong productivity growth during the mining investment boom helped push AUD/USD above parity, its slump since is weighing heavily on the exchange rate.

◼Australia’s weak productivity growth is a key reason we forecast AUD/USD’s rally being limited to 0.68 by end-2025 and reaching 0.70 by H2 26. Supporting this rally is the risk that the RBA’s new way of looking at the inflation-productivity dynamic is too optimistic and thereby constrains its rate cuts.

Meh. 2026 heralds crashing Terms of Trade and rampant immigration. This is precisely the recipe of the post 2015-lowflation period in Australia.

The RBA has finally joined reality. The mass immigration economic model doesn’t do productivity, income gains or inflation.

This is why I agree that the AUD rises to 0.68 cents and then starts to fall again in 2026.

If you want a rat wheel economy, you will get a rat wheel currency.