The fix is in for Australian gas. The deeply corrupt Albanese government is undertaking a review of gas policies with both hands tied behind its back, having already ruled out the only policy that makes sense: retrospective reservation for QLD gas exporters.

What we are seeing instead, again, is performative democracy in which everyone pretends to debate an issue while they all know the outcome beforehand.

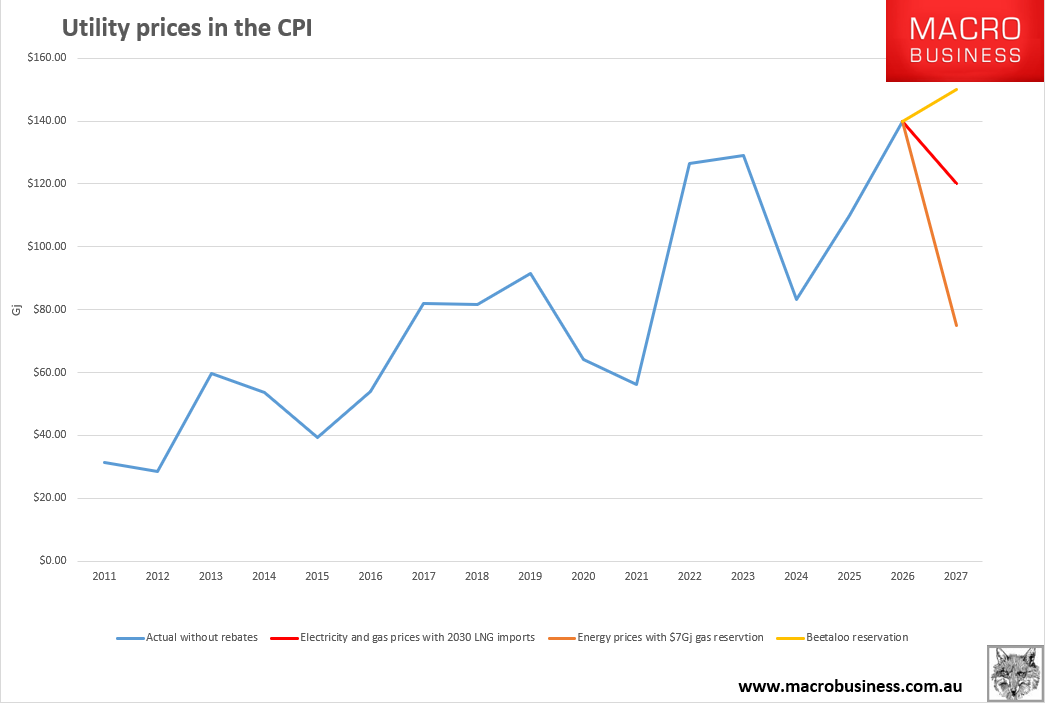

That outcome will be to unleash Beetaloo Basin gas in return for a prospective domestic reservation that is perfectly useless.

It is useless because it won’t drop prices at all.

To prevent the gas cartel from gouging us ongoing, we will need new competition to apply price discipline.

Without using policy to curtail cartel influence, that can only come from offshore, via imported LNG.

Yes, that’s right. Assuming the deeply corrupt Albanese government is doing what I think it is with the Beetaloo, only foreign gas will stop the price gouge.

Notably so, after Putin and Xi rode to our rescue. Goldman.

The news yesterday that the Power of Siberia 2 pipeline is going ahead is big in these terms.

While we’re still awaiting details around the Russia-China memorandum of understanding announced today (September 2nd) to build the Power of Siberia 2 (PoS2) pipeline, this announced project has the potential to exacerbate and extend the significant bearish cycle we already expect for global LNG markets towards the end of this decade.

If built, PoS2 would move 50 Bcm/y (36 mtpa, nearly the same capacity as the Nord Stream pipeline) of natural gas from the Russian Yamal region to China.

This can work as an outlet for Russian gas that has been stranded since the curtailment of Russian exports to Europe, which started in the fall of 2021.

The pipeline’s large capacity has the potential to significantly crowd out China LNG imports.

To be clear, combined with the 8 Bcm/y1of additional exports announced today, the total incremental Russian gas supply to China would be the equivalent of 10% of today’s existing global LNG supply or 37% of the US total LNG export volumes we estimate for this year.

These sizable volumes would likely hit the market around what we see as the peak oversupply period of the upcoming bearish cycle for global gas markets, towards the end of this decade.

More specifically, while the timeline for PoS2 is uncertain, the fact that it could create an outlet for Russian stranded gas can work as an incentive for a faster build than the five years it took to build the 38Bcm/y Power of Siberia 1 pipeline to China 2.

If realized, this would lead to significantly higher global gas supply likely towards the end of this decade, exacerbating the risk of downside pressure to global gas prices, and potentially resulting in the cancellation of US LNG exports.

We continue to see an opportunity for LNG sellers to hedge the back of the TTF or JKM curves, which we believe have not fully priced these risks.

Of course, what Australia should do with this news is immediately apply Peter Dutton’s retrospective reservation to QLD gas exports.

The world is no longer going to need those volumes, so the price is going to crash just as Aussie export contracts roll off.

This policy would immediately lower the local gas price to whatever price we like. $7Gj looks good to me.

In lieu of this eminent sense, and given that the fix is already in to produce Beetaloo volumes, we need an LNG import terminal!

The glutted global gas markets of 2015-2018 averaged Asian gas prices around $6Gj, with prices sinking as low as $4Gj. It will be similar later this decade, so it can land gas in Australia at $9-11Gj.

This is still eminently stupid versus keeping our own cheap gas. But it’s better than allowing the gas cartel to charge us $15Gj for Beetaloo gas, as gasless Asian nations pay $9GJ for US volumes.

Build the LNG import terminals!