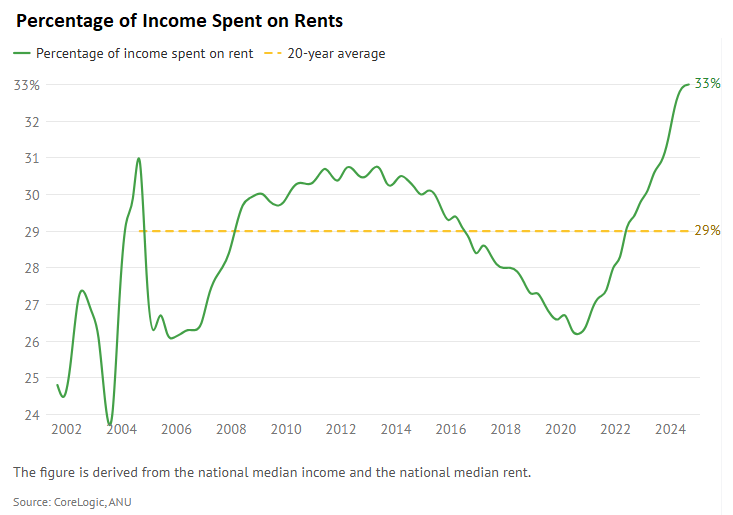

According to Cotality (formerly CoreLogic), Australian rental affordability was at a record low at the end of 2024, with the median household required to spend 33% of their income to rent the median home.

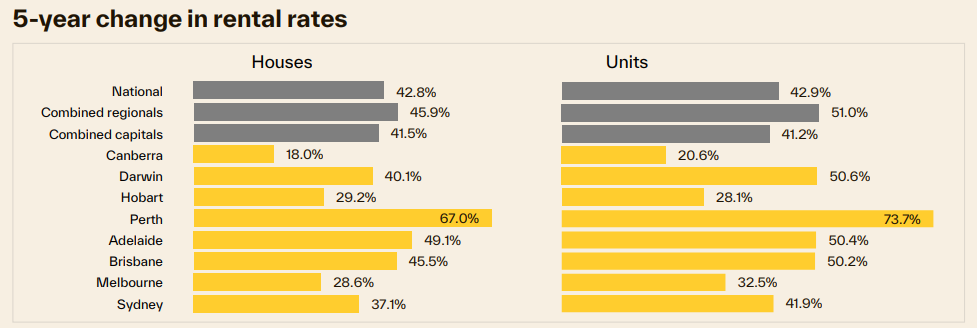

Cotality’s latest Quarterly Rental Review, released in July, showed that rents nationally have surged by 43% over the past five years:

Source: Cotality

As a result, the national median weekly rent has risen by nearly $200 to $665 per week, adding $10,350 per year to the median rent.

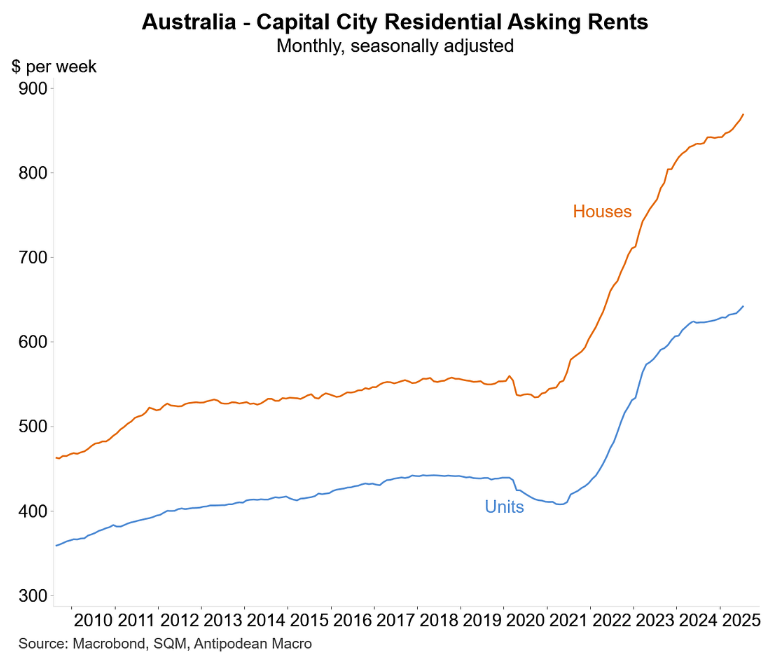

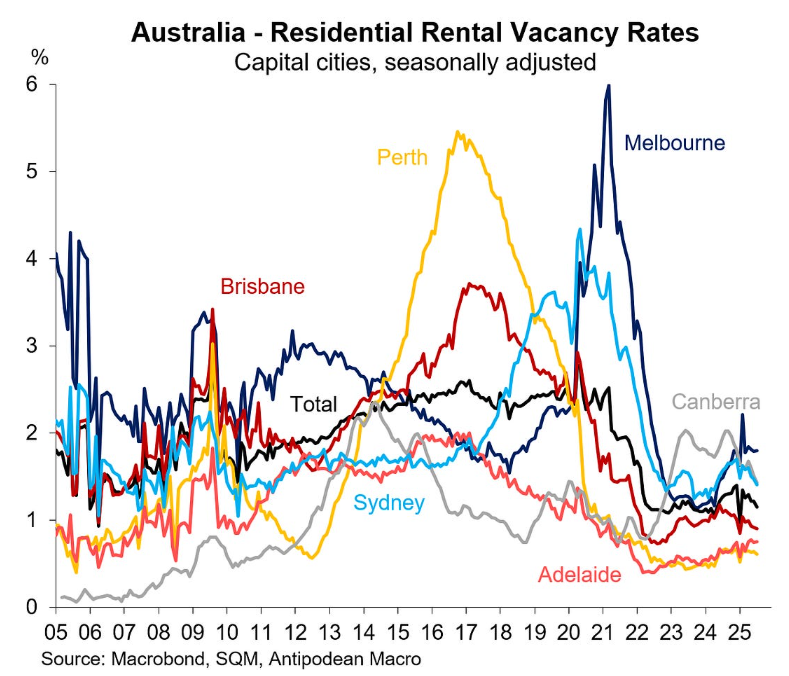

The following chart of SQM Research’s rental asking prices, presented below by Justin Fabo from Antipodean Macro, paints a dire picture for Australian tenants:

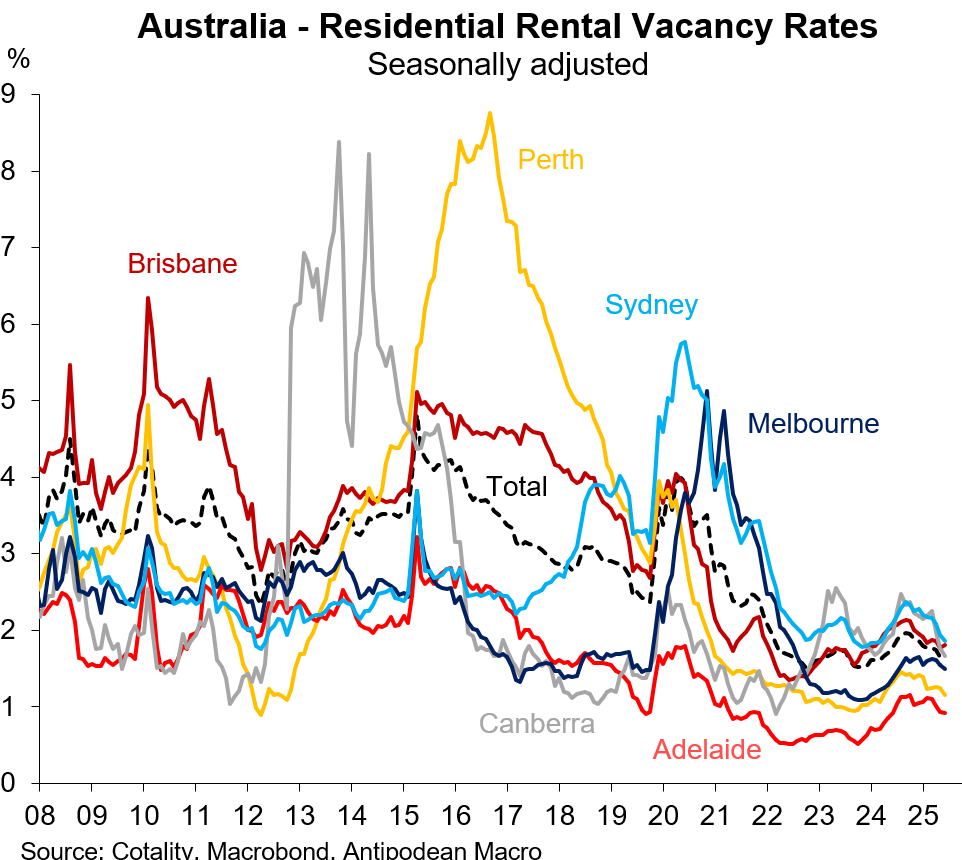

After showing improvements last year amid moderate immigration, Australia’s rental vacancy rates have tightened.

This tightening of rental vacancy rates is illustrated below using Cotality data:

As well as SQM Research data:

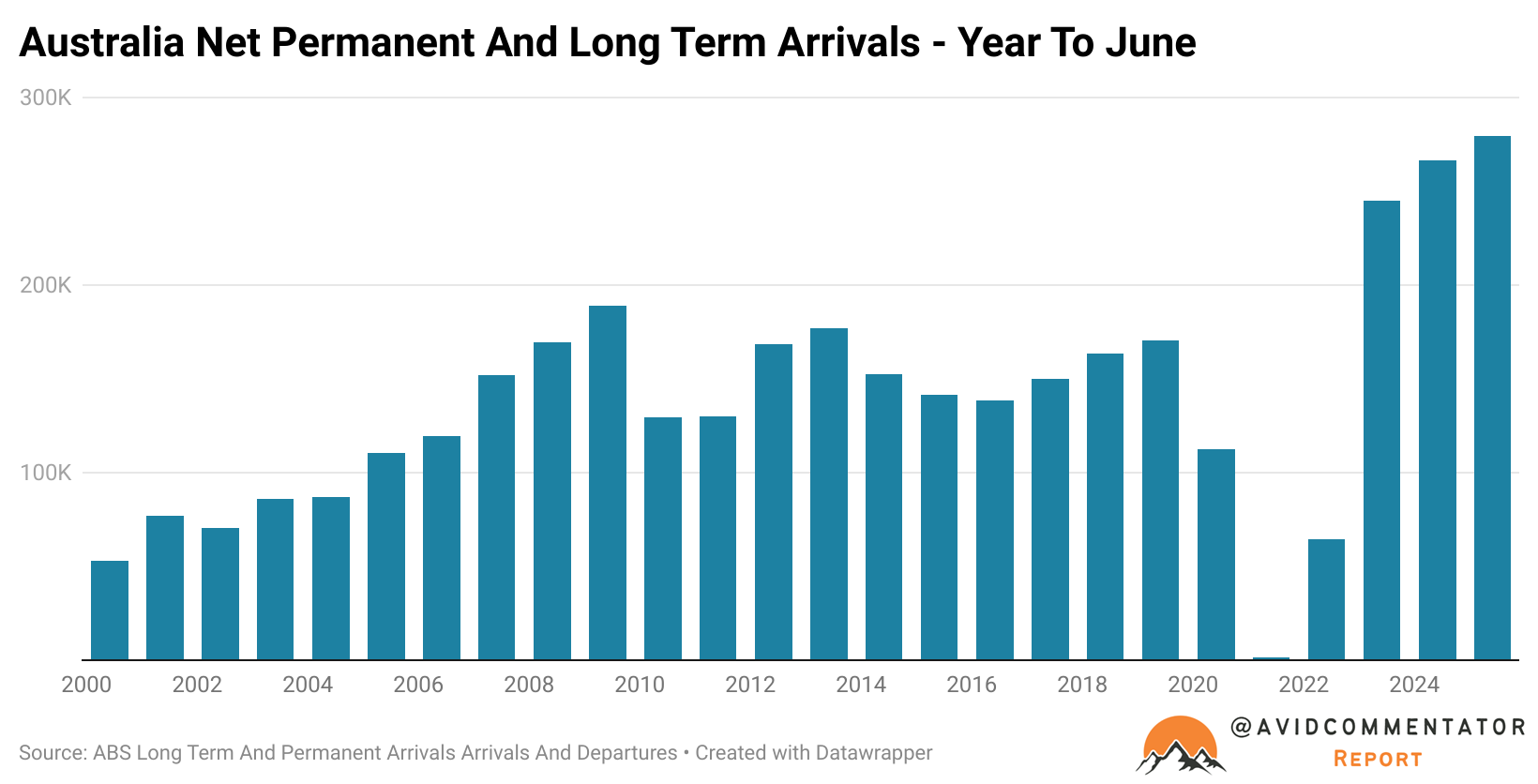

My guess is that the record surge in net permanent and long-term arrivals over the first half of 2025 has tightened the rental market as population demand has overrun rental supply:

Cotality has released its August housing market results, which report that “national rental growth picked up to 0.5% in seasonally adjusted terms through August, the largest month-on-month rise since May last year”.

“The re-acceleration in rental growth has been apparent through most of 2025, with the annual change now rising over two consecutive months, reaching 4.1% in August”.

Source: Cotality

“Rental markets remain extremely tight across most regions, with the national vacancy rate at 1.5% in August which is around record lows. The five years prior to 2020 recorded an average vacancy rate of 3.3%, more than double the current level”.

Cotality warned that the reacceleration in rents could put renewed upward pressure on inflation.

“The reacceleration in market rents is one to watch considering the large weight allocated to rental prices in the CPI”, Cotality research director Tim Lawless said.

“There is more than a year of lag between rental value estimates and CPI rents paid, but if this uptick in rental growth continues it could gradually place some upwards pressure on inflation”.

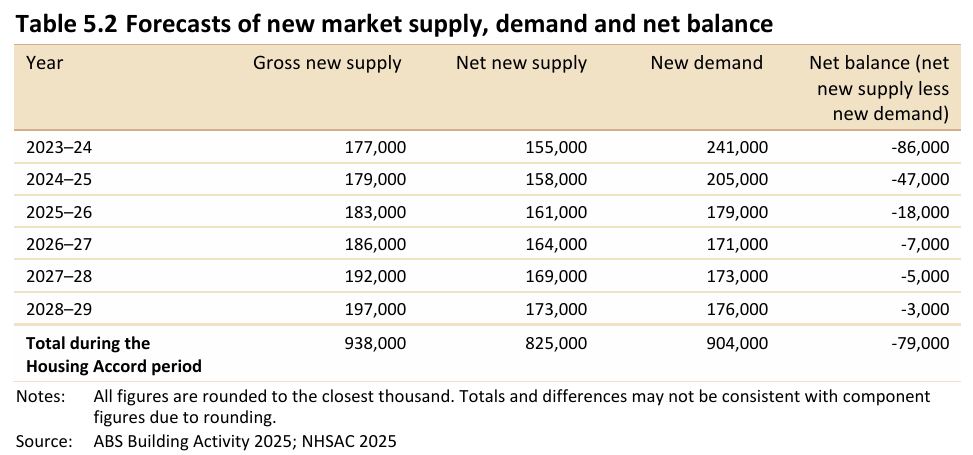

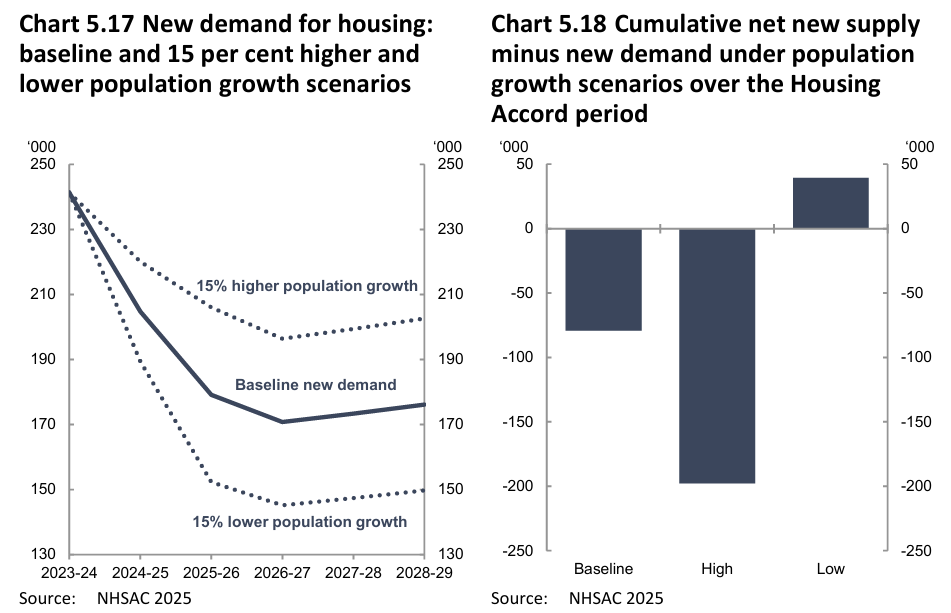

Recall that the National Housing Supply and Affordability Council (NHSAC) forecasts that new housing supply will remain below population demand over the five years to 2028–29, resulting in an additional cumulative undersupply of 79,000 homes.

NHSAC warned that ongoing strong immigration relative to supply will place upward pressure on rents and result in more homelessness and overcrowding.

“The excess of new demand relative to new supply over the Housing Accord period will worsen the existing undersupply of housing in the system and add to affordability pressures”, the NHSAC report said.

“Rental housing will remain scarce for households across the income spectrum as the vacancy rate remains below its historic average”.

“A lowered vacancy rate will absorb some of the unmet demand, and some will add to the homeless population. Some may be absorbed by suboptimal types of shelter not captured by traditional measures of the housing stock, such as caravan parks, hotels and emergency shelters. Most will be absorbed by households not forming that otherwise would have, resulting in larger households and more instances of overcrowding”, NHSAC warned.

However, NSAC’s sensitivity analysis projected a surplus of 40,000 homes after five years if population growth is just 15% less than forecast.

NHSAC’s modelling shows that the primary solution to Australia’s housing shortage is to reduce net overseas migration to a level below the nation’s capacity to build housing and infrastructure.

Otherwise, the rental crisis will continue indefinitely.