DXY is looking decidedly ill.

AUD is rampaging again.

CNY is up.

Gold is up. Oil is down.

Metals meh.

Mining bear intact.

EM to the moon.

Junk fine.

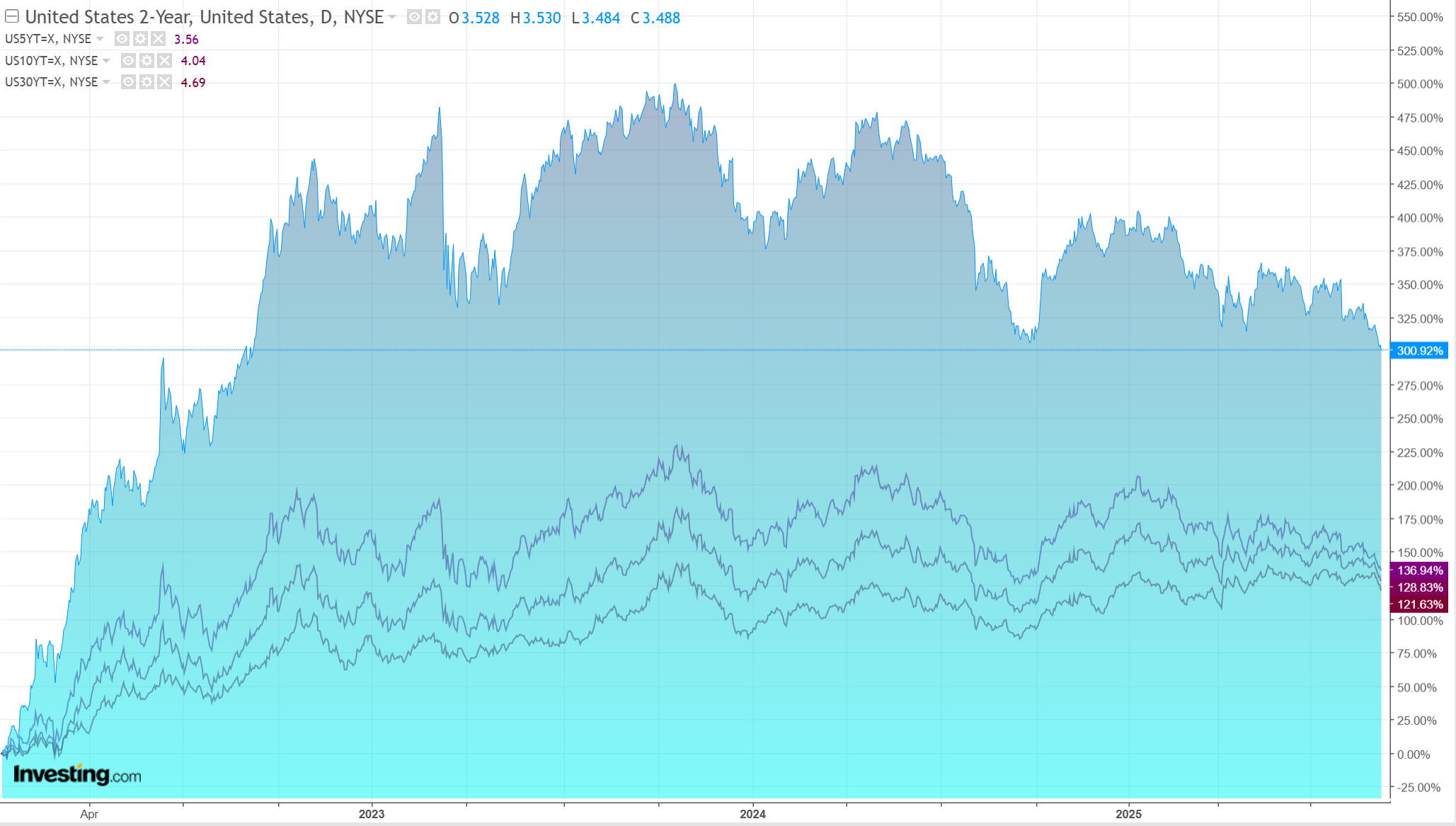

Major US yield breakdown across the curve.

Stock ATH.

Not much doubting what’s going on here. The Fed is coming, and its independence might be going, which is a pretty bearish combination for the USD. Deutsche has more.

The US is in the midst of a combined negative demand shock (tariffs) and supply shock (immigration) with the risk of fiscal dominance on top.

We argued this combination is clearly dollar negative.

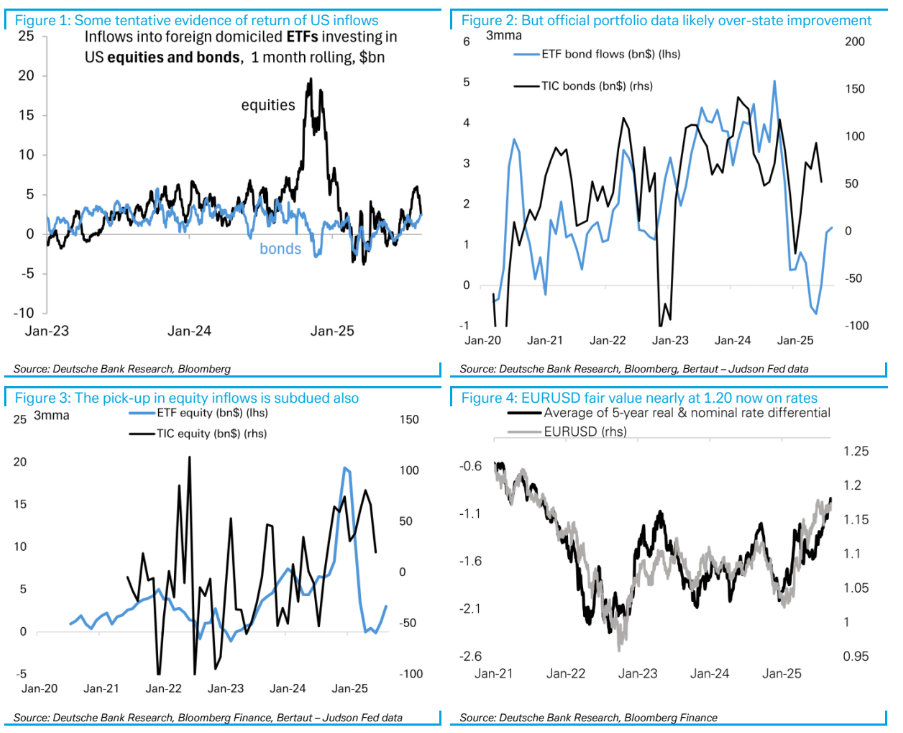

…The improvement in the flow picture has arguably removed some of the extreme tail risks that would have resulted from a complete absence of inflows.

Uncertainty about the underlying steady state of demand for US assets remains high however.

In the meantime the underlying cyclical support for the dollar has deteriorated, reflected in a material narrowing in the EUR–US rate differential which is now consistent with a financial fair value in EUR/USD in the 1.18-1.20 range (figure 4).

It is stating the obvious that additional Fed cuts from here would increase incentives to hedge dollar assets by foreign investors.

With the dollar having in the meantime removed any excess cheapness/ risk premium relating to President Trump’s policies, it still leaves the overall outlook as leaning asymmetrically dollar bearish.

I am still in the camp that the Fed will cut less than the market would like, but cut it is. Once into next year, all bets are off as Trump increasingly takes control.

It is still a bullish AUD picture of a bearish DXY.