DXY is up again.

AUD is down again.

CNY has popped.

Gold is screaming at Trump to back off the Fed.

Metals too.

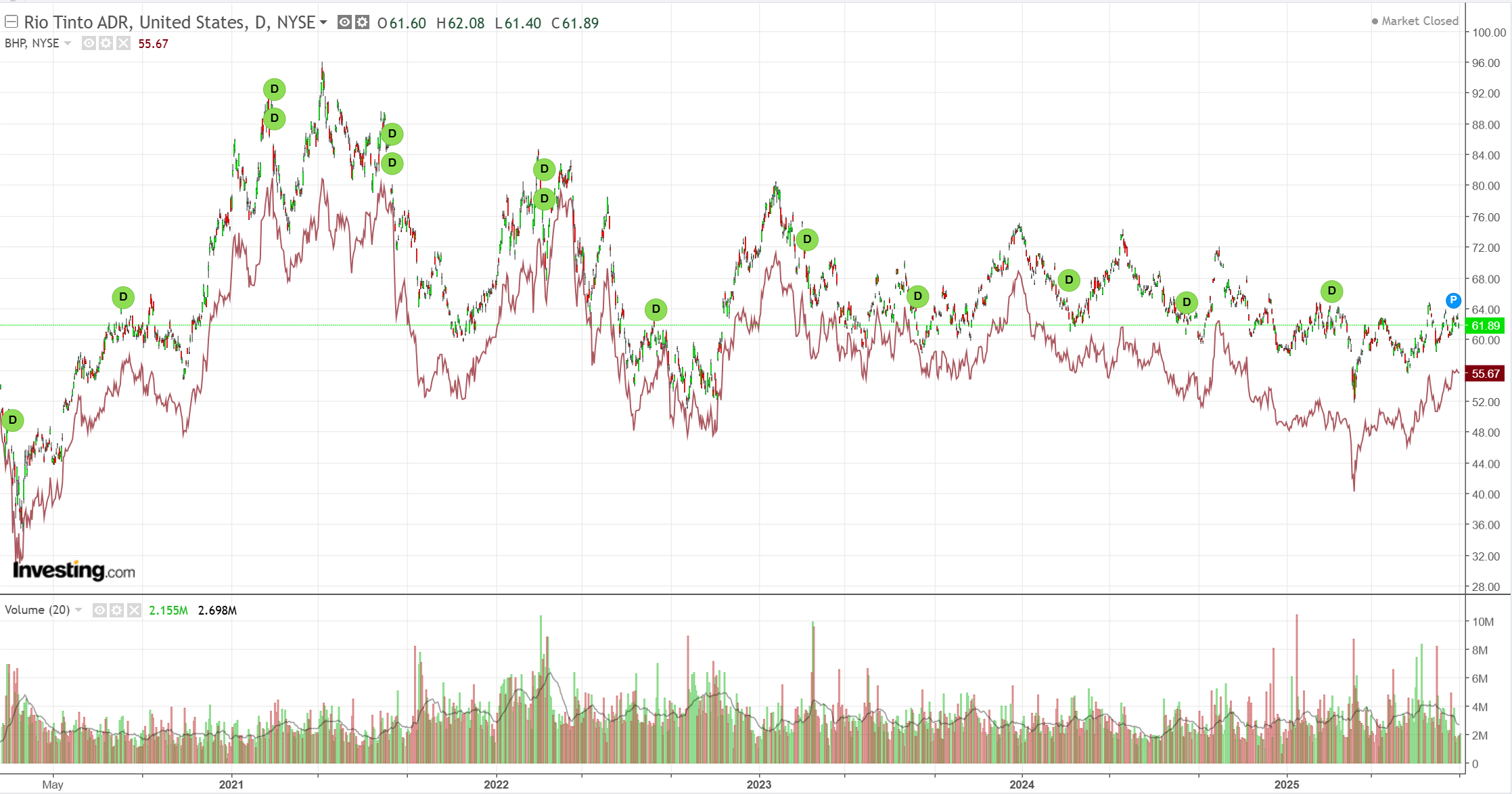

Mining bear still intact.

EM no bueno.

Junk hard reversal.

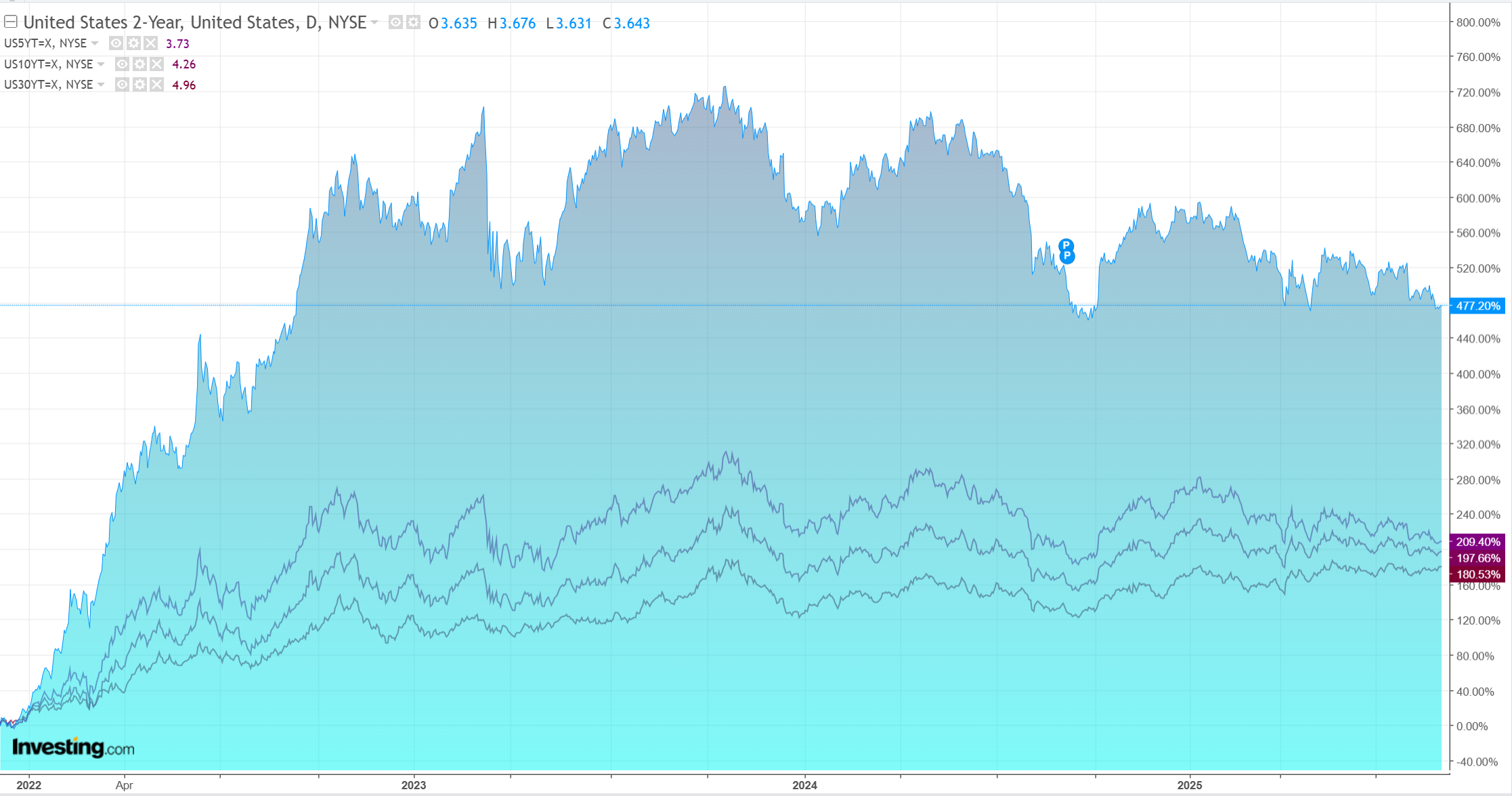

The long bond is still selling.

Stocks no likee.

The ISM had a distinctly stagflationary feel.

The Manufacturing PMI® registered 48.7 percent in August, a 0.7-percentage point increase compared to the 48 percent recorded in July.

The overall economy continued in expansion for the 64th month after one month of contraction in April 2020. (A Manufacturing PMI® above 42.3 percent, over a period of time, generally indicates an expansion of the overall economy.)

The New Orders Index indicated growth in August following a six-month period of contraction; the figure of 51.4 percent is 4.3 percentage points higher than the 47.1 percent recorded in July.

The August reading of the Production Index (47.8 percent) is 3.6 percentage points lower than July’s figure of 51.4 percent.

The Prices Index remained in expansion (or ‘increasing’) territory, registering 63.7 percent, down 1.1 percentage points compared to the reading of 64.8 percent reported in July.

The Backlog of Orders Index registered 44.7 percent, down 2.1 percentage points compared to the 46.8 percent recorded in July.

The Employment Index registered 43.8 percent, up 0.4 percentage point from July’s figure of 43.4 percent.

The new orders/inventory ratio is promising for profits, but prices are a problem.

The Fed should not be cutting with service inflation rising with sticky wages on shuttered immigration exacerbated by tariffs, and if it does, we might well see a completely counterintuitive move in markets as long yields back up and DXY takes off.

That will not be good risk assets and the AUD.