DXY is flopping around like a dead fish.

AUD was rejected once, but looks ominous for a breakout.

CNY is helping.

Gold paused. Oil is stuffed.

Metals meh.

Big bear returned.

EM to the moon!

Junk is fine.

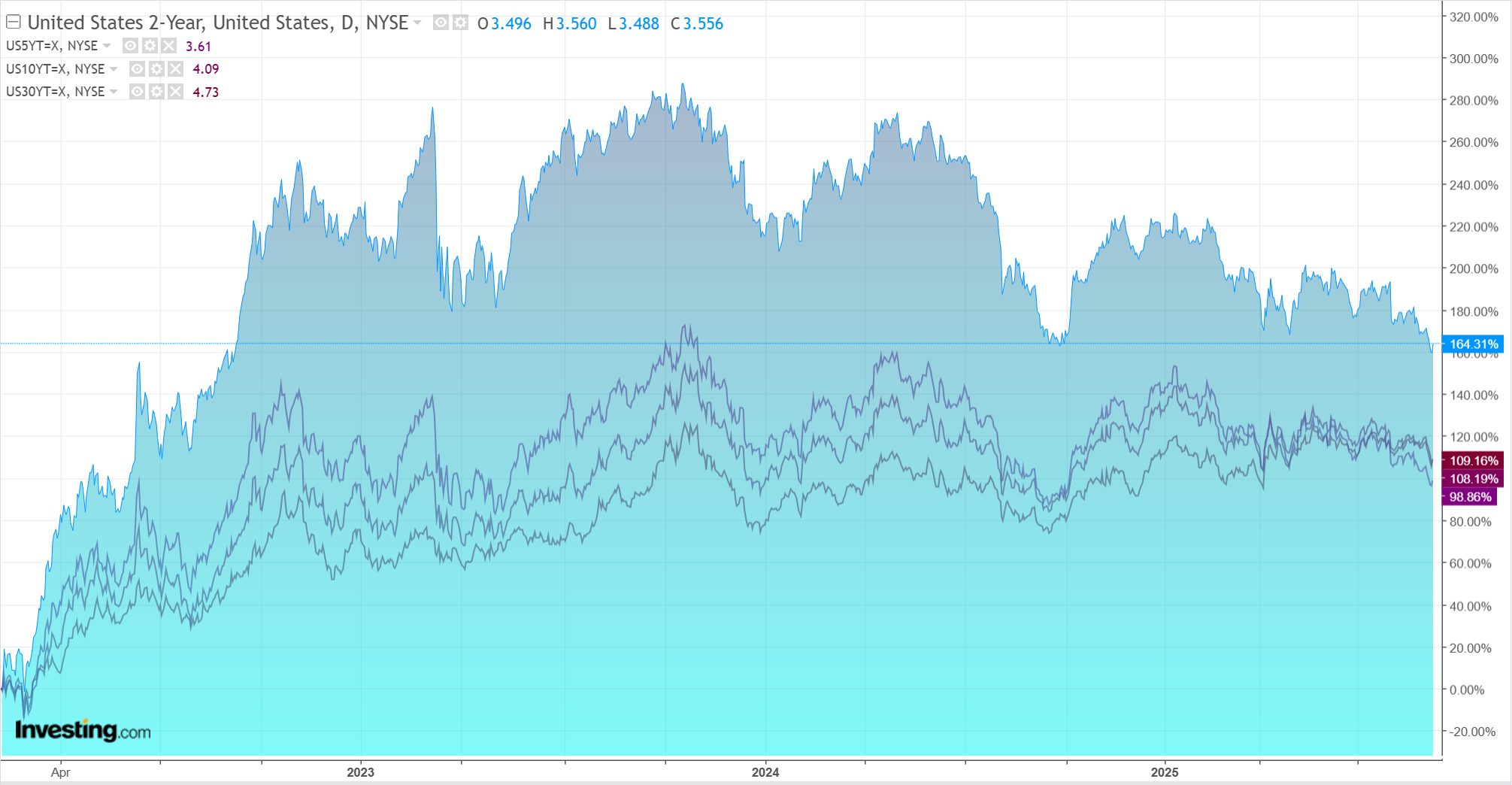

Yields reversed a bit.

Stocks ATH.

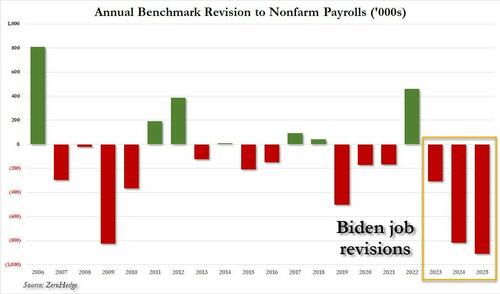

US inflation is tomorrow, so that probably accounts for yields. There is sudden speculation that the US is in recession as jobs revisions mount.

Bloomberg’s chief economist Anna Wong reckons:

Taking the preliminary benchmark estimate at face value, last year’s labor market looked recessionary:

The three-month moving average of nonfarm payrolls – often used by the Fed to gauge the underlying hiring pace — fell from 196k in March 2024 to just 6k in August 2024.

Given the brisk pace of population growth, most analysts estimated the economy needed to add around 200k net jobs each month to stabilize the unemployment rate. The three-month average suggests job creation was running significantly below the breakeven level.

There also were likely two months of negative payrolls last year – August (-5k) and October (-32k).

Payrolls rebounded after the Fed began cutting rates in September, with the three-month moving average recovering to 133k by December. But payrolls slowed again early this year, with the three-month average dropping to 35k in March.

That’s quite a revision, to be sure. Not that Trump sacking the BLS moss will change anything. The numbers are not made by the department head.

Some of this labour market weakness is probably AI as well.

Are we about to enjoy a US growth scare? Maybe. Housing is weak. Light and heavy vehicle sales are soft. Unemployment is up. There’s a demand shock in tariffs.

Probably not with the Fed chiming in, but early-cycle cuts are often a bearish signal.

Be on your guard for sharp reversals, including AUD.