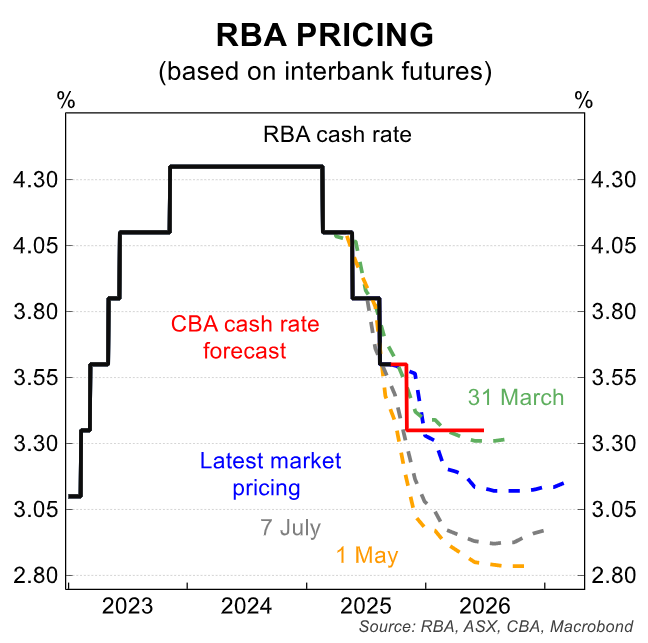

Belinda Allen, CBA’s Head of Australian Economics, believes that the Reserve Bank of Australia (RBA) will only cut the official cash rate (OCR) once more in November, given the recent stronger run of economic data.

This would take the OCR to 3.35%, which is close to CBA’s estimate of neutral.

Market pricing has also shifted higher, with less easing now expected.

Allen highlights “seven pieces of economic data that collectively have confirmed an economic recovery is becoming entrenched in the economy”.

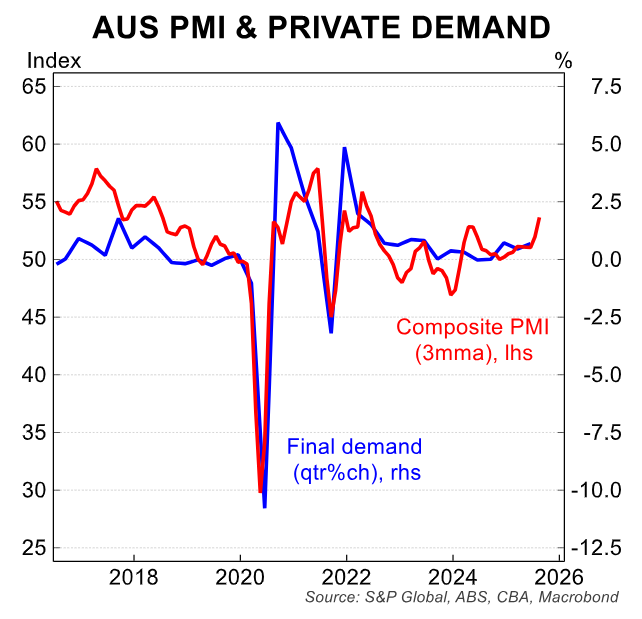

First, the S&P Composite PMIs have shifted higher:

“Historically the composite PMI tracks final demand in the economy quite well”, Allen notes. “Overall, it suggests that the economy should continue to improve from here”.

“Diving into the details shows new orders and the employment components have both moved higher and point towards further improvement in economic momentum in the September quarter”.

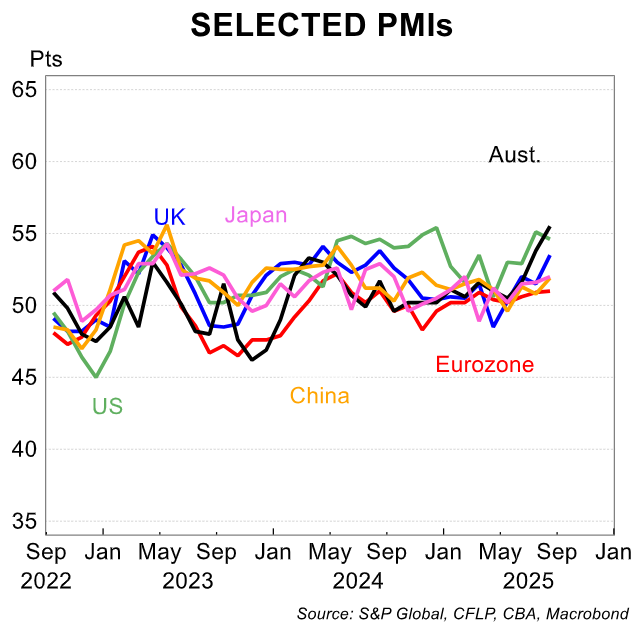

“Australia also has the highest PMI index out of a number of advanced economies, indicating the change of fortunes in recent months”.

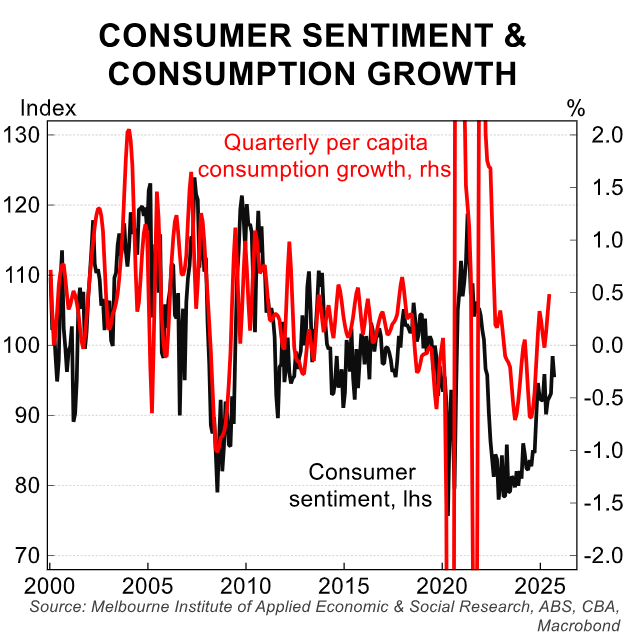

Second, the Westpac / MI consumer sentiment index has trended higher.

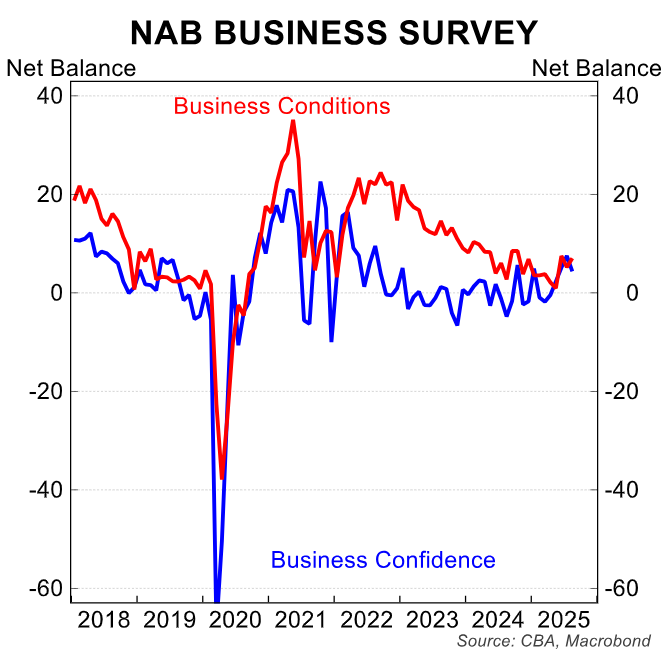

Third, the NAB business survey has also shown a reversion to trend:

“The conditions index is currently sitting around its long-term average, the same as business confidence”, Allen noted.

“Improvements in employment, profitability and trading all point to an economy that should be growing around its potential. The implication of course is the cash rate should settle around neutral. Capacity utilisation has also picked up suggesting improved momentum in the economy”.

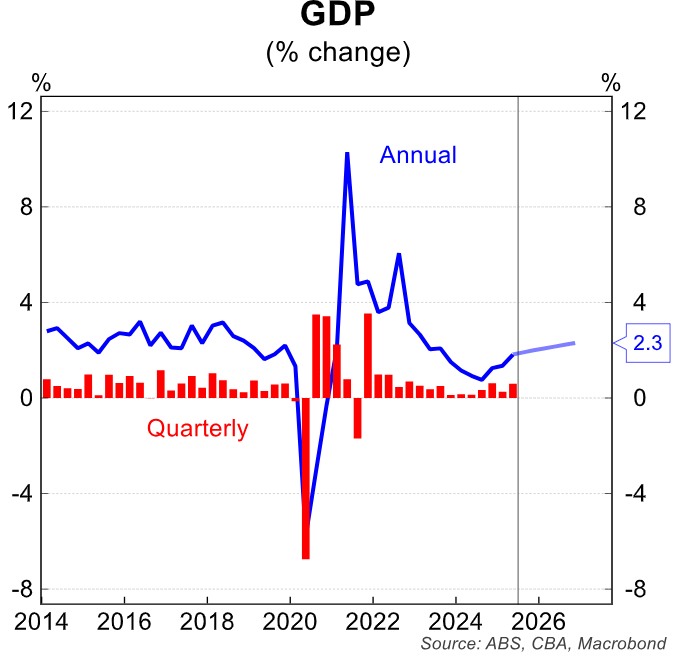

Fourth, Australia’s GDP growth has picked up, printing stronger than consensus and the RBA’s forecasts in the second quarter:

“Importantly, the data confirmed a transition from public to private sector growth is underway”, Allen wrote.

“Household consumption did the heavy lifting. We had noted CBA spend data showed strength in Q2 25 and this was confirmed by a 0.9% lift in household consumption in the quarter, taking the annual growth rate up to 2.0%”.

“At 1.8%/yr growth rate, the economy is closing in on the RBA’s estimate of potential growth rate of 2%. We expect economic activity to improve to 2.3% in 2026”.

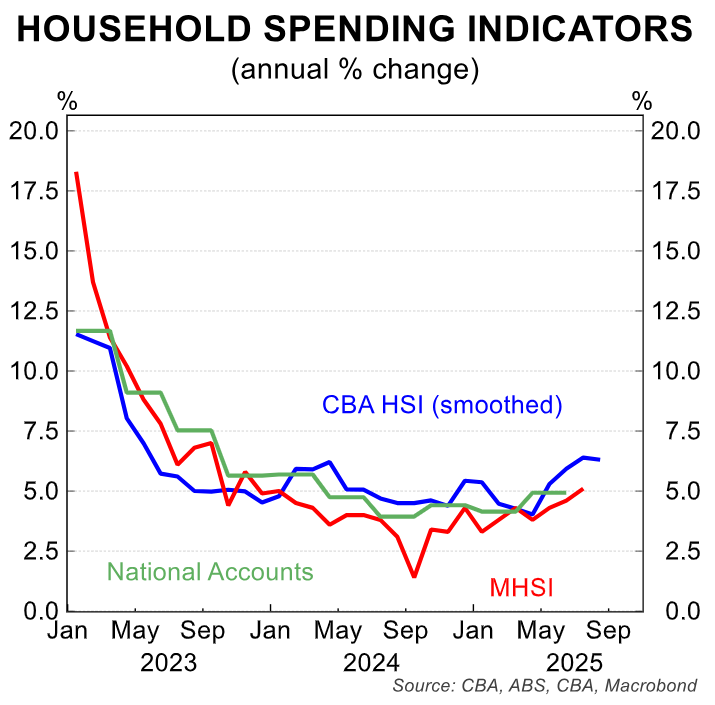

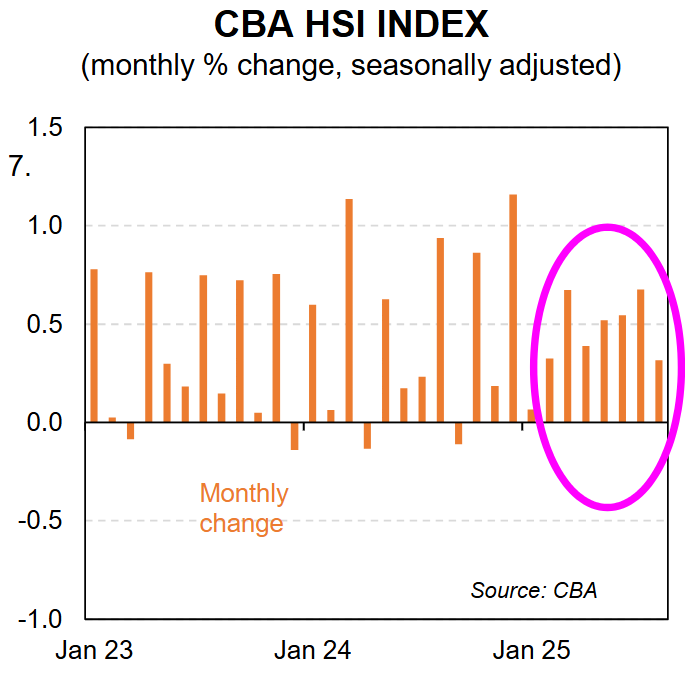

Fifth, reflecting the above, CBA consumer spending data has firmed:

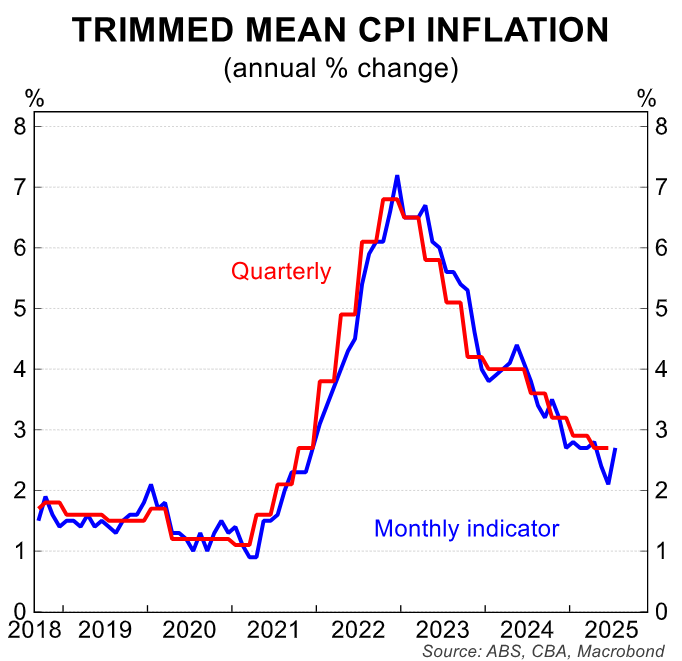

Sixth, the July CPI printed higher than expected at 2.7%/yr, and the headline rate at 2.8%/yr (compared to expectations of 2.3%):

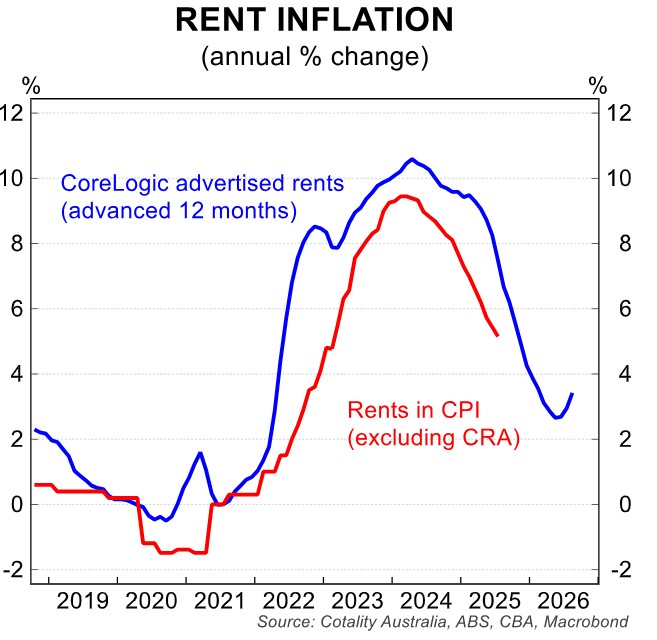

“Advertised rents have ticked higher again and new dwelling construction costs have lifted in three out of the past four months”, Allen notes.

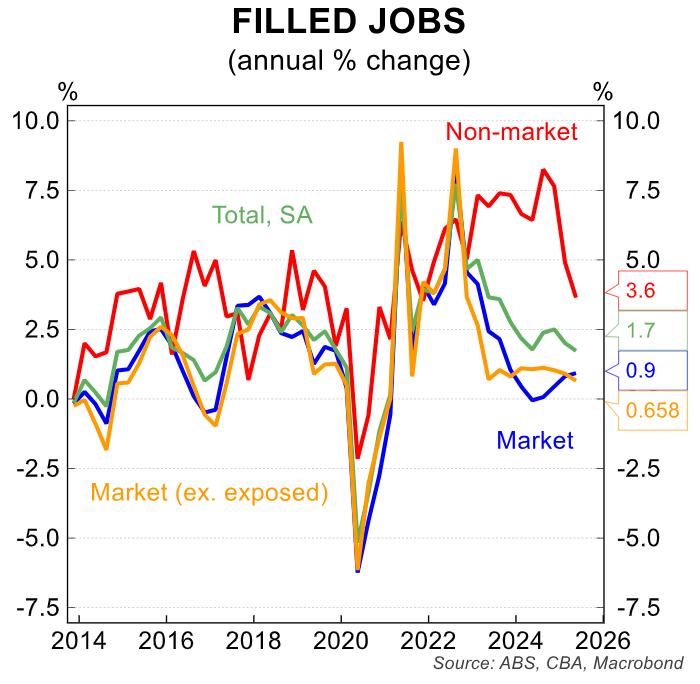

Seventh, Allen claims there has been a non-market to market jobs transition:

“In Q2 25, the labour account total filled jobs growth increased by 0.2% to be 1.7% higher through the year”, Allen noted.

“Non-market sector jobs rose 0.3% (+14k) while market sector jobs rose 0.2% (+22k). Annual growth was +3.6% (+168k) and +0.9% (+103k) respectively. So far, the market sector has stepped up to absorb most, but not all of the slack”.

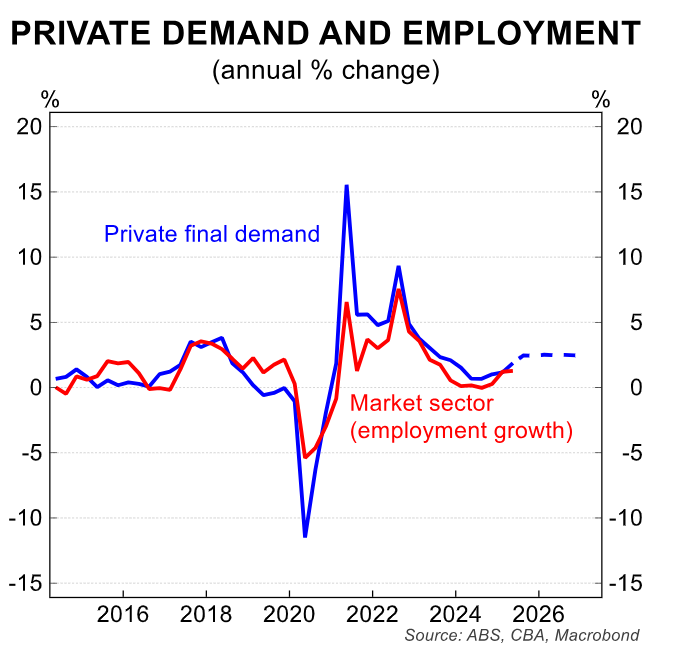

“We would note looking at the relationship between private final demand and market sector employment there is reason to be optimistic for an orderly handover”.

My main contention with Allen’s reasoning is the strong risk that there is not a smooth transition from non-market to market sector jobs.