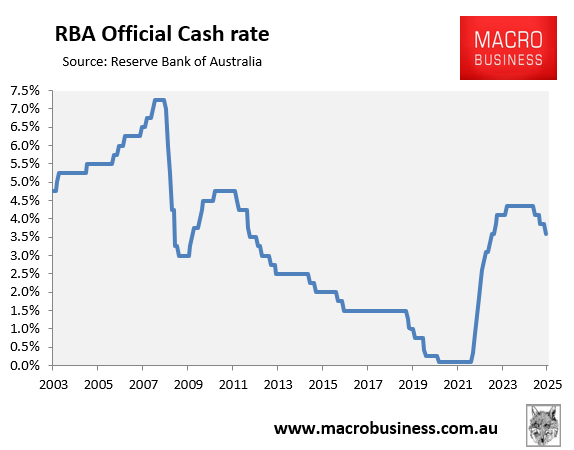

Alongside this week’s 0.25% interest rate cut from the Reserve Bank of Australia (RBA), it noted that it expects to lower the cash rate “gradually”.

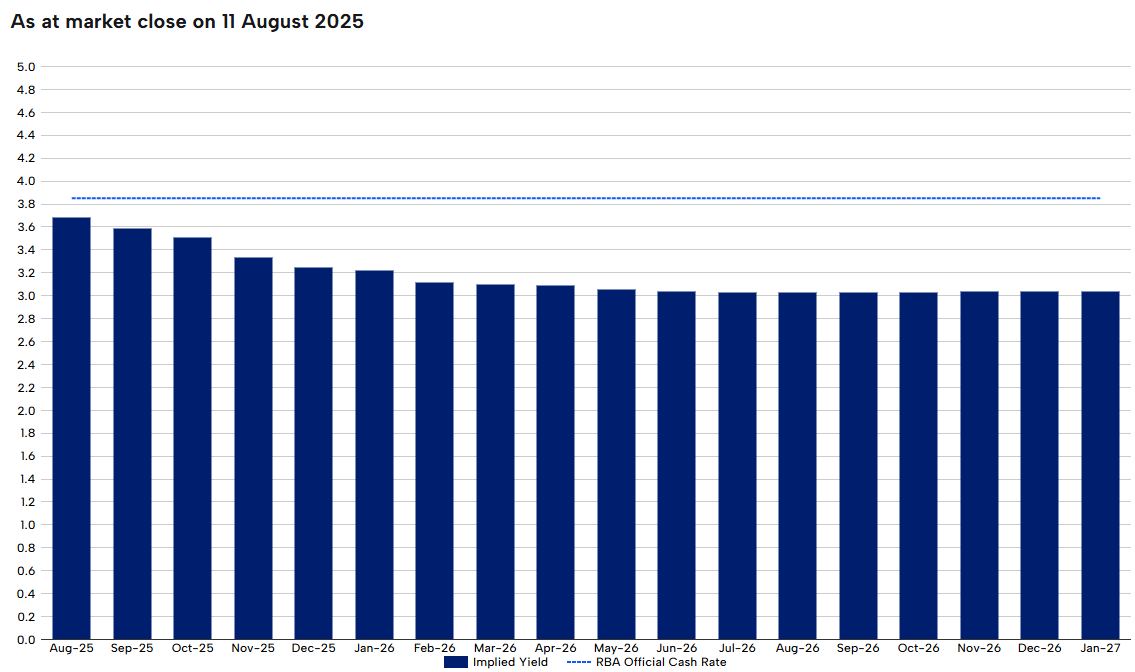

Financial markets are currently tipping one more rate cut this year, followed by another in early 2026.

This would take the official cash rate to 3.10%, 1.25% below its recent peak.

However, the RBA Statement of Monetary Policy’s (SoMP) forecasts allow for significantly larger rate cuts.

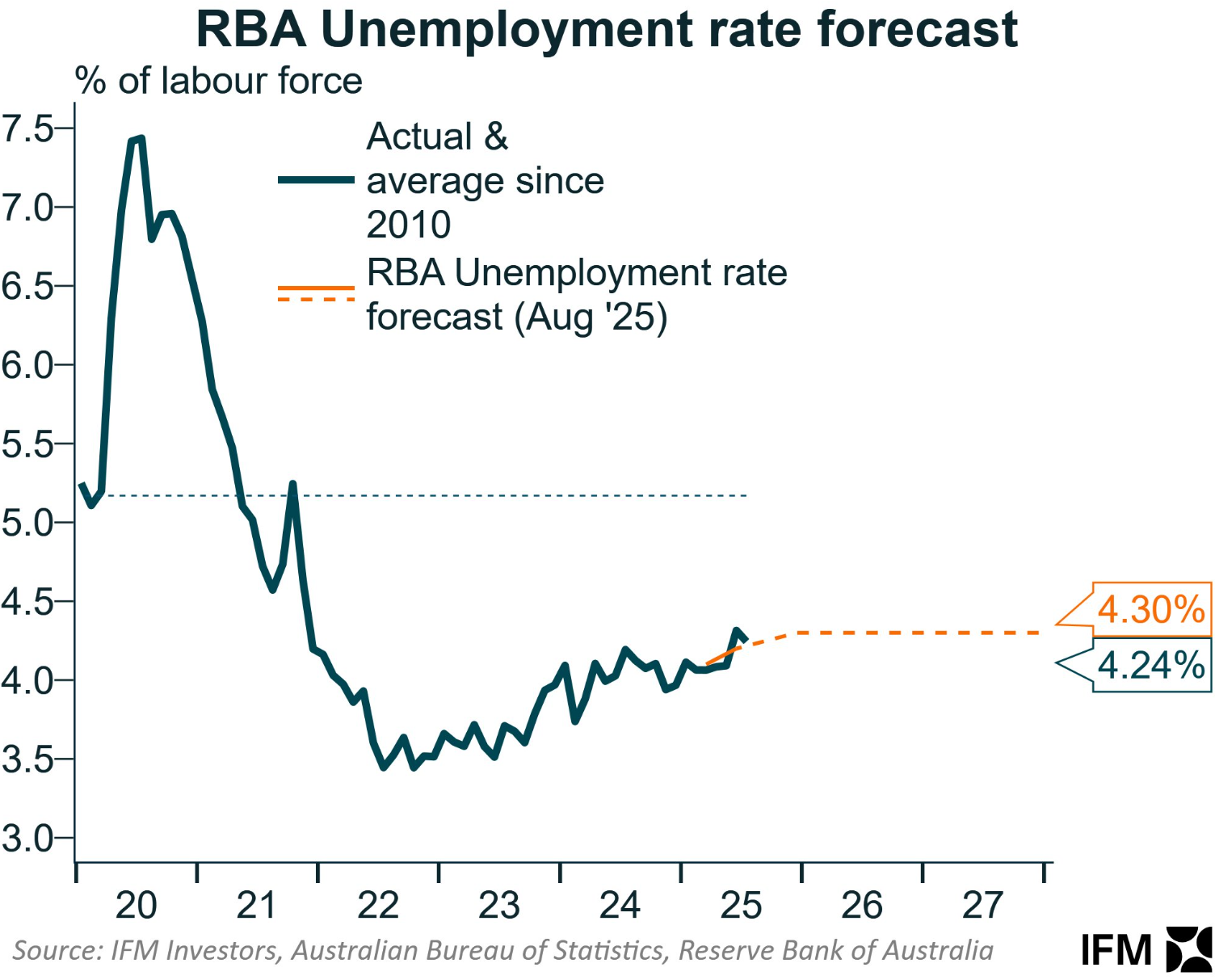

The August SoMP lowered its forecasts around GDP growth, productivity growth, and wage growth.

However, surprisingly, the RBA left its forecast for unemployment at 4.3%—the current level—until the end of 2027. This is the same unemployment forecast as the May SoMP.

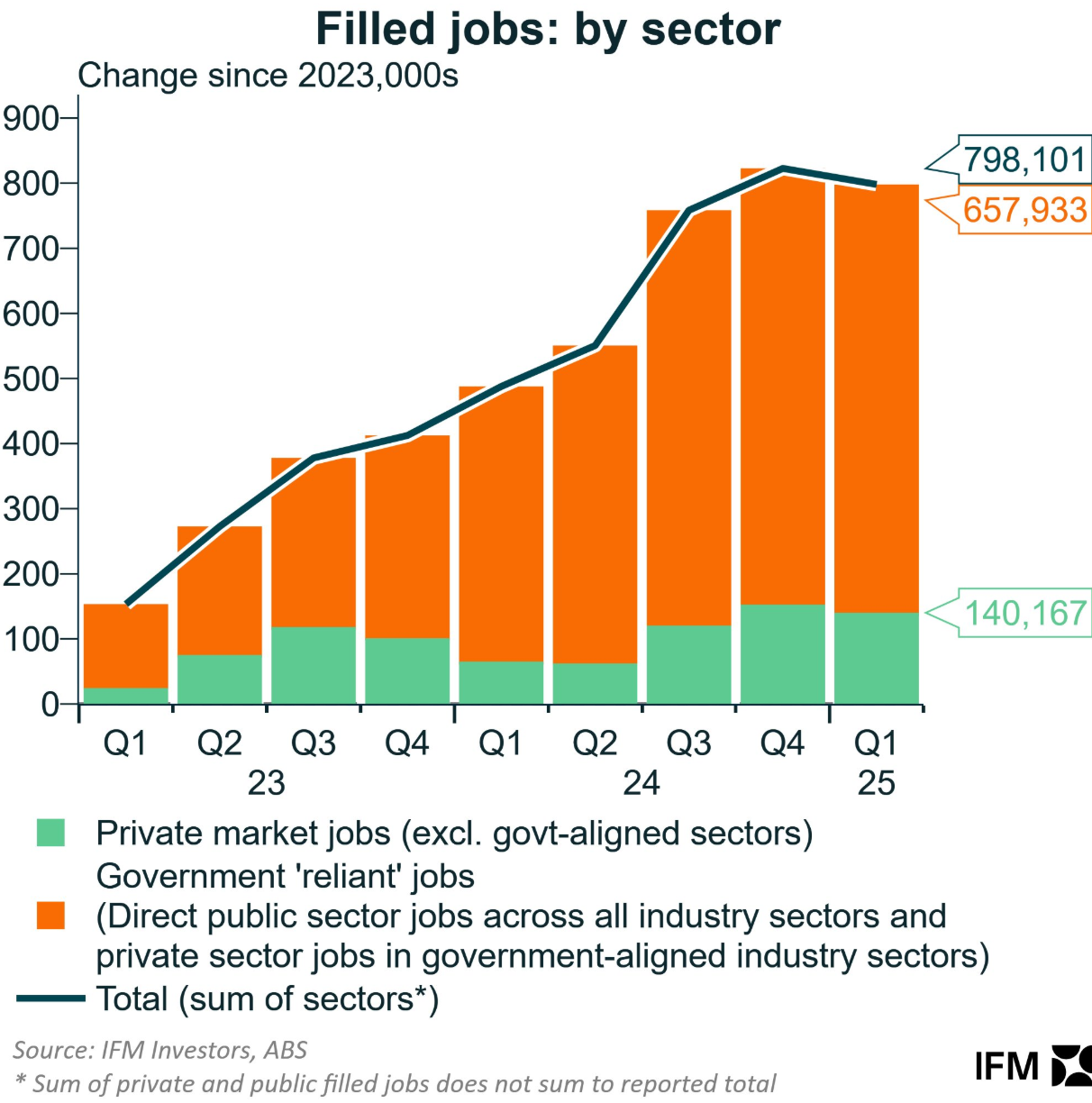

The non-market (government-funded) sector has dominated Australia’s recent job growth and is the primary reason why the unemployment rate is tracking at its current historically low level of 4.2%.

As illustrated below by Alex Joiner from IFM Investors, 82% of jobs created in Australia between Q1 2023 and Q1 2025 were in the non-market sector, driven by the expansion of the NDIS.

The non-market sector generated around 658,000 jobs between Q1 2023 and Q1 2025, compared to only 140,200 jobs created in the market (private) sector.

With federal and state budgets in deficit, both are looking at ways to curb expenditure and “right size” their workforces. The federal government has also committed to stem the cost of the NDIS.

Therefore, non-market sector will no longer be the driver of job growth in Australia. Indeed, Q1 2025 was the first time in several years that the non-market sector actually shed jobs.

The RBA SoMP’s forecasts suggest that it expects a seamless transition of job creation from the non-market to the market sector, which is highly unlikely.

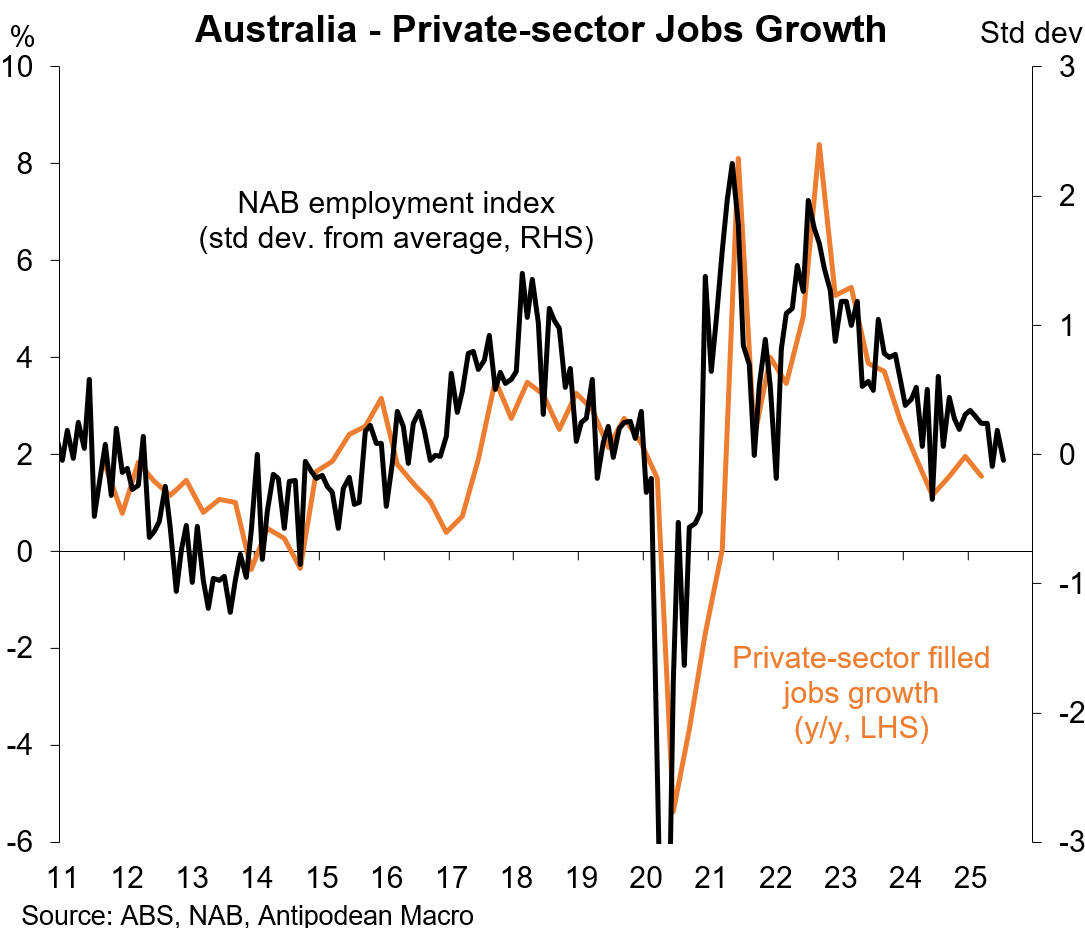

If fact, as illustrated below by Justin Fabo from Antipodean Macro, the NAB employment index for July suggests that private sector job growth is weakening:

The upshot is that with job growth likely to continue slowing at the same time as the labour force continues to grow strongly via net overseas migration, Australia’s unemployment rate is destined to rise above the RBA’s projection.

When this happens, the RBA will be forced to lower the cash rate in a bid to stimulate the private sector economy.

In summary, rising unemployment is likely to result in deeper rate cuts in Australia.